Finance Friday — Inflation Bites, Dangote Holds the Line, Otedola Doubles Down, and the World Renegotiates Its Energy Order

Ranora Daily - Your daily source for reliable market analysis and news.

Market Overview

Good evening, Investors.

Welcome to your Close-of-Week briefing, the edition where everything clicks.

This week handed us more than headlines. It handed us a roadmap. Monday opened with the CBN draining ₦3.3 trillion from the system in a single liquidity sweep. Wednesday escalated Dangote signaled a $50 billion refinery valuation, OPEC’s demand outlook softened, and Nigeria’s oil quota miss deepened fiscal concerns. Today, Friday closes the week with a gut-punch inflation print, a billionaire doubling his banking bet, a state oil company’s stake offer getting flatly rejected, and a global trade conversation that could reshape emerging market flows entirely.

This isn’t noise. Every move this week was a signal. Let’s connect the dots.

Nigerian News & Market Update

Macroeconomy

Inflation Climbs to 15.69% - The Number That Changes the Conversation:

Nigeria’s inflation climbed to 15.69% in April. Food, transport, and energy costs all pushing in the same direction. The NBS confirmed it. The market felt it all week. Rewind to Monday: the CBN’s ₦3.3 trillion OMO sweep now looks less like routine liquidity management and more like an institution that saw this number coming. Add petrol at ₦1,350/litre and you have a full compression environment consumers squeezed, corporates under margin pressure, and one question hanging over everything heading into next week: Does this inflation print force the CBN’s hand on rates? If it does, that’s the single biggest market mover of Q2. - Leadership

Financial Services

Leadership Signals Confidence:

First Bank appointed Julius Omodayo Owotuga as Executive Director this week a clear move to reinforce leadership depth as the banking sector navigates recapitalization and strategic repositioning. - Punch

And if that wasn’t enough of a statement from the banking corridor, billionaire Femi Otedola doubled down with a ₦43 billion acquisition of additional FirstHoldCo shares. That’s not a trade that’s a declaration. Recall from Monday: the Banking Index was the week’s top-performing sectoral index on the NGX. Otedola’s move this week confirms that the smart money is watching the same signals as the market. - Channels

Energy

The Dangote-NNPC Standoff Is the Story of the Week:

Wednesday told us Dangote was eyeing a $50 billion valuation ahead of a potential listing the most ambitious capital market move in Nigerian history. Today, the story took its next turn: NNPC attempted to increase its equity stake in the Dangote Refinery. Dangote declined. Read that carefully. A refinery that is this close to a landmark public listing just turned down a state oil company’s offer to buy more of it. This is a sovereignty-of-capital moment and it signals that pre-IPO positioning has already begun. Dangote is curating its cap table. Investors should be paying close attention to what comes next. - Channels

Oil Production: Nigeria Finally Hits Its Number:

After weeks of quota underperformance flagged in Wednesday’s edition, Nigeria this week hit 99.2% of its OPEC production quota its strongest output performance in recent memory. This is not a small win. Earlier this week, production misses were framed as a compounding fiscal risk. Today’s figure suggests that the operational stability the market needed is materializing. The question now is whether this holds through Q3. - TheSun

