Fitch Upgrade of Nigeria to ‘B’ Stable – Implications and Impact

Ranora Daily - Your daily source for reliable market analysis and news.

Introduction

Fitch Ratings announced on April 13, 2025, that it upgraded Nigeria’s sovereign Long-Term Foreign-Currency Issuer Default Rating to ‘B’ from ‘B-’ and assigned a Stable Outlook. This one-notch upgrade, underpinned by Nigeria’s reform efforts since mid-2023, marks an important positive turn in the country’s credit trajectory. Fitch cited increased confidence in the government’s commitment to policy reforms – including exchange rate liberalization, tighter monetary policy, an end to deficit monetization, and removal of fuel subsidies – which have improved policy coherence and reduced near-term macroeconomic risks. Although the new ‘B’ rating remains in the speculative (non-investment grade) category, it signals a notably stronger credit profile than before. The upgrade has sparked discussion about its broad economic implications and how it might influence investor sentiment, borrowing costs, and capital inflows for Nigeria.

Economic Implications of the Upgrade

Fitch’s improved rating outlook reflects evolving trends in Nigeria’s economy. Key macroeconomic implications include:

Inflation Trajectory: Nigeria’s inflation remains elevated despite recent tightening. Headline CPI was 23.2% year-on-year in February 2025 (after a rebasing of the index), which is dramatically above the median of 4.3% for ‘B’-rated peers. Fitch projects inflation will average ~22% in 2025 and 20% in 2026, gradually easing but staying high relative to other ‘B’ sovereigns. The Central Bank of Nigeria (CBN) has responded with aggressive monetary tightening – raising the policy rate to 27.5% (a cumulative 875 basis points hike since early 2024) – and is expected to avoid premature rate cuts in order to cement disinflation gains. Containing inflation is crucial for sustaining any benefits of the ratings boost on the broader economy.

Growth and GDP Outlook: The reforms driving the upgrade are aimed at laying the foundation for stronger growth. While Fitch’s statement did not quote a specific GDP growth figure, it highlighted improvements in the oil and energy sector that could support economic expansion. Nigeria’s oil production (excluding condensates) is forecast to rise to ~1.43 million barrels per day (mbpd) in 2025, up from 1.34 mbpd in 2024. This modest increase, helped by improved onshore security and new investments, should bolster oil GDP – though output would still remain below pre-2019 levels due to years of underinvestment. Additionally, the Dangote Refinery’s ramp-up to an expected 0.65 mbpd capacity by mid-2025 (from 0.55 mbpd currently) means more domestic refining of fuel. Meeting domestic fuel demand internally will cut import bills (fuel had been ~30% of goods imports) and could improve industrial productivity, contributing positively to real GDP. Overall, Fitch’s upgrade suggests a belief that Nigeria’s reform-driven policies will eventually translate into a more stable and growing economy, even if tangible growth gains may materialize gradually.

Fiscal Policy and Debt: The sovereign rating upgrade comes despite persistent fiscal challenges. Fitch notes that fiscal pressures remain significant – projecting Nigeria’s general government fiscal deficit to average around 4.2% of GDP in 2025–2026. This deficit level, while not extreme by international standards, reflects rising expenditures (such as a growing public wage bill, higher interest payments, and anticipated pre-election spending) outpacing revenue growth. Nigeria’s revenue base is structurally low, and interest payments absorb roughly 30% of general government revenues (nearly 50% at the federal level), a very high ratio that constrains fiscal flexibility. Such a heavy debt-service burden – about four times the ‘B’ median interest/revenue ratio according to Fitch – has been a key weakness for Nigeria’s credit profile. The government’s reform agenda includes efforts to boost non-oil revenues and phase out costly subsidies (e.g. fuel subsidies that were abolished in mid-2023), which should gradually improve the fiscal outlook. Indeed, the removal of the petrol subsidy and exchange-rate unification were estimated by the World Bank to save the government up to ₦3.9 trillion in 2023, though these also led to short-term inflationary pain for consumers. Fitch’s stable outlook assumes the authorities will maintain a more orthodox fiscal stance – limiting central bank financing of deficits (deficit monetization) and sticking with subsidy reforms – to prevent slippage. Over time, a more sustainable fiscal path would reinforce Nigeria’s improved credit standing. However, Fitch warns that lower oil prices or any wavering on reforms could weaken fiscal metrics and test the new policy framework, underscoring that prudent fiscal management remains crucial following the upgrade.

