Midweek Review: Inflation, Rates and Risk Appetite Are Repricing the Week

Ranora Market Outlook -Nigeria’s inflation surprise, softer equities, a fresh Treasury bills auction and the pending Fed decision have shifted the market conversation from optimism to selectivity.

Opening View

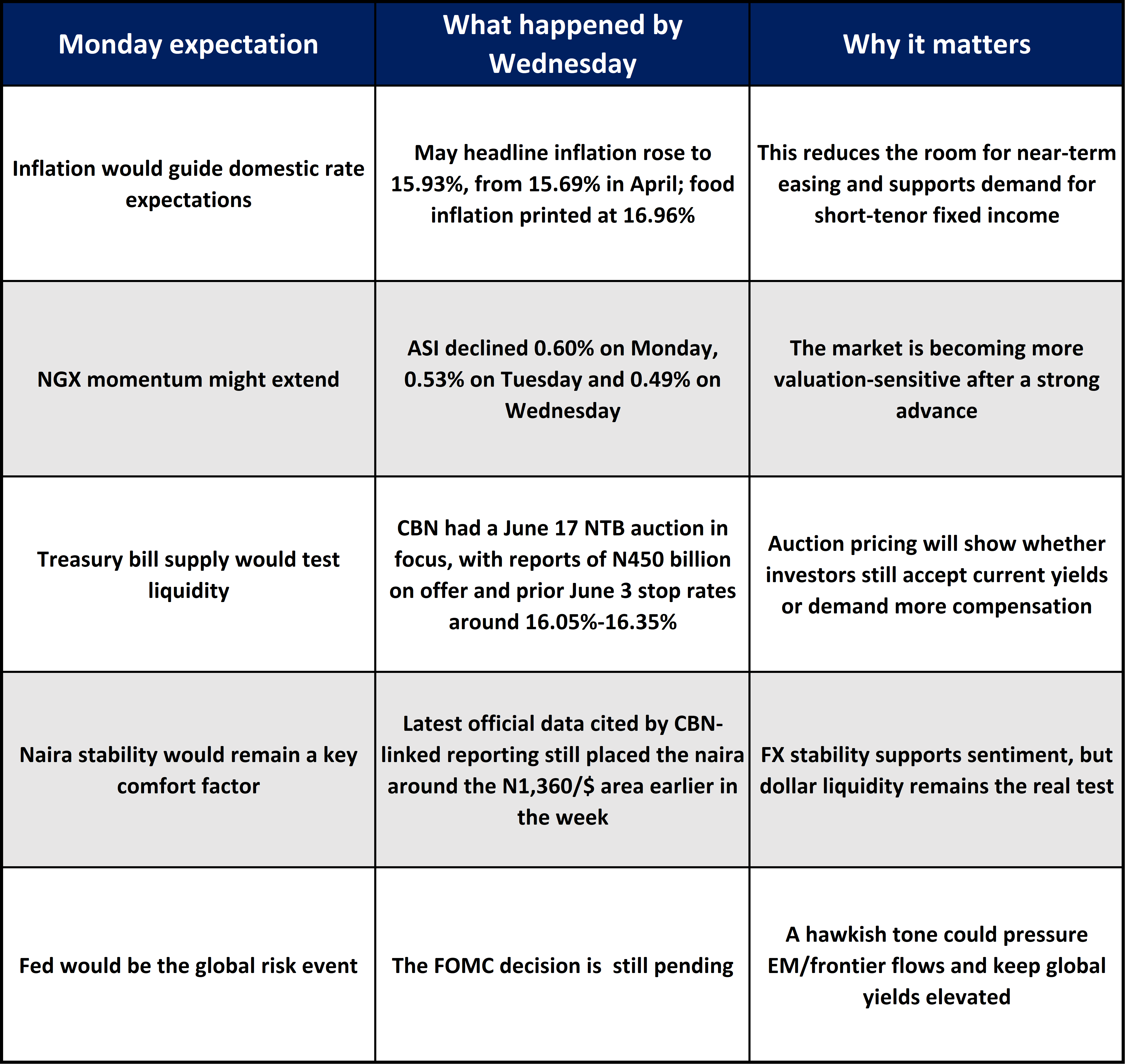

By midweek, the main change is that Nigerian markets have moved from waiting for signals to pricing them. The May inflation print confirmed that price pressure has not yet fully settled, with headline inflation rising to 15.93% from 15.69% in April, while food inflation rose to 16.96%. That makes aggressive monetary easing less likely in the near term and keeps the case for short-duration fixed income intact.

Equities have also lost some momentum. The NGX All Share Index fell on Monday, Tuesday and Wednesday, suggesting profit-taking after a strong run rather than a collapse in risk appetite. The more important signal is rotation: investors are likely to demand stronger earnings visibility before paying higher multiples.