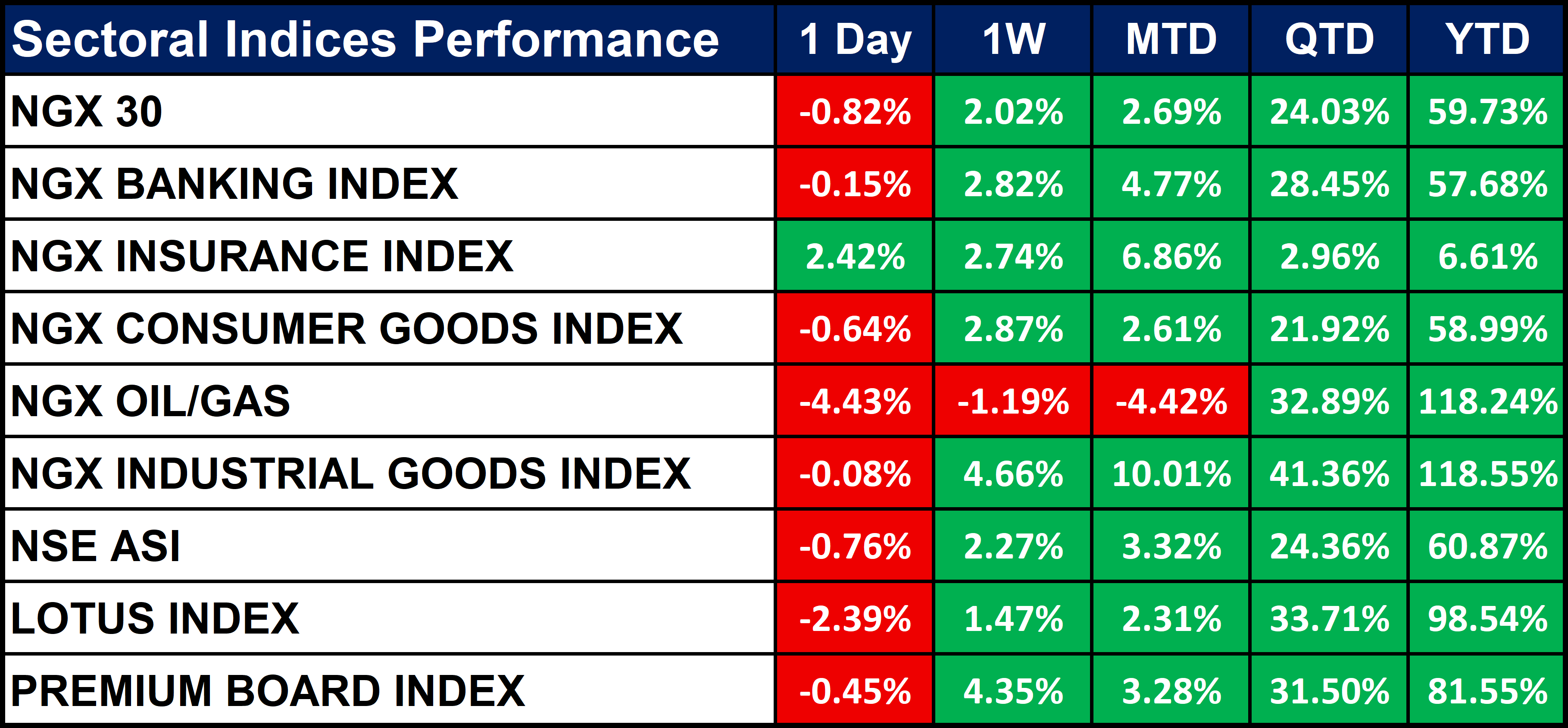

Nigeria Sectoral Indices Performance

The table below shows that the Market breadth was weak on the day, with most indices closing lower; Insurance was the key exception, gaining 2.42%, while Oil/Gas led losses at -4.43%. Weekly and MTD performance remain broadly positive, though Oil/Gas is still under pressure across both periods.

QTD and YTD returns remain strong, led by Industrial Goods and Oil/Gas, both up over 118% YTD.