External Accounts: Nigeria’s external position has strengthened under the reform agenda, which is a key factor behind Fitch’s improved outlook. Exchange rate liberalization and efforts to channel inflows through official markets have significantly boosted FX liquidity. Fitch highlighted that net FX inflows through official and autonomous sources rose by 89% in Q4 2024 (vs just +8% a year earlier) after the CBN introduced a new trading platform and FX code of conduct to enhance transparency. This helped narrow the gap between the erstwhile official and parallel market naira rates, restoring some confidence in the currency market. The influx of FX and reduced outflow from imports (thanks in part to domestic fuel production) contributed to a current account surplus of $6.8 billion in 2024 (about 6.6% of GDP). Fitch expects Nigeria will continue to run current account surpluses, though smaller – averaging ~3.3% of GDP in 2025–26 – as oil exports face headwinds and imports gradually pick up with growth. These external surpluses, combined with “continued formalisation of FX activity,” are forecast to keep Nigeria’s external reserves at around 5 months of current external payments coverage, slightly above the ‘B’ sovereign median of 4.4 months. Gross official reserves climbed from a low of $32 billion in mid-2024 to $41 billion by end-2024, before dipping to ~$38 billion in early 2025 due to debt service outflows (including a $1.1 billion Eurobond maturity due in November 2025). Importantly, the CBN has been reducing its off-balance-sheet FX liabilities – Fitch estimates that FX swap obligations now account for roughly 14% of gross reserves, down from 25% in late 2024 – which improves the quality of the reserve buffer. Altogether, the improved reserve position and external balances increase Nigeria’s resilience to external shocks, a fact reflected in Fitch’s upgrade. Nonetheless, risks remain: Fitch pointed out that a recently announced U.S. tariff on Nigerian non-oil exports (reportedly 10–14%) is not expected to seriously hurt Nigeria’s trade balance since oil – 92% of Nigerian exports to the US – is excluded. A bigger external risk would be a sustained drop in global oil prices, which would erode export earnings and fiscal revenues. The Stable Outlook from Fitch thus assumes that Nigeria’s external improvements will be maintained, barring a major shock, and that the naira will only see modest further depreciation in the short term under the new market-driven FX regime.

In summary, the rating upgrade reflects a judgment that Nigeria’s macroeconomic picture is stabilizing: inflation, though high, is on a downward path; growth prospects are tentatively improving with reforms in energy and forex policy; fiscal and external metrics, while still weak in absolute terms, are moving in a positive direction. The government’s reform course – if sustained – is expected to gradually tackle macroeconomic imbalances. Fitch’s endorsement may also bolster domestic confidence in these policies, creating a feedback loop that could further improve economic outcomes. Still, Nigeria must navigate the persistent challenges of high inflation and debt service, and leverage this momentum to implement deeper structural changes that support long-term GDP growth.

Market and Investor Confidence

The immediate reaction to the Fitch upgrade has been largely positive among investors and market stakeholders in Nigeria. The upgrade serves as an external validation of Nigeria’s reform progress, which can significantly boost market confidence. Local financial observers noted that the rating news “has excited stakeholders who believe it will boost investors’ confidence and positively impact the economy as a whole.”