Globally, the Fed remains the biggest swing factor. The FOMC decision is still pending, with the statement expected shortly later today. That matters for Nigeria because a hawkish Fed tone could support the dollar, lift global yields, and reduce foreign appetite for frontier-market risk. Oil is still supportive for Nigeria’s external position, but price volatility means FX comfort should not be treated as permanent.

The Big Picture:

Monday began with markets watching three things: Nigeria’s inflation print, domestic liquidity through the Treasury bills market, and the Fed’s June policy decision.

By Wednesday, the domestic picture had become clearer. Inflation rose again, fixed income remained attractive, and the equity market showed signs of fatigue. That combination supports a more selective allocation stance: short-duration fixed income remains useful for yield capture, while equities require stronger earnings conviction.

The global picture is less settled because the Fed decision sits at the centre of risk pricing. The Federal Reserve calendar confirms the June 17 FOMC meeting, with this meeting associated with updated projections. Markets were broadly positioned for no rate change, but the tone of the statement and press conference matters more than the hold itself. A firm inflation message would keep US yields elevated and make dollar assets harder to compete with.

What Changed On Monday:

Nigeria Market Intelligence:

Inflation Has Become the Week’s Main Domestic Signal

What happened: NBS data showed headline inflation at 15.93% in May 2026, up from 15.69% in April. Food inflation stood at 16.96%, while core inflation was 16.82%.

Why it matters: The disinflation story has become less straightforward. Even with the rebased CPI series, three consecutive increases in headline inflation would make the CBN more reluctant to loosen policy quickly.

What it means for investors: This keeps short-duration fixed income attractive. Investors may continue to prefer Treasury bills and money-market instruments where yields compensate for inflation and liquidity risk. For equities, the implication is more selective: companies with pricing power, strong margins and low financing stress should screen better.

What to watch next: June food prices, liquidity conditions, and the July MPC meeting scheduled for July 20-21.