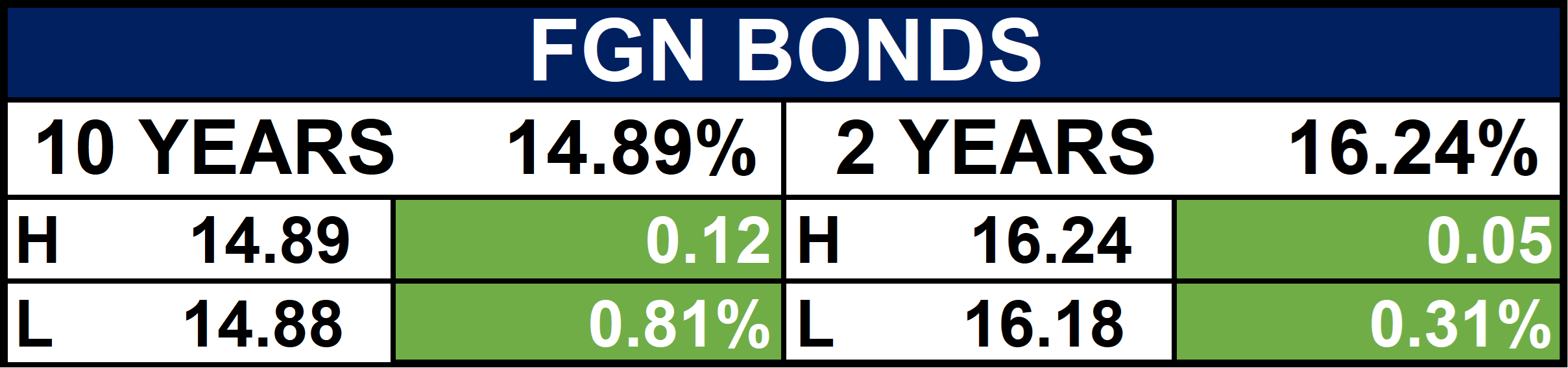

Fixed Income (FGN Bonds)

Global News & Market Update

Geopolitics (North America & Asia)

US-China: The Trade Thaw Continues:

Trump and Xi entered a second day of trade talks despite renewed Taiwan tensions. As flagged on Wednesday, a credible US-China trade thaw is a risk-on signal for emerging markets commodity prices, global trade volumes, and Nigeria's non-oil export story all stand to benefit if tariff reductions materialize. - Reuters

Macroeconomy (Asia)

Hong Kong's 5.9% Q1 Growth:

This adds weight to the Asia recovery narrative. Combined with moderating inflation in Argentina and Peru's steady-rate hold, the global macro backdrop heading into next week is cautiously constructive. - Reuters

Energy (Global)

OPEC's Supply Pivot:

Plans to restore up to 1.65 million barrels per day of previously cut output — potentially by September — creates a ceiling on oil prices just as Nigeria is hitting its stride on production. Watch crude prices closely next week. A supply-driven pullback in oil would pressure Nigeria’s fiscal position heading into the second half of 2026. - Reuters