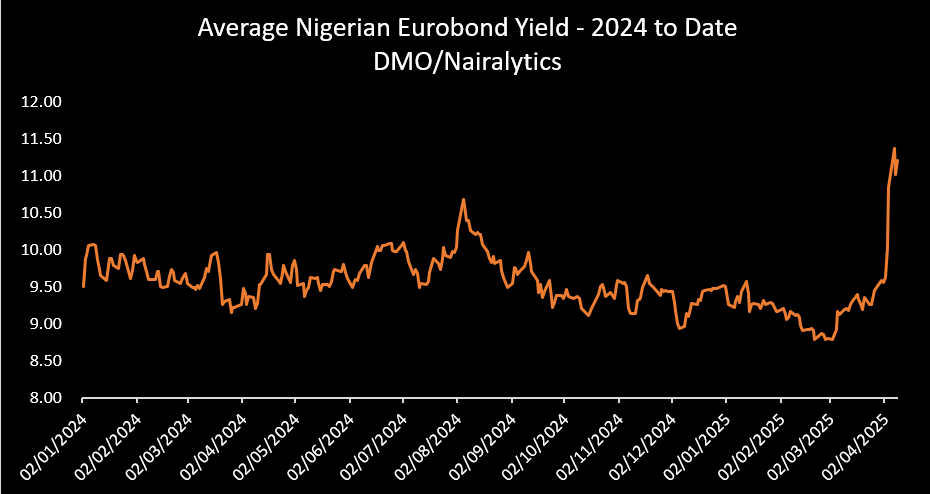

One area of impact is the bond market, particularly Nigeria’s Eurobonds, which are a barometer of international investor sentiment. Prior to Fitch’s announcement, Nigerian sovereign bonds had been under pressure from global market turbulence. In fact, in early April 2025, Nigerian Eurobond yields spiked to multi-year highs amid a broader risk-off environment: an average yield of about 9.6% at end-March surged to over 11% by April 9, 2025. This jump (yields up ~160 basis points in a matter of days) was driven by international factors – notably news of US trade tariffs that rattled emerging markets – and reflected investors demanding a higher premium for Nigeria’s debt. Such yield levels were the highest since the start of the COVID-19 pandemic, underscoring the fragility of market confidence at that time.

Figure: Average Nigerian Eurobond yield (%) from 2024 through early April 2025, showing a sharp spike in yields in April 2025. The Fitch upgrade (April 11, 2025) occurred amid this upswing, and is expected to help reverse some of the risk premium priced into Nigeria’s bonds (Data: DMO/Nairalytics).

The Fitch upgrade announcement provided a much-needed positive signal to markets, helping to counteract some of these concerns. By affirming Nigeria’s creditworthiness and stable outlook, Fitch has improved investor perception of Nigerian debt. Market analysts anticipate that the stronger rating will increase demand for Nigeria’s bonds and potentially drive yields lower. “It will boost investors’ confidence in Nigeria’s Eurobond – people would readily subscribe whenever it is issued,” explained Oladele Adeoye, chief rating officer at a Nigerian credit rating agency. Indeed, with a ‘B’ rating (versus the previous B-), a larger pool of global investors may now find Nigeria’s bonds eligible under their investment criteria, and those already holding Nigerian debt may view the credit risk as less severe. As confidence returns, sovereign bond prices should strengthen and yields fall, reducing the cost of borrowing on the international market.

Early indications following the upgrade support this optimism. Although global market conditions still influence yields, Nigeria’s credit spread is expected to tighten relative to benchmarks as the upgrade “enhances Nigeria’s global financial standing” and alleviates some default risk concerns. In practical terms, this means if Nigeria were to issue a new Eurobond in the near future, it should be able to do so at a more favorable interest rate than it would have prior to the upgrade. (Notably, reports emerged that Nigeria was hiring advisers for a potential Eurobond issue – the first in two years – as of April 2025, suggesting the sovereign may capitalize on improved sentiment to re-enter international capital markets.)

Beyond bonds, equity markets and investor sentiment toward Nigerian assets also stand to gain. A sovereign upgrade often serves as a vote of confidence in the country’s direction, which can encourage equity investors to reassess country risk premiums. While Nigeria’s stock market response in the immediate aftermath of the announcement has not been widely reported yet, the general expectation is positive. A Lagos-based stock analyst noted that the new rating “shows that the investment climate in Nigeria is very good”, which can only help equities in the long run. If foreign portfolio investors interpret the upgrade as a sign of improving stability, some who were previously cautious might increase their exposure to Nigerian stocks or local bonds. In addition, the currency market could benefit: greater investor confidence usually translates into more forex inflows, which would support the naira. Adeoye pointed out that the anticipated foreign currency inflows from a better rating “will give further room for the CBN to support the local currency and strengthen [the] exchange rate”. Indeed, a stabilization or appreciation of the naira due to renewed capital inflows would reinforce investor confidence in a virtuous cycle.

