Finance Friday- Energy Expansion and Capital Flows Drive Nigerian Market Narrative Amid Global Policy Shifts

Ranora Daily - Your daily source for reliable market analysis and news.

Market Overview

Good evening and welcome to today’s market kick-off, where Nigerian markets are shaped by fresh energy-sector developments, corporate capital raising, and policy support initiatives. Key highlights include strategic board changes at Seplat, renewed momentum in oil and port infrastructure, and continued deepening of Nigeria’s capital markets. Globally, central bank actions and easing trade tensions are influencing risk sentiment across assets.

Nigerian News & Market Update

Seplat appoints Elumelu as board member:

Tony Elumelu has been appointed Non-Executive Director of Seplat Energy following his investment vehicle’s acquisition of a 20.07% stake in the company. - Punch

Nestlé achieves 100% plastic neutrality:

Nestlé Nigeria has achieved 100% plastic neutrality by recovering every tonne of plastic it introduced into the market through the Food and Beverage Recycling Alliance. - Punch

Tinubu approves commercial oil drilling in Ogun:

President Tinubu has approved commercial oil drilling at Tongeji Island and the immediate take-off of the Olokola Deep Seaport project in Ogun State. - Punch

FCMB-TLG private debt fund series 2 to open with ₦20billion offer:

FCMB Asset Management is launching Series 2 of its Naira-denominated Private Debt Fund with a offer targeting institutional and high-net-worth investors. - DailyTrust

Tinubu okays incentives for Shell’s Bonga Southwest project, eyes jobs, FX boost:

President Tinubu has approved targeted incentives to accelerate Shell’s Bonga Southwest project, aiming to boost jobs, foreign exchange, and long-term revenue for Nigeria. - TheSun

GTCO raises ₦10 billion through private placement:

GTCO raised ₦10 billion through a fully subscribed private placement of 125 million shares at ₦80 each to strengthen its capital base. - PremiumTimes

Nigeria Sectoral Indices Performance

The table below shows that the daily performance was mixed, with modest gains across most indices, while Insurance was the sole laggard on the day (-0.42%). Week-to-date performance remained broadly negative, except for Oil & Gas and the Lotus Index, reflecting short-term market softness. Medium- to long-term trends are strong, led by Oil & Gas (13.73% MTD/YTD) and Insurance (10.87% MTD/YTD), highlighting sustained sectoral momentum.

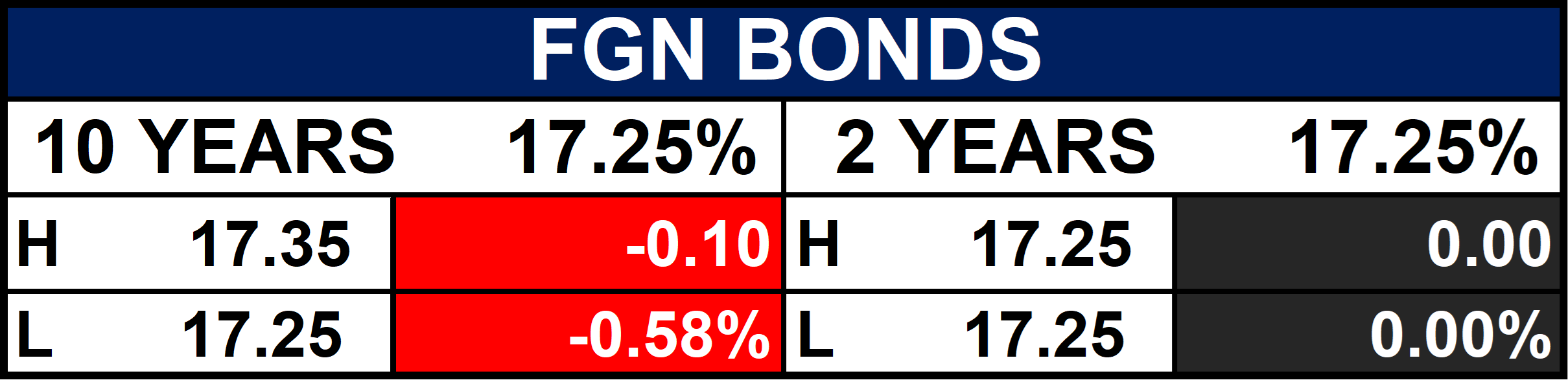

Fixed Income (FGN Bonds)

