Finance Friday

Ranora Daily - Your daily source for reliable market analysis and news.

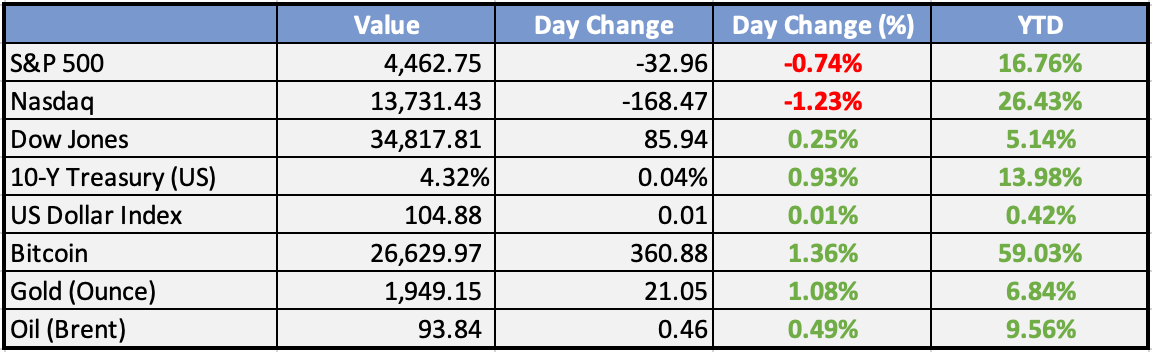

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Nigeria’s total public debt jumps N87.3 trillion in Q2 – DMO - Naira Metrics

Nigeria's total public debt increased to N87.3 trillion in the second quarter, according to the Debt Management Office (DMO). This represents a significant jump and is attributed to increased borrowings amid revenue challenges faced by the country. External debt accounted for about 36.77% of the total debt, while domestic debt made up the remaining 63.23%.

AfDB is ready to disburse $250 million for Nigeria’s electrification project – Minister for Power - Naira Metrics

The African Development Bank (AfDB) is prepared to release $250 million for Nigeria's electrification project, according to Nigeria's Minister for Power. This financial support aims to enhance access to electricity and improve the country's power infrastructure.

Global

August wholesale inflation rises 0.7%, hotter than expected, but core prices in check - CNBC

The Producer Price Index (PPI) for August 2023 indicates rising inflation pressures, with a 0.6% increase from the prior month. This surge is primarily attributed to higher energy prices, particularly gasoline, and it marks the most significant monthly gain in over a year. Core PPI, excluding food and energy costs, also showed a substantial increase of 0.4% from July.

IRS shuts door on new pandemic tax credit credit claims until at least 2024 - WSJ

The IRS is temporarily suspending the acceptance of claims for the Employee Retention Credit (ERC) tax credit until 2024 due to concerns about fraudulent applications. The ERC was designed to assist small businesses during the pandemic by helping them pay their employees when they were fully or partially suspended from operating.

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian equities closed mostly higher on Friday. Gains were led by China-trade-related and technology-heavy markets, with Australia, South Korea, and Taiwan all posting solid returns. Greater China experienced an uneven day, despite better-than-expected economic activity data. Hong Kong ended higher but well off its highs, while mainland Chinese markets closed in the red. Japanese equities ended at six-week highs.

There appears to be a slight improvement in data from China, with Industrial Production and Retail Sales beating estimates. Industrial production rose by 4.5% YoY, while Retail Sales increased by 4.6% YoY. However, housing data wasn’t as positive, with China’s new house prices falling by 0.3% MoM in August, marking the steepest decline in ten months.

The People’s Bank of China (PBOC) announced on September 14th that it would cut the reserve requirement ratio (RRR) by 25 basis points for all financial institutions except those already facing a 5% RRR. A PBOC official stated that the rate cut is expected to release more than CNY 500 billion ($70 billion) in liquidity.

Iron ore reached a five-month high as China’s property downturn continued.

The Taiwan Stock Exchange is looking to diversify by attracting a new crop of technology companies.

The Japanese government is considering extending fuel subsidies to compensate for inflation.

Europe, Middle East, Africa:

European equity markets generally showed gains. The Personal and household Goods sector led the way, with many constituents exposed to China. The Construction/Materials and Basic Resources sectors also saw increases, while the Technology and Retail sectors lagged.

A noteworthy development from the ECB meeting was a new sentence in the statement indicating that policy rates “had reached levels that, maintained for a sufficiently long duration, would make a substantial contribution to the timely return of inflation to target.” This has led the market to interpret the 25-basis point hike as potentially the last one, although the ECB has not ruled out further tightening.

The EUR/USD currency pair reached a six-month low following the ECB’s dovish rate hike.

European mining stocks are being watched closely in anticipation of Chinese stimulus measures potentially providing a much-needed boost to the sector.

French Finance Minister Le Maire announced the government’s aim to achieve €16 billion in savings after reducing its growth outlook. The French economy is forecasted to grow by 1.4% next year, down from the previous estimate of 1.6%.

The Americas:

Arm Holdings (ARM) had a successful debut, pricing its largest IPO since Rivian in 2021 at $51. The stock opened at $56.10 on 13.3 million shares and closed at $63.59, likely providing a boost to tech shares overall.

Auto workers in Detroit initiated a strike after negotiations between union leaders and the Big Three automakers broke down at the midnight deadline. Workers began walking out of Ford Motor’s Michigan plant that makes the Bronco SUV, a General Motors facility in Missouri, and a plant in Ohio that manufactures the Jeep Wrangler. This marked the first time in history that the UAW took action against all three carmakers simultaneously.

Disney is set to hold talks regarding a potential sale of ABC to Nexstar. Byron Allen has made a $10 billion offer. Additionally, Disney is expected to downgrade its 2024 streaming subscriber forecast.

Apple has appointed a new head for its project aimed at developing a glucose monitor that doesn’t require a skin prick for a blood sample. This news led to a decline in the share prices of DexCom and Tandem.

TSMC (Taiwan Semiconductor Manufacturing Company) has instructed major suppliers to delay the delivery of high-end chipmaking equipment due to concerns about demand.

Salesforce is planning to hire 3,300 people across various departments after layoffs earlier this year.

The U.S. is preparing new sanctions on Russia, targeting companies and individuals profiting from Moscow’s invasion.

The Week Ahead:

Monday:

Tuesday:

Wednesday:

UK Manufacturing PMI was revised slightly higher to 43.0 in August 2023, up from the preliminary estimate of 42.5.

Industrial production in the Euro Area declined by 1.1% month-over-month in July 2023.

The consumer price index, rose 0.6% for the month and was up 3.7% from a year ago.

Thursday:

Employment in Australia surged by 64,900 to 14.10 million in August 2023, easily topping market forecasts of a 23,000 gain

Retail trade sales grew 0.6% in August compared to July, while increasing 1.6% year over year.

Friday:

China's industrial output up 4.5 pct in August

The NY Empire State Manufacturing Index surprisingly jumped to 1.9 in September 2023 from -19 in August

Industrial Production (MoM) (US)

Michigan Consumer Sentiment declined from 69.5 in August to 67.7 in September

Investment Tip of The Day

Establish an Emergency Fund: Maintain a dedicated emergency fund separate from your investments. This cash reserve provides a safety net for unexpected expenses, reducing the need to sell investments during market downturns.

Meme of the Day