That said, analysts also caution that Nigeria’s rating, even at ‘B’, remains below investment grade, meaning global funds still perceive substantial risk. The upgrade is an encouraging step, but continued policy momentum and macro improvements will be needed to sustain investor optimism. Overall, however, Fitch’s action has clearly sent a positive signal to markets, reflected in upbeat commentary from financial experts and likely improvements in the pricing of Nigerian financial assets.

Borrowing Costs and Debt Financing

One of the most tangible benefits of a sovereign credit upgrade is the potential reduction in borrowing costs for the country. In Nigeria’s case, the move from B- to B (Stable) should translate into easier and cheaper access to financing, both internationally and domestically.

External Borrowing: The upgrade immediately impacts Nigeria’s Eurobond yields and future Eurobond issuances. As mentioned, yields on existing Eurobonds are expected to fall as investors accept a lower risk premium on Nigeria’s debt. A better credit rating can broaden the universe of lenders and investors willing to hold Nigeria’s bonds, which creates more competition and drives down the interest rates Nigeria must offer. Prior to the upgrade, Nigeria’s dollar-denominated bonds were trading at yields in the high-single to low-double digits (around 10–11% for medium-term maturities). With the new rating, these yields could compress, for example, from ~11% toward 9–10%, assuming stable global conditions. That translates to significant interest savings for the government. Crucially, if Nigeria approaches the Eurobond market for new financing, it stands to “borrow money on international markets at better interest rates.” The Nation (Nigeria) noted that thanks to the rating lift, the country now “stands a better chance of… [borrowing] at better interest rates” abroad. In effect, Nigeria’s next Eurobond could price at a tighter spread over U.S. Treasuries than it would have pre-upgrade, lowering the debt service costs for years to come. This is particularly important as Nigeria has a history of international bond issuance and will need to refinance existing Eurobonds (such as the $1.1bn due in late 2025) or raise new funds for budget support. A concrete example: if the upgrade shaves even 50-100 basis points off a new $1 billion, 10-year Eurobond’s coupon, Nigeria would save on the order of $5–10 million in interest per year compared to the higher-rate scenario.

Moreover, improved creditworthiness might open up alternative external funding sources. Multilateral lenders and bilateral creditors often take ratings into account; a higher rating can improve terms for development loans or enable greater use of policy-based lending. Even Nigeria’s Eurobond guarantees or diaspora bond programs could benefit from the perception of lower risk. Fitch’s stable outlook also signals to creditors that Nigeria’s debt trajectory is not deteriorating in the near term, which could encourage longer-term lending.

Domestic Borrowing: Although the Fitch rating mainly speaks to foreign-currency debt, it can indirectly influence domestic debt markets as well. Nigerian government bonds (denominated in naira) have yields largely driven by domestic factors – notably CBN policy rates (currently elevated) and domestic inflation expectations. However, a sovereign upgrade can reduce the “risk premium” investors demand on local bonds too, especially if it attracts foreign portfolio inflows into the local debt market. To the extent that Fitch’s move increases confidence in Nigeria’s overall stability, domestic bondholders may accept slightly lower yields. Additionally, if the government’s financing need in foreign currency can be met more externally due to the upgrade, there may be less crowding-out in the local credit market. A Nigerian rating agency expert highlighted that “good [sovereign] rating also implies lower cost of fund” generally. In recent years Nigeria’s local bond yields have been quite high (often in the mid-teens percent) to compensate investors for inflation and currency risk. A stronger credit profile and improving FX outlook could lure more foreign investors back to naira bonds, which drives yields down. As those yields decline, the government’s domestic borrowing (e.g. Treasury bills, FGN bonds) becomes cheaper, easing the debt service burden on the budget. Thus, while the effect may not be immediate or as pronounced as on Eurobonds, Nigeria’s domestic cost of capital is likely to improve modestly in the wake of the Fitch upgrade.

