Impact of Nigeria’s CPI Rebasing on Local Bond Yields (Short, Medium & Long Term)

Ranora Daily - Your daily source for reliable market analysis and news.

Nigeria’s recent rebasing of its Consumer Price Index (CPI) has significant implications for inflation, interest rates, and bond yields across different tenors. In January 2025, the National Bureau of Statistics updated the CPI basket and base year from 2009 to 2024 – the first rebase in over a decade.

This statistical change lowered the official inflation rate dramatically (without an actual drop in prices) and is influencing investor behavior and monetary policy expectations. Below, we analyze the short-, medium-, and long-term effects on bond yields, covering inflation expectations, central bank policy, yield curve shifts, foreign investor flows, historical comparisons, and expert forecasts.

Inflation Expectations and Investor Sentiment

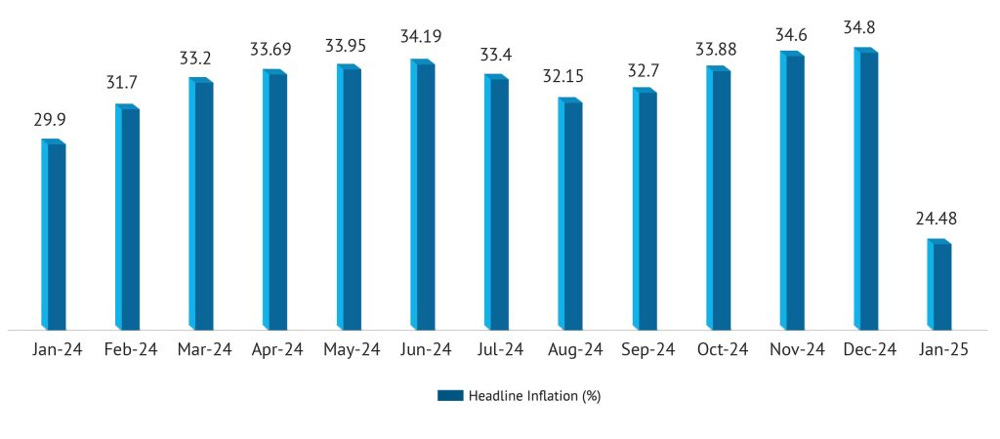

Post-Rebasing

Nigeria’s headline inflation fell from 34.8% in Dec 2024 to 24.5% in Jan 2025 after rebasing.

The chart shows monthly inflation (% YoY) before and after the new CPI base year (2024).

The CPI rebasing immediately reduced measured inflation from 34.8% in December 2024 (old methodology) to 24.5% in January 2025 (new methodology). Food inflation saw a similar decline from ~39.8% to 26.1%. This large statistical drop surprised many in financial markets – analysts did not expect such a big difference in the headline rate. While the rebasing hasn’t made actual prices cheaper overnight, it altered inflation expectations: investors now anticipate a lower trajectory for reported inflation in the near term. Standard Chartered’s chief economist for Africa, Razia Khan, noted that January’s much lower figure “potentially opened the door” for an interest rate cut, signaling that markets immediately viewed the rebased data as reason to expect easier monetary policy ahead.

From an investor sentiment perspective, the rebasing has been largely positive. With official inflation lower, the real return on Nigerian bonds looks more attractive, boosting confidence. Market commentary highlighted “improved inflation outlook” rekindling interest among both domestic and international investors. In effect, the perception that inflation is moderating (even if largely due to methodology) has made investors more bullish on fixed-income assets. Many see the change as a turning point, expecting that inflation will be better contained going forward and that monetary tightening has peaked

This optimism spurred a rally in the bond market, as detailed below, with investors eager to lock in high yields before any future interest rate cuts. It’s worth noting that some analysts urge caution in interpreting the new data. The Statistician-General emphasized that the drop is statistical and “not saying prices have come down” in reality.

Nonetheless, sentiment shifted markedly: investors flocked to bonds to capitalize on improved inflation-adjusted returns, even if underlying price pressures remain. Overall, the rebased CPI has tempered inflation fears in the short term and boosted investor confidence, creating a more favorable mood in financial markets.

Expected Central Bank Reaction and Monetary Policy

The Central Bank of Nigeria (CBN) has reacted cautiously to the rebased inflation figures. At its first Monetary Policy Committee (MPC) meeting after the rebase (February 2025), the CBN held the benchmark interest rate at 27.5%, opting to wait and assess the new data rather than rush into policy changes. Governor Olayemi Cardoso acknowledged that rebasing “lowered reported inflation rates, even though underlying price pressures remain high”. In other words, the CBN recognizes the cosmetic improvement but is mindful that true inflationary pressures (e.g. food and fuel costs) are still elevated.