Global News & Market Update

India’s central bank to inject over $23 billion of liquidity into banking system:

The Reserve Bank of India plans to inject over $23 billion into the banking system through bond purchases, FX swaps, and repos to support liquidity and stabilize the rupee. - Reuters

EU to suspend 93 billion euro retaliatory trade package against US for 6 months:

The EU will suspend its €93 billion retaliatory trade measures against the U.S. for six months following eased tariff tensions. - Reuters

BOJ keeps rates steady as expected, ups growth and inflation forecasts:

The Bank of Japan kept interest rates at 0.75% while raising growth and inflation forecasts, signaling a cautious path toward future rate hikes. - Reuters

China to offer LNG futures as soon as next month:

China plans to launch yuan-denominated LNG futures next month to reduce reliance on Western benchmarks and strengthen its domestic energy market. - Reuters

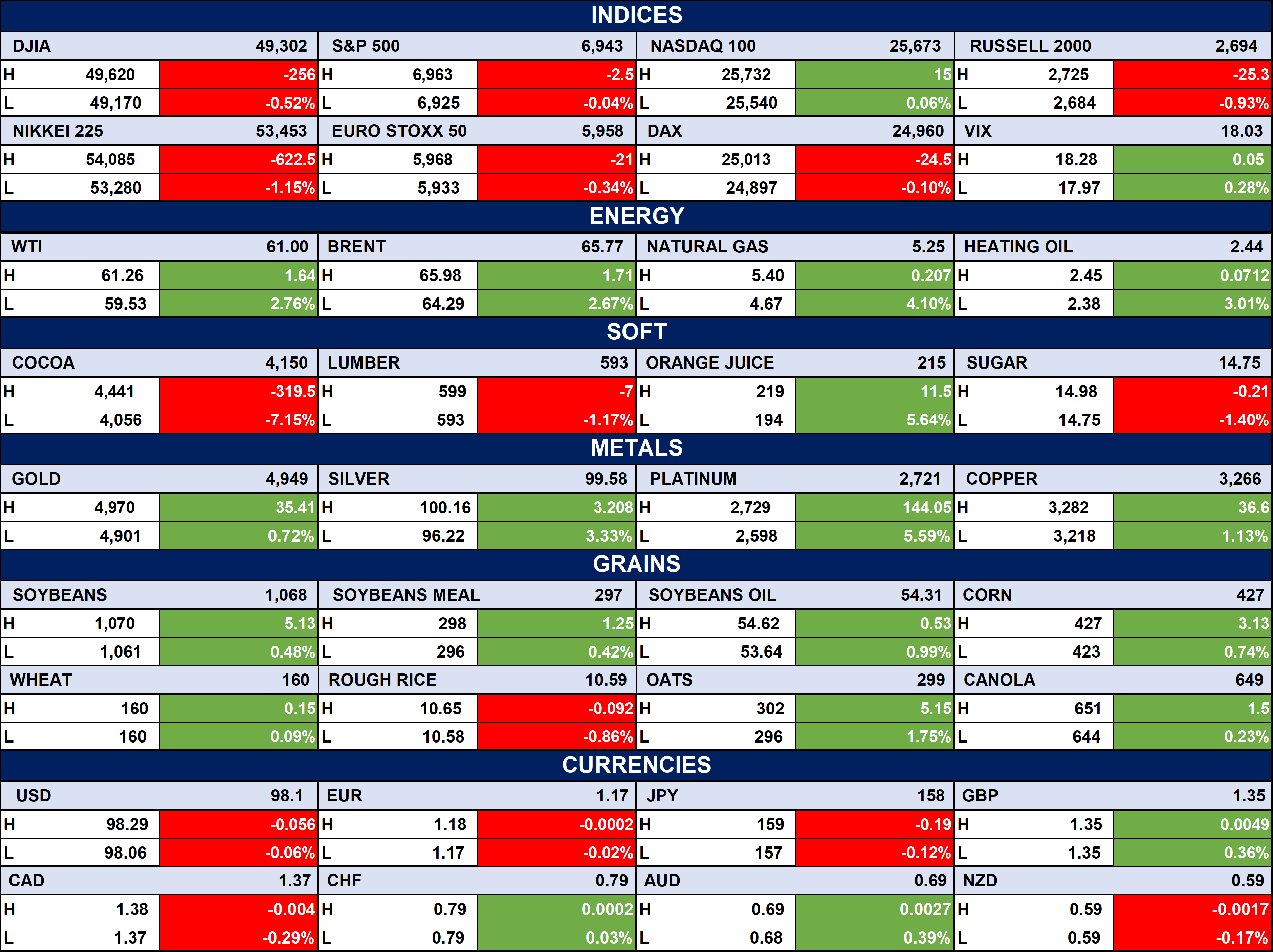

Indices, Commodities & Currencies