It’s also worth noting that Nigeria’s overall debt management strategy could get a boost. The Debt Management Office (DMO) may seize this opportunity to rebalance debt by issuing longer-term bonds or refinancing expensive short-term debt. If market conditions permit, Nigeria might even consider a liability management exercise (for example, swapping or buying back some costly debt) to capitalize on improved spreads. Each percentage point reduction in interest rates can free up fiscal space for other priorities.

In summary, the Fitch upgrade is “expected to … reduce borrowing costs” for Nigeria, as cited in one media report, by improving lenders’ perceptions of the country. This will be crucial for a nation that has seen its debt servicing costs surge in recent years. Lower borrowing costs directly complement the government’s reform efforts – for instance, savings from cheaper debt can be redirected to development projects or social spending, reinforcing economic growth and, by extension, future creditworthiness. The challenge will be to maintain the policies that earned the upgrade so that borrowing costs continue to trend downward over time.

Foreign Direct Investment and Portfolio Inflows

A sovereign credit upgrade often serves as an encouraging green light for various forms of international investment. In Nigeria’s case, the move to ‘B’ stable is expected to stimulate greater foreign direct investment (FDI) and portfolio inflows, as it signals a lower-risk, more stable investment environment.

Even before the upgrade, Nigeria’s recent reforms were beginning to rekindle foreign investor interest. The CBN reported a significant uptick in capital inflows in late 2024, attributing it to improved economic fundamentals and confidence. According to the CBN, Nigeria registered a Balance of Payments surplus of $6.83 billion in 2024, a stark turnaround from deficits of over $3 billion in each of the two prior years. This swing to surplus was driven in part by “renewed investor confidence in Nigeria’s economy” and stronger trade performance, as noted by the central bank. In particular, the unification of exchange rates and removal of the fuel subsidy in mid-2023 sent a positive signal to foreign investors that Nigeria was serious about addressing long-standing distortions. Fitch’s upgrade effectively validates this progress, which could encourage longer-term foreign investments that had been on hold.

Foreign Direct Investment (FDI): An improved sovereign rating can bolster FDI by enhancing Nigeria’s image as a stable destination and by lowering the perceived sovereign risk which often factors into business decisions. The upgrade to ‘B’ stable might not immediately flood Nigeria with new factories or infrastructure projects, but it adds momentum to the government’s pitch to investors. A stock market analyst, Peter Adebola, observed that the Fitch rating demonstrates a stable investment outlook for Nigeria and “can have a positive effect on our foreign direct investments… [it] shows that Nigeria is a good investment destination.”. In practical terms, multinational companies may view the upgrade as a sign of improving macro stability (important for planning and profitability), and it might tip the scales for companies considering entering Nigeria or expanding existing operations. Sectors like energy, manufacturing, and technology – which the government has been keen to attract investment into – could see greater interest. It’s also likely that Nigeria’s authorities will leverage the upgrade in investor roadshows and marketing materials to showcase the country’s reform success, potentially helping to conclude FDI deals. However, FDI decisions also depend on microeconomic factors (like ease of doing business, security, infrastructure), which Nigeria must continue to work on. The rating upgrade is one piece of the puzzle that enhances Nigeria’s credibility in the eyes of foreign businesses and could combine with other initiatives (such as recent tax and fiscal reforms) to make Nigeria more attractive for direct investment.

Portfolio Inflows: The upgrade’s impact on foreign portfolio investment (FPI) – such as foreign purchases of stocks, local bonds, and money market instruments – is likely to be more immediate. Portfolio investors are usually quite sensitive to ratings and will adjust their allocations according to risk and return. With Nigeria now rated ‘B’ (stable) by Fitch, some global fund managers who have internal rating floors might increase their exposure to Nigerian assets. For instance, certain emerging-market bond funds might have been underweight Nigeria when it was B- due to risk limits; those could rebalance to a neutral or overweight position now. Local financial experts explicitly predict an inflow of foreign currency into the economy on the back of the improved rating, as global investors respond to Nigeria’s enhanced standing. Such inflows are likely to go into government securities (to take advantage of still-high yields with lower risk) and possibly into equities if growth prospects brighten. As noted earlier, even a moderate inflow can have beneficial side effects: supporting the naira, increasing liquidity, and lowering local interest rates. Nigeria experienced large portfolio outflows in past years due to forex restrictions and repatriation concerns; the moves to liberalize FX (now endorsed by Fitch) and the rating upgrade together may persuade some investors that those issues are being resolved.