Why the caution? Policymakers face a dilemma: continued tight policy could hurt a fragile economy, but a premature rate cut might reignite inflation. Analysts note that inflation is “at an inflection point but could pick up again in a few months,” so the MPC will likely wait for a few months of data to validate the downtrend before any major moves. Essentially, the CBN wants to ensure the lower inflation is sustained (and not solely a statistical artifact) before easing. The MPC would probably hold off on cuts for at least one or two more meetings (a few months) to “assess the rebased numbers”.

That said, the rebasing has certainly opened room for a policy pivot sooner than previously expected. With inflation now officially in the mid-20s (rather than mid-30s), the pressure to keep ultra-high rates has somewhat eased. Even at 27.5%, Nigeria’s real policy rate is mildly positive (+3% by new inflation) – a stark change from a deeply negative real rate pre-rebasing. This gives the CBN breathing space to consider rate cuts to support growth. Razia Khan suggested even a token 25 bp cut could be conceivable to acknowledge that policy was very tight. While the February meeting did not deliver a cut, expectations of future easing have grown louder

In the short term (next 1-3 months): the CBN is likely to maintain a holding pattern – no hikes (given inflation appears lower) but no significant cuts yet until trend clarity emerges.

In the medium term (mid-2025): if rebased inflation continues to moderate or at least doesn’t spike, the CBN could cautiously begin an easing cycle, reducing the policy rate in small increments. The central bank has hinted that “a sustained decline in inflation may enable a dovish pivot to stimulate growth,” whereas any renewed upward creep will prolong tightening.

By the long term, assuming the new CPI methodology leads to better-anchored inflation around low double-digits, the CBN would be aiming for a lower interest rate environment than the crisis levels of 2023–2024. However, structural issues (food supply, FX volatility) mean policy will remain data-dependent and cautious.

In sum, the rebasing has shifted CBN’s stance from outright inflation-fighting to a more balanced approach, delaying further hikes and bringing forward the timeline for eventual rate cuts (contingent on inflation’s path).

Short-Term vs. Medium/Long-Term Government Bond Yields

Immediately after the CPI rebase, Nigeria’s yield curve experienced a notable downward shift, especially at the short and medium ends. Investors aggressively bought government securities, driving yields lower across maturities as they priced in a better inflation outlook and potential monetary easing.

Short-term (T-Bills): Yields on Treasury bills fell sharply in the February 2025 auction following the inflation release. The 91-day T-bill stop rate dropped from 18% to 17%, and the 182-day fell from 18.5% to 18.0%. Most dramatically, the 1-year (364-day) T-bill yield declined from about 20% to 18.43% – a six-month low. This ~1.5–2 percentage point drop in short yields reflects investors’ surging demand for short-tenor paper, anticipating that the CBN might cut rates in the coming months. In fact, the auction was massively oversubscribed (total bids far exceeded the amount offered), allowing the government to borrow at much lower rates. An expert noted that part of the one-year bill’s yield crash was technical – the CBN sold far less than the maturing volume, so bidders accepted lower yields to get an allocation (nairametrics.com). Nonetheless, it’s clear that short-term yield expectations have reset lower on the back of the new inflation data and sentiment that the peak of tight monetary policy is past.

Medium- to Long-term (FGN Bonds): Yields on mid- and long-term government bonds also declined significantly, although the magnitude varied by tenor. In a February 2025 bond auction, 4- to 6-year FGN bonds cleared at roughly 19.2–19.3%, down from yields above 21–22.5% in the previous auction. For example, the April 2029 bond came in at 19.20% (vs 21.79% prior) and the Feb 2031 at 19.30% (vs 22.50% prior). This 2–3 percentage point drop in medium-term yields is a direct consequence of investors’ “growing expectations” of a more accommodative MPC stance as inflation pressures recede. In secondary trading, benchmark bond yields also trended down. Market yields on 2027–2033 bonds fell by ~20–30 basis points on average immediately after the rebased CPI was published. By some reports, the average yield on government bonds pulled back to around 20% following the CPI news (down from roughly 21–22% pre-rebasing). This broad rally flattened the yield curve somewhat. The short and mid segments saw the strongest buying, with yields on 2–5 year bonds compressing more, while the longest end (10+ year) moved less. Traders noted, for instance, the 2035 bond yield fell by nearly 0.95% (95 bps) in the aftermath, indicating even long-tenor bonds attracted interest as investors repositioned for potential rate cuts

