Finance Friday

Ranora Daily - Your daily source for reliable market analysis and news.

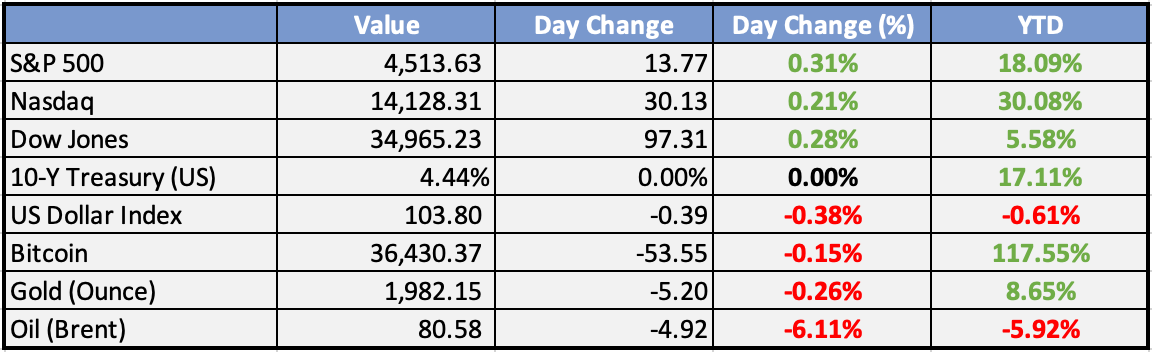

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Land reforms to unlock $300bn dead capital – FG - Daily Trust

The federal government has stated that the ongoing land reforms would help to unlock $300billion dead capital.

Nigeria withdraws $1bn claim against Eni - Punch

The Federal Government has concluded plans to withdraw civil claims totalling $1.1bn against Eni SpA, ending a long battle in Italian courts over allegations of corruption in an oil field deal.

Nigeria can't rely on borrowing—Minister of Finance Wale Edun - Daily Post

The Minister of Finance and Coordinating Minister for the Economy, Wale Edun, declared on Thursday that Nigeria could not continue to rely on borrowing to fund its budgets, stressing the need for adequate revenue to finance them.

Ecobank, AGF Sign Transformative $200m Risk Sharing Agreement - ThisDay

Ecobank and the African Guarantee Fund (AGF), yesterday joined forces in a groundbreaking $200 million risk-sharing agreement, aimed at catalyzing economic growth and supporting entrepreneurial ventures – including women-owned (SMEs) on the continent.

Global

US continuing jobless claims rise to highest in almost two years - Bloomberg

U.S. unemployment benefits rose to nearly a two-year high, reaching 1.87 million in the week ended Nov. 4, marking eight consecutive weeks of increases. Initial jobless claims also rose to 231,000 in the week ending Nov. 11, the highest since August. These numbers indicate a cooling in the labor market, increasing price pressures, and subdued consumer spending.

Bitcoin falls 4.94% to $36,007 - Reuters

Bitcoin experienced a 4.94% drop, reaching $36,007 and shedding $1,870 from its previous close. The leading cryptocurrency is down 5.2% from its peak of $37,978 on November 9. Ether, the cryptocurrency associated with the Ethereum blockchain, also saw a decline, dropping 4.86% to $1,959.8 and losing $100.2 from its previous close

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian markets showed mixed performance this morning. Japan and Australia closed marginally higher, while Hong Kong, China, and the Kospi experienced a pullback. India faced declines due to new loan regulations.

In an interesting development, the USD/JPY pulled back below 150 for the first time since November 6. The Japan Trade Union Chief expressed intentions to seek wage hikes beyond 2024, emphasizing the importance of bringing wages in line with global standards. However, Japan’s Deputy Finance Minister reiterated that they won’t intervene solely because the JPY is weakening, and they don’t have a specific FX level in mind for intervention.

Bank of Japan (BOJ) Governor Ueda reiterated the consideration of ending Yield Curve Control (YCC) and negative rates if the price goal is in sight. He also noted an overall assessment that the domestic economy has recovered moderately and is likely to continue doing so.

Indian banks and financials faced a downturn due to the government’s new policies tightening loan regulations after an unprecedented rise in consumer loans. The Sensex Index (-0.28%) and the Nifty50 (-0.17%) closed lower, with concerns that the credit tightening could impact consumer spending and GDP growth.

Europe, Middle East, Africa:

European equities traded higher this morning, and there were no changes to the final Eurozone Consumer Price Index (CPI) numbers.

ECB’s Holzmann (Austria, hawk) stated that the ECB would not cut rates in Q2 2024.

Moody’s is set to update Italy’s sovereign ratings, currently one notch above junk with a negative outlook. S&P affirmed the rating on October 20, and Fitch decided on November 10, both rating Italy at the second-lowest investment grade with a stable outlook. Moody’s rating for Italy is already the lowest investment grade (Baa3) with a negative outlook.

The Americas:

Money Market Fund Assets reached a record $5.73 trillion, with $21.9 billion flowing in over the past week, leading to speculation about ample dry powder on the sidelines.

US Industrial Production declined by 0.7% year-on-year in October 2023, following a revised 0.2% contraction in the previous month. Continuing Jobless Claims in the US are at the highest level in two years (1865k), rising for eight straight months, and Initial Jobless Claims also came in higher at 231k versus 218k prior. The 4-week average has moved up to 220k from 212k.

Bank of America’s Weekly Flows showed the first outflow from Treasuries since February 2023 ($1 billion), the second-largest inflow into stocks in 2023 ($23.5 billion), the largest inflow into US Large Cap Stocks since February 2022 ($23.7 billion), the first inflow into Financials since July 2023 ($0.9 billion), and the fifth consecutive week of inflows into Materials ($1.1 billion cumulative), the longest streak since May 2022.

The Week Ahead:

Monday:

Tuesday:

U.S. inflation slows to 3.2% in October

Eurozone's GDP declines by 0.1% in Q3

US mortgage applications up 2.8%

Wednesday:

UK producer prices up by 0.1% in October

UK inflation down to 4.6% in October

US Core Producer Price Index is at a current level of 140.24, down from 140.29 last month

US Retail sales decreased by 0.1% m/m in October 2023

US NY Empire State Manufacturing Index rose 14 points to 9.1 in November 2023

Thursday:

Unemployment Claims (US) fell to 192,000

Friday:

UK retail sales down 0.3% in October

Investment Tip of The Day

Assess Mutual Fund Overlap: If you hold multiple mutual funds, analyze the overlap in their holdings. Overconcentration in similar assets can expose you to higher risks.

Meme of the Day