There are already concrete signs of returning foreign investor interest: J.P. Morgan, a major US financial institution, has applied for a merchant banking license in Nigeria to upgrade its presence from a representative office to a full branch. This would allow J.P. Morgan to lend directly in Nigeria (e.g. providing dollar loans to corporations) and is a strong vote of confidence in Nigeria’s financial sector reforms. While this move was likely in motion before the rating change, it aligns with the narrative of renewed engagement by international players. Likewise, the World Bank’s commitment of $16 billion across 28 projects (announced in April 2025), though not an investment in the private sense, underscores international institutions’ support for Nigeria’s development – which often encourages private investors to follow suit, knowing that the country has backing for infrastructure and policy support.

It is important to temper expectations: Nigeria’s rating, at ‘B’, is still below investment grade, so many conservative institutional investors (such as pension funds or insurance companies in developed markets) will still classify Nigerian securities as high-risk. Moreover, FDI decisions particularly can take time to materialize. Nonetheless, the upgrade strengthens the argument that Nigeria’s trajectory is improving, which can only help in attracting both “foreign investment and portfolio inflows” over the coming months. Maintaining political stability and continuing the reform agenda will be key to converting this ratings milestone into tangible investment on the ground. If those investments do come, they can create jobs, bring in new technologies, and diversify Nigeria’s economy – outcomes that would validate Fitch’s optimism and potentially lead to further positive rating actions in the future.

Reactions from Domestic and International Institutions

The Fitch upgrade of Nigeria’s sovereign rating has elicited reactions from both domestic authorities and international observers, generally applauding the development while acknowledging the work ahead.

Government and Central Bank (Domestic): Nigerian officials have welcomed Fitch’s decision as a validation of the economic reforms undertaken by the current administration. Although, as of this writing, an official press release from the Federal Ministry of Finance or the Presidency has not been published, the sentiment in government circles is clearly positive. The CBN, in particular, has been vocal about the success of recent policies. At an international trade forum, CBN representatives highlighted that wide-ranging macroeconomic reforms and renewed investor confidence are strengthening the Nigerian economy, evidenced by the return to a BoP surplus in 2024. The CBN’s Acting Director of Corporate Communications, Mrs. Hakama Sidi Ali, noted that foreign direct and portfolio investments have significantly increased, attributing this to the current management’s efforts to address macroeconomic challenges. Such comments, coming around the time of the Fitch upgrade, reinforce the bank’s message that the reforms (many of which the CBN helped implement, like the FX market liberalization) are bearing fruit. It wouldn’t be surprising if the Finance Minister and other officials echo these points in upcoming media briefings, emphasizing that Fitch’s upgrade is proof that Nigeria is moving in the right direction and urging continued support for the reform agenda. There is also a sense of cautious pride – as expressed by members of Nigeria’s financial community – that “the Fitch rating ‘means a lot.’ It is solid, it is stable, it is progressing”, in the words of the head of Nigeria’s Institute of Credit Administration. This reflects an understanding that while challenges remain, the country has turned an important corner.

Local economic experts have also weighed in. Many see the upgrade as an opportunity for Nigeria to double down on reforms. For example, analysts have urged the government to “step up efforts” to boost productivity, exports, and revenue collection in order to capitalize on the improved rating. The overarching domestic view is that the upgrade is a positive signal that should translate into concrete economic gains if Nigeria stays the course. There is also recognition that Nigeria is still rated “highly speculative” – a reminder that policy complacency could reverse these gains. This perspective is healthy, as it frames the Fitch decision not as a laurel to rest on, but as motivation to tackle remaining issues (like power supply, infrastructure, and security, which commentators mention need continued work).