Overall, the yield curve shifted downward in the short term, with yields easing across all maturities. Short-term T-bills, which had been exceptionally elevated, are now closer to the high-teens, and medium-tenor bond yields have also converged to the high-teens. The curve remains relatively steep in absolute terms (reflecting Nigeria’s still-high inflation and risk premiums), but the gap between short and long yields has narrowed. Prior to rebasing, short-term yields above 20% were actually higher than some longer bond yields (an inverted to flat curve due to tight liquidity and inflation fears). Post-rebasing, we see a more normal upward slope: e.g. 1-year around 18.4% vs 5-year around 19–20%. This suggests the market is pricing in lower short-term rates ahead (hence short yields fell more), while longer-term yields still embed caution about inflation in the years to come.

Short Term Outlook: In the immediate months, we expect continued high demand for short-term bills, which could keep T-bill yields in the mid-to-high teens. If the CBN holds policy steady or delivers a minor cut, short yields may inch down a bit more. Medium Term: As the year progresses, the trajectory of inflation will guide yields. If rebased inflation remains relatively lower or keeps slowing, bond yields could gradually decline further. Some research houses forecast yields to moderate to ~18% by end-2025, assuming inflation stabilizes under the new index. For instance, Cordros Research predicts 1-year T-bill and long bond yields could settle around 18.5% and 18.0%, respectively, by late 2025 under a stable inflation scenario (businessday.ng). However, if underlying price pressures re-emerge (say food or energy prices push inflation up again), investors may demand higher yields, and we could see an uptick. Long Term: Longer-dated Nigerian bonds will continue to price in structural inflation and currency risks. Persistent reforms (fiscal prudence, exchange rate stability) would be needed to anchor long-term inflation in lower ranges. Should that happen, a secular decline in yields is possible over years (perhaps moving toward low- to mid-teens). But if inflation expectations worsen or fiscal deficits widen, the yield curve could shift back up, undoing some of the post-rebasing gains. For now, the consensus is that yields have likely peaked in late 2024 and, barring shocks, will stay below those highs due in part to the improved inflation metrics.

Foreign Investor Interest and Portfolio Flows

Nigeria’s improved statistics – a lower inflation rate and even a recently rebased GDP (making the economy appear larger) – are catching the eye of foreign investors. The bond market rally post-CPI rebasing was not just driven by locals; global investors also increased their participation. The combination of high nominal yields and a sharply lower inflation print makes Nigerian government bonds more attractive in real terms. Investors from advanced economies facing much lower yields see an opportunity for higher returns. As one analysis noted, Nigerian bonds now offer yields that “compare favorably to other emerging market instruments”, especially with the prospect of capital gains if interest rates fall.

Indeed, foreign portfolio inflows have shown signs of picking up after the rebasing. In a primary auction in February, the Debt Management Office received an enormous N1.2 trillion in bids for FGN bonds (over 4x the amount offered), reflecting surging demand. Market observers reported that a significant portion of these bids came from foreign portfolio investors repositioning into Nigerian fixed-income assets. The high bid-to-cover ratio (about 4.7x in that auction) underscores the renewed risk appetite for Nigeria’s debt

Several factors drive this foreign interest:

Improved macro indicators: The rebased inflation figure gives confidence that Nigeria is turning a corner on macro stability. Along with other reforms (fuel subsidy removal, exchange rate unification), it paints a picture of a government serious about economic reset. Rating agencies have taken note – for example, Moody’s recently maintained Nigeria’s credit rating outlook as positive, citing reform momentum.

Higher Real Yields: Even though inflation is still high at 24%, Nigeria’s policy rate (27.5%) and bond yields ~18–20% now imply a less negative or near-zero real yield environment, versus deeply negative real yields before. This, combined with expectations of disinflation, suggests potential for real yield to turn positive, a key attraction for foreign investors seeking carry. In comparison, many developed markets have near-zero or negative real yields, so Nigeria stands out.

Currency Outlook: There are tentative signs of currency stabilization, which is crucial for foreign investors (who fear being unable to repatriate returns). The rebasing and broader economic reforms have slightly boosted confidence in the naira. Observers noted the naira saw some appreciation on the parallel market amid rising investor optimism. If Nigeria’s FX management continues to improve, it could unlock more portfolio inflows, as investors feel safer that high yields won’t be eroded by FX losses.