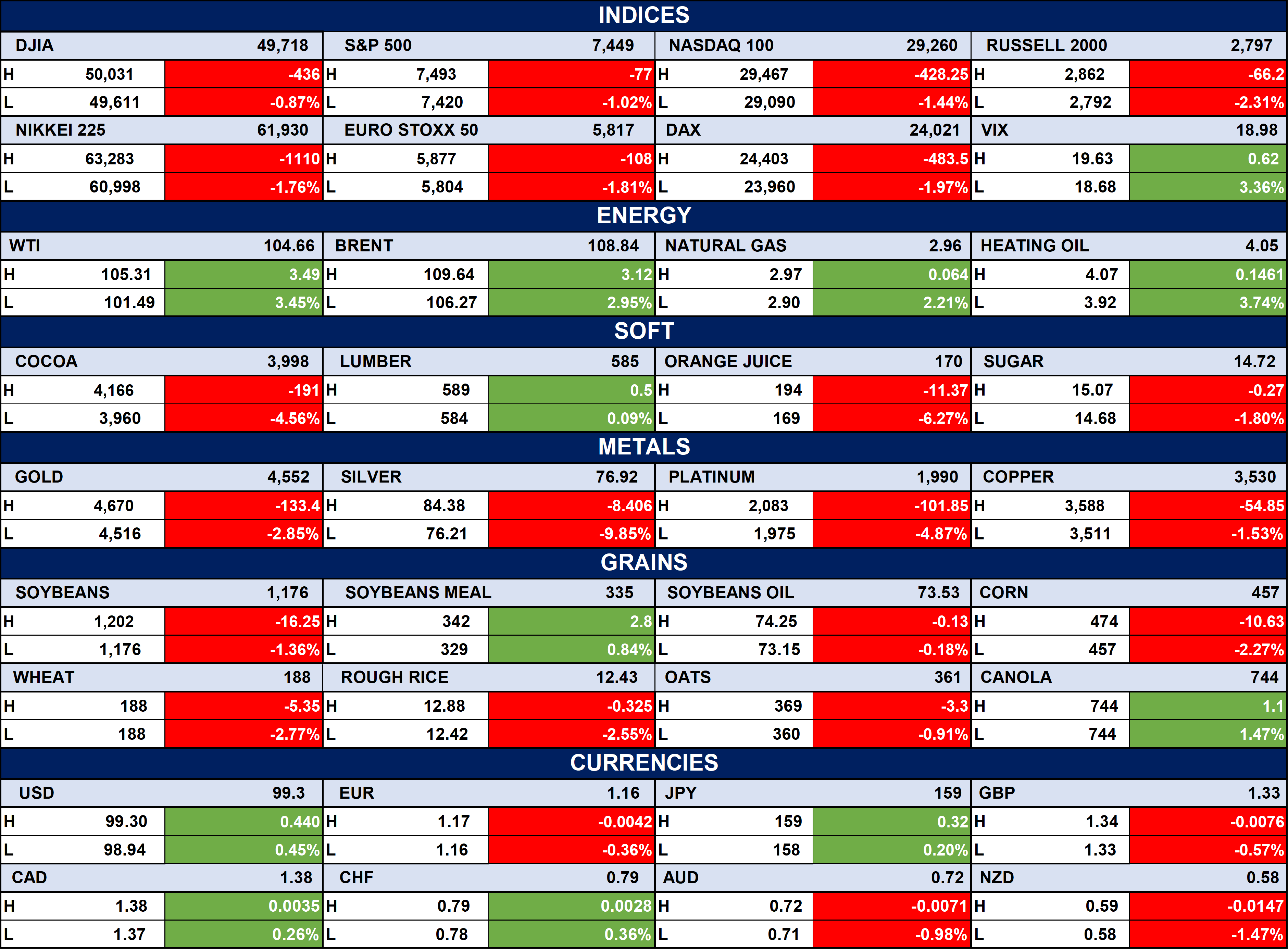

Indices, Commodities & Currencies

The table shows Equities are broadly under pressure, with major indices red across the board while the VIX rises, signaling higher risk-off sentiment.

Energy is the standout sector, with WTI, Brent, natural gas, and heating oil all posting solid gains.

Metals and most softs/grains are weaker, while currencies are mixed: USD, JPY, CAD, and CHF firm, but EUR, GBP, AUD, and NZD slip.

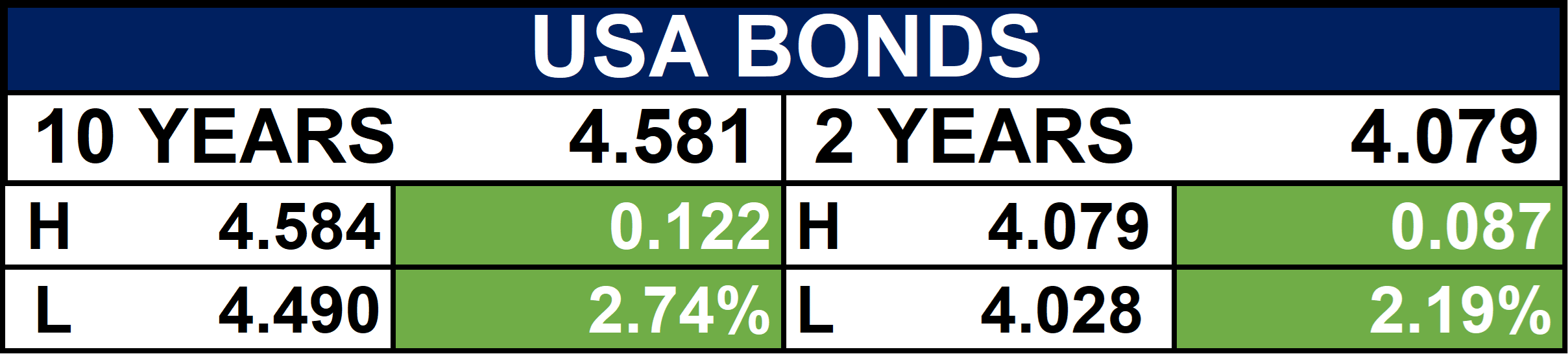

Fixed Income (USA Bonds)

Conclusion

Inflation at 15.69%. A billionaire buying billions. A refinery rejecting a state company’s advances. OPEC preparing to open the taps. Trump and Xi still at the table. This week didn’t just deliver news it delivered a matrix of forces that will define Nigeria’s market narrative well into the second half of 2026. The compression is real. But so is the opportunity if you know where to look.

The week is closed. The signals are set. We’ll be back Monday to open the next chapter.

Stay sharp. Stay positioned. Stay with Ranora.

Thanks for reading Ranora Consulting! Subscribe for free to receive new posts and support my work.