The table below shows that the Major U.S. indices were mixed DJIA (-0.52%) and S&P 500 (-0.04%) fell slightly, while Nasdaq 100 (+0.06%) edged higher; global indices like Nikkei 225 (-1.15%) and Euro Stoxx 50 (-0.34%) declined. Energy and metals mostly gained WTI (+2.76%), Brent (+2.67%), Gold (+0.72%), Silver (+3.33%), Platinum (+5.59%) while some soft commodities fell, notably Cocoa (-7.15%) and Lumber (-1.17%). USD softened slightly to 98.1; grains and oilseeds saw gains, e.g., Corn (+0.74%), Soybeans (+0.48%), while Rough Rice (-0.86%) and NZD (-0.17%) dipped.

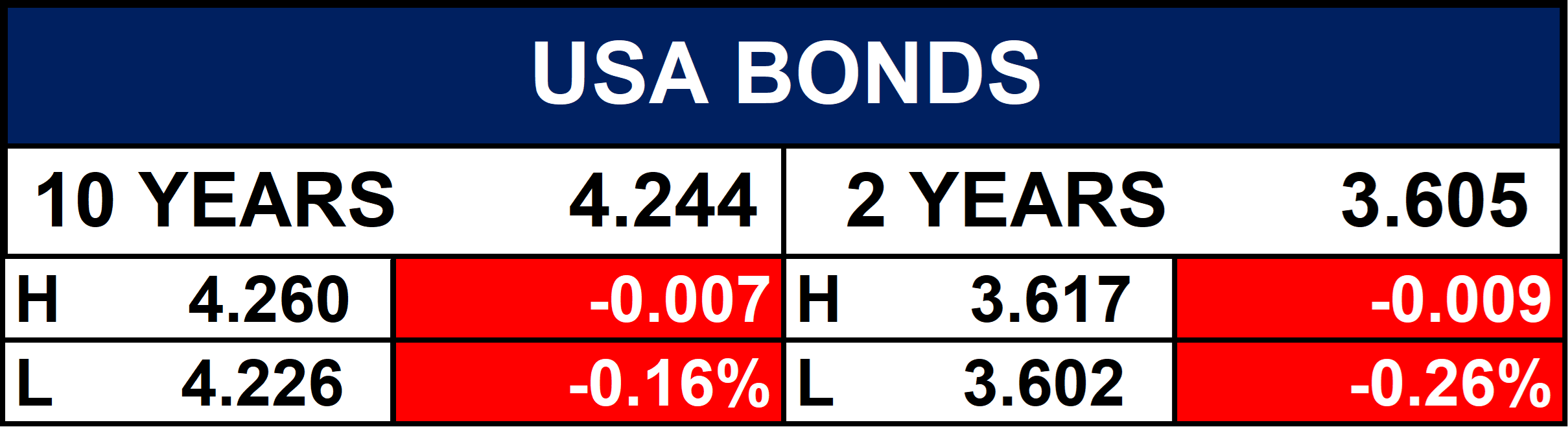

Fixed Income (USA Bonds)

Event

Conclusion

Looking ahead, investor focus may remain on Nigeria’s energy expansion, infrastructure execution, and financial sector recapitalisation, which could drive selective equity and fixed-income opportunities. Global liquidity injections, steady policy rates, and stabilising trade relations may support risk assets, though volatility could persist. Overall, markets may favour fundamentally strong sectors, especially energy, banking, and commodities, amid cautious optimism.

Thanks for reading Ranora Consulting! Subscribe for free to receive new posts and support my work.