Going forward, portfolio flows are expected to increase provided the new inflation data remains credible and Nigeria navigates its reforms well. A senior investment advisor commented that Nigeria may be viewed as having a stronger debt repayment capacity with a larger GDP and lower inflation, which “could make Nigerian bonds more attractive to investors” (cnbcafrica.com). However, sustained foreign interest will also depend on on-the-ground realities: e.g., if inflationary pressures resurge or if there are FX liquidity issues, foreigners could pull back. For now, post-rebasing, Nigeria is seeing a moment of renewed foreign confidence, with early indications of rising portfolio inflows into bonds and even equities (as evidenced by a bullish stock market in early 2025 alongside bond rally). This is a reversal from the outflows of previous years when inflation and currency worries were dominant.

Comparison with Past Rebasing in Nigeria and Other Emerging Markets

Rebasing a price index is not unique to Nigeria – many emerging markets periodically update their CPI basket. However, the magnitude of Nigeria’s inflation drop after rebasing in 2025 is unusual. Historically, CPI rebasing often leads to only modest changes in reported inflation, and in some cases even an increase, depending on how weights shift.

Nigeria’s Past CPI Rebasing: Nigeria had not rebased its CPI since 2009, which is why the 2025 update had such a pronounced effect. In prior instances (e.g., if we go back to when the base was changed to 2009), the change in inflation rate was much smaller. In fact, analysts noted that Nigeria (like Kenya) previously saw little change in inflation due to rebasing. This suggests that the 2025 rebase – coming after 15+ years – corrected a lot of “historical bias” in the old index, yielding a larger one-time adjustment. The old basket over-weighted items (like food and fuel) whose prices had spiked, thereby overstating inflation, according to the NBS. By reducing food’s weight from ~52% to 40% and increasing weights of housing, transport, etc., the new CPI better mirrors current spending. This drove the headline rate down. The key point is that Nigeria’s case is an outlier in size of impact because the base year was extremely out-of-date (supposed to be updated every 5 years, but delayed since 2009).

Other Emerging Markets: Experiences have varied. For example, South Africa rebased its CPI multiple times (most recently to base 2021) and typically saw minimal impact – the inflation rate changed by only –0.2 percentage points after one rebase. Kenya’s last rebase lowered inflation by about 1.5 points. On the other hand, Ghana’s CPI rebasing in 2019 (updating base from 2012 to 2018) actually increased the measured inflation by roughly 6.9 percentage points. This can happen if rapidly-rising items gain more weight in the new basket. Uganda also saw a jump (from 2.3% to 2.7% inflation) after shifting its base year. These examples show that rebasing can either raise or lower the headline number – it’s a statistical realignment to consumption patterns. The direction and scale of change depend on how the economy’s spending mix evolved. In Nigeria’s case, the shift toward more weight on services (which had lower inflation) and less on food/energy (which had higher inflation) produced a big downward revision.

In summary, compared to peers, Nigeria’s 2025 CPI rebase had an outsized effect, drastically lowering reported inflation. Past Nigerian and Kenyan rebase episodes didn’t substantially alter the trend, whereas some countries like Ghana experienced higher inflation after rebasing. This context is important: it tells investors and policymakers to interpret Nigeria’s new inflation numbers with care – the drop is a recalibration, not a sudden victory over inflation. It also means historical comparisons of Nigerian inflation need to be adjusted, as pre-2025 and post-2025 data are not directly equivalent (effectively “measuring with different rulers” as one report put it (agusto.com).

Expert Opinions and Forecasts

Economists and market analysts have offered a range of insights on what the rebased CPI means for Nigeria’s economic trajectory and bond market:

Razia Khan, Standard Chartered – Emphasized the surprise in the size of the drop and immediately flagged the possibility of a rate cut due to the lower inflation figure. Khan suggested even a small cut would send a signal that policy tightening had been overdone, given local sentiment that rates were too high (reuters.com).

Basil Abia, Veriv Africa – Advises caution, noting that inflation could creep up again. He expects the CBN to hold off major policy changes for a quarter to see if the low inflation is sustained (techcabal.com). His view underscores that the central bank should validate the trend before easing, to avoid whipsawing if “statistically lower” inflation drifts upward later.

Egie Akpata, Skymark Partners – Points out technical factors in the bond rally. He explained that the significant drop in 1-year T-bill yields was partly due to lower supply, as the CBN rolled over far less than maturities (nairametrics.com). This suggests not all the yield decline is due to rebasing euphoria; market mechanics played a role. Going forward, Akpata implies yields could adjust if issuance increases.