International Organizations and Partners: The international community has generally reacted favorably to Nigeria’s improved credit standing, seeing it as indicative of successful reforms. The World Bank swiftly followed the Fitch announcement with news of its own: a commitment of over $16 billion in financing for Nigeria across dozens of active projects. While this commitment was likely in the pipeline, the timing (announced just after the rating upgrade) and the scale of support underscore a vote of confidence. The World Bank’s regional vice president was scheduled to visit Nigeria in mid-April 2025 to discuss economic recovery and job creation – topics likely buoyed by the positive ratings news. Such high-level engagement suggests that multilateral institutions view Nigeria’s reform momentum favorably. Indeed, these institutions have been advocating many of the same reforms (exchange rate unification, subsidy removal, fiscal consolidation) that Fitch applauded. For instance, the IMF in its last Article IV consultations commended Nigeria’s “ambitious reform path” and projected significantly improved fiscal outcomes if reforms are sustained. The IMF and World Bank have, however, also cautioned about the short-term hardships from these reforms – noting issues like high inflation and the need to strengthen social safety nets. With the Fitch upgrade, one can expect the IMF and others to encourage Nigeria to leverage the improved market sentiment to possibly undertake further beneficial steps (such as phasing out remaining distortions, improving governance, and addressing debt vulnerabilities). They are also likely to use Nigeria as a reform success example to other countries, given how quickly the ratings outlook improved after difficult policy changes were made.

Another set of important international actors are global rating agencies and financial analysts. S&P Global Ratings had earlier (August 2023) revised Nigeria’s outlook to stable from negative, citing the Tinubu government’s swift reforms and the expectation of gradual benefits to growth and public finances. S&P’s move, while keeping Nigeria at B-/B, presaged Fitch’s more recent upgrade. Now that Fitch has taken the leap, there may be speculation on whether Moody’s (which downgraded Nigeria to a very low Caa1 in late 2022 amid debt concerns) will consider an upward move or at least a outlook revision, if Nigeria’s fiscal and external improvements continue. Such a development would further solidify international confidence. Global banks and investment houses have also commented: many have released notes to clients highlighting Nigeria’s improved outlook. J.P. Morgan’s interest in expanding in Nigeria has already been mentioned, and other banks could follow suit or increase Nigeria’s weight in their emerging market portfolios.

In summary, domestic institutions like the CBN and Nigerian analysts have hailed the Fitch upgrade as a positive endorsement of reform policies, using it to bolster public and investor confidence. International organizations and financial stakeholders have likewise reacted by reaffirming support – whether through funding commitments or analytical coverage – while advising Nigeria to stay vigilant on remaining challenges. The broadly favorable commentary suggests that Nigeria’s reputation among the global economic community has improved. The government can leverage this goodwill in diplomacy and economic partnerships, translating the ratings win into real development benefits. Importantly, the upgrade and its reception send a message to the Nigerian public as well: that difficult reforms can yield tangible rewards in terms of international trust and economic opportunities. Keeping that public support will be essential as Nigeria navigates the next steps of its economic transformation.

Conclusion

Fitch’s upgrade of Nigeria’s sovereign rating to ‘B’ with a Stable Outlook marks a significant milestone, reflecting the country’s progress in stabilizing its economy through bold policy reforms. The economic implications are encouraging – policy credibility has improved, inflation is expected to gradually moderate (though vigilance is needed), and external and fiscal indicators are on a mend albeit from weak starting points. The rating boost has in turn galvanized investor confidence, which should lower borrowing costs for the government and possibly spur new investments. Nigeria now finds itself in a better position to access international capital on more favorable terms and attract foreign capital inflows to fuel growth. Early reactions from markets and institutions show a renewed optimism about Nigeria’s prospects, coupled with an understanding that sustaining this momentum is key. To fully realize the benefits of this upgrade, Nigeria will need to continue along the reform path – strengthening its fiscal position, keeping inflation on a downward trend, and fostering an environment conducive to business and investment. If it can do so, the country’s economic trajectory and credit standing could improve further, creating a virtuous cycle of stability and growth. Fitch’s endorsement is a welcome development for Nigeria, and with prudent management, it can be a stepping stone towards even greater financial resilience and economic prosperity for Africa’s largest economy.