Emmanuel Odiaka, Ecob Capital – Believes the rebased GDP and CPI improve Nigeria’s investment case. He expects bond and T-bill yields to “adjust depending on inflation trends post-rebasing”. If inflation indeed stays lower, yields may fall; if not, they could readjust upward. He also noted that Nigeria’s larger GDP base post-rebasing boosts creditworthiness perception, which “could make Nigerian bonds more attractive” to foreign investors (cnbcafrica.com).

Cordros Securities Research – Forecasts that if inflation stabilizes around the lower levels, yields will moderate to the high-teens by end-2025. They project ~18% yields for government bonds, but caution that continued naira depreciation or high energy costs could keep yields elevated above that (businessday.ng). In essence, their base case is some further easing of yields, but risks (FX, oil prices) could limit the decline.

Rating Agencies – While not issuing forecasts on yields, agencies like Moody’s and Fitch have reacted to Nigeria’s changing landscape. Moody’s recently affirmed Nigeria’s rating with a positive outlook, citing improvements such as the rebasing (which indicates better statistical footing) and ongoing reforms (proshare.co). This positive outlook from a major agency suggests that if Nigeria capitalizes on lower inflation to pursue growth-friendly policies while keeping reform momentum, its credit risk could improve. That, in turn, would gradually compress sovereign risk premia and support lower yields. Conversely, agencies are also watching if the inflation drop is misleading – one noted that “headline inflation… came in at 24.48%, but does this reflect reality?”, hinting they will watch core inflation and price stability before changing views (premiumtimesng.com).

Local Economists – Some Nigerian economists have commented that the rebasing is a “double-edged sword” (tribuneonlineng.com). It improves the optics of inflation, which can bolster confidence, but there’s a risk that policymakers or the public might be complacent about underlying inflation which is still high. The consensus among experts is that Nigeria must accompany the statistical changes with real economic improvements (boost food supply, maintain FX stability) to ensure inflation genuinely falls. If that happens, many expect a virtuous cycle: lower inflation -> lower interest rates -> lower borrowing costs for government -> improved fiscal health, etc.

Bottom line: The rebasing has injected optimism and altered forecasts toward a more positive direction. Investment banks and research teams are revising their outlooks: for instance, some now predict interest rate cuts in 2025 (where before they expected more hikes). Bond strategists anticipate strong demand to continue for Nigerian bonds given the improved real yield outlook and Nigeria’s commitment to reforms. However, there is also an understanding that much depends on actual inflation behavior in coming months. If the official numbers stay low and trend downward, Nigeria could see a sustained rally in its bonds and a steeper decline in yields across the curve. If not, the initial enthusiasm may fade and yields could correct upward. For now, forecasts are tilted toward Nigeria “turning the corner” on inflation, with numerous experts highlighting opportunities for policy easing and investment growth in the wake of the CPI rebase.

Conclusion

In conclusion, Nigeria’s CPI rebasing has had an immediate dampening effect on inflation expectations, translating into lower yields on both short-term and long-term government debt. Investors, domestic and foreign, have reacted positively, driving a bond rally and increasing portfolio inflows as real yield prospects improved. The CBN is treading carefully – acknowledging the new data but holding policy steady until it’s confident inflation is truly contained. The yield curve has shifted downward and somewhat flattened in the short run, with T-bill rates dropping toward the high-teens and bond yields around 19–20%, versus well above 20% before.

In the short term, local bond yields are likely to remain lower than pre-rebasing levels, barring any shock, thanks to changed sentiment and the possibility of monetary easing. In the medium term, much will hinge on whether the lower inflation is sustained; steady or falling inflation could see yields fall further, whereas any resurgence of price pressures might push yields back up. Longer-term, if Nigeria can use this statistical reset as a foundation for actual disinflation (through reforms and prudent policy), it could pave the way for structurally lower interest rates and borrowing costs in the economy.

Crucially, Nigeria’s case underscores that while rebasing is a statistical exercise, its impact on perceptions and behavior is very real. The challenge ahead will be to convert the optimism from improved data into tangible economic gains – keeping inflation on a downward trajectory so that the bond market gains are sustained and the CBN can safely lower rates. As one report summed up, the rebased CPI is “a new compass” for Nigeria– it provides a clearer direction, but the journey to low inflation and stable yields will require continued careful navigation of policy and structural issues beyond this technical change.