Nigerian Equities Have Shifted From Momentum to Profit-Taking

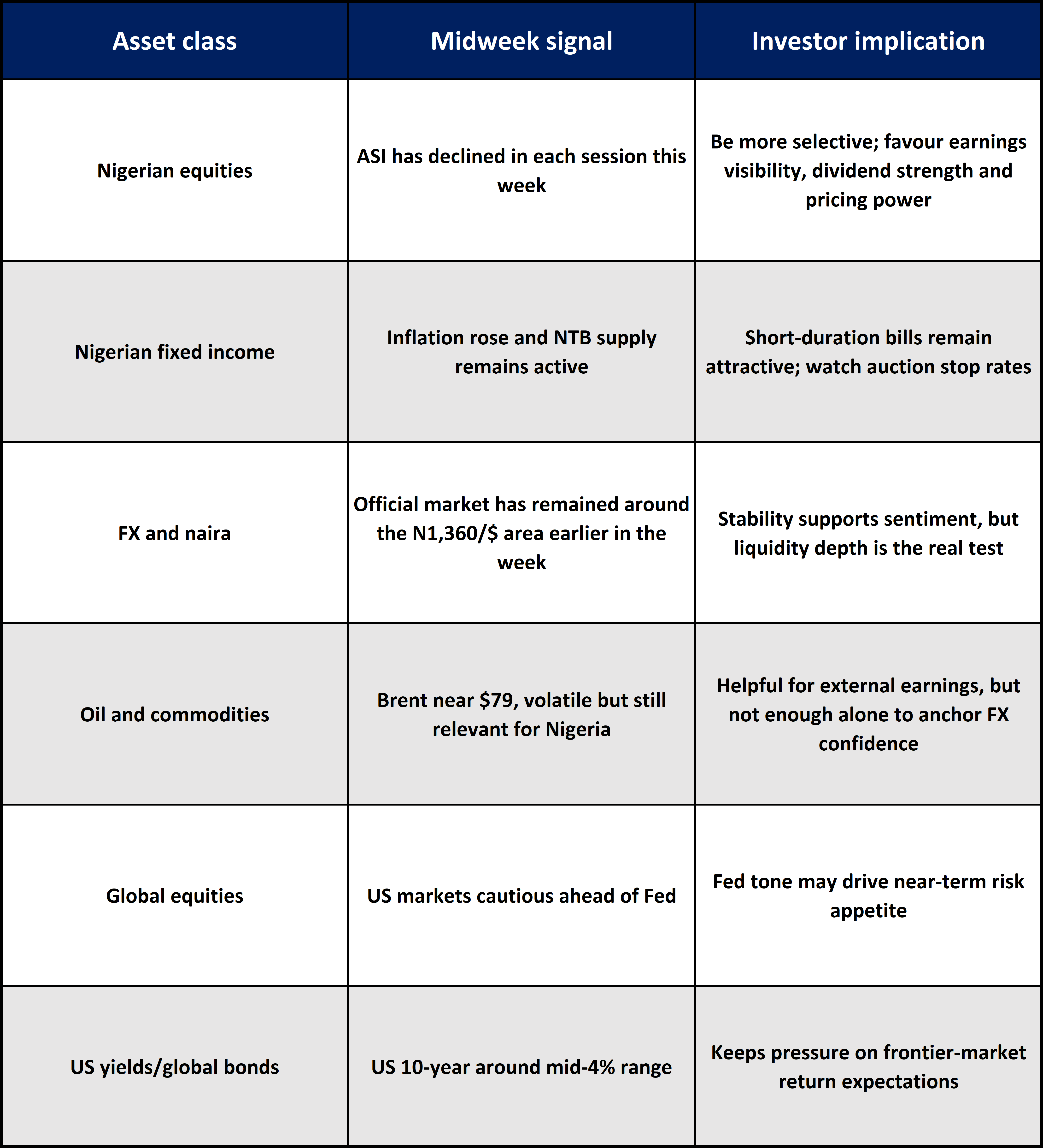

What happened: The NGX All Share Index fell to 240,802.72 on June 17, after closing at 241,984.80 on June 16 and 243,271.56 on June 15. That means the market has declined each trading session so far this week.

Why it matters: This does not automatically signal a change in the broader equity story. It does suggest that investors are no longer buying the market indiscriminately. After a strong year-to-date move, earnings quality and dividend visibility matter more.

What it means for investors: Banks and cash-generative large caps may remain supported if earnings momentum holds, but weaker names could see more pressure if yields stay attractive. High fixed-income yields create a real hurdle rate for equities.

What to watch next: Whether sell-offs are concentrated in previously high-performing names or spread across defensives, banks and industrials.

Treasury Bills Remain the Key Domestic Allocation Battleground

What happened: CBN data for the June 3 NTB auction showed stop rates of 16.05% for 91-day bills, 16.19% for 182-day bills and 16.35% for 364-day bills. A fresh NTB auction was scheduled for June 17, reporting N450 billion on offer and settlement on June 18.

Why it matters: The auction matters because it will show whether the market is comfortable with current yields after the inflation print. If stop rates move higher, that strengthens the case for fixed income and could pull liquidity away from equities.

What it means for investors: Short bills remain useful for liquidity management. Longer duration should be approached carefully unless yields offer enough protection against inflation, supply and policy risk.

What to watch next: Auction stop rates, bid-to-cover levels, and whether investors crowd into the 364-day tenor.

FX Stability Is Helpful, But Not Yet a Free Pass

What happened: CBN exchange-rate data earlier in the week showed the official NFEM market still trading around the N1,360/$ region, reporting about N1,363.83/$ at the start of the week.

Why it matters: Naira stability reduces imported inflation pressure and helps foreign investors assess entry risk. But the key question is not only the spot rate; it is the depth and consistency of dollar supply.

What it means for investors: Stable FX supports banks, import-linked consumer names and overall confidence. But portfolios should still account for renewed naira pressure if oil weakens, dollar demand rises, or Fed messaging strengthens the dollar.

What to watch next: NFEM turnover, external reserves, oil receipts and parallel-market pressure.

Global Market Intelligence:

The Fed Is the Week’s Main Global Event

What happened: The Federal Reserve’s June 16-17 FOMC meeting is underway, with the official Fed calendar showing it as a projections meeting. Market commentary before the decision expected the Fed to hold the target range at 3.50%-3.75%.

Why it matters: A hold is not the main issue. The key is whether the Fed sounds comfortable, patient or more hawkish on inflation. For Nigeria, higher-for-longer US rates can reduce foreign appetite for frontier-market assets.

What it means for investors: If the Fed sounds hawkish, Nigerian fixed income may need to offer higher risk-adjusted returns to attract offshore interest. Equities could also face pressure if global investors reduce exposure to higher-risk markets.

What to watch next: The dot plot, inflation projections, Chair Kevin Warsh’s tone, and US yield reaction.

US Yields Are Still High Enough to Matter

What happened: Data showed the US 10-year Treasury yield at 4.47% on June 15. The US 10-year yield around 4.44% intraday on June 17.

Why it matters: At those levels, US duration still competes strongly for global capital. Frontier markets need a credible local yield, currency and policy story to attract flows.

What it means for investors: Nigeria’s fixed-income market can still appeal if yields remain compelling and FX conditions hold. But a stronger dollar or rising US yields would raise the return premium investors demand.

What to watch next: The post-Fed move in the US 2-year and 10-year yields.

Oil Is Supportive, But Volatility Is the Message

What happened: Brent crude around $79 per barrel on June 17. The price was slightly higher on the day but materially lower over the past month.

Why it matters: Nigeria benefits from firm crude prices through external earnings and reserves, but volatility limits how much confidence investors should place on oil alone.

What it means for investors: Oil above recent lows can support FX sentiment, but the fiscal and reserve impact depends on production, export receipts and subsidy/import dynamics. Investors should avoid treating oil strength as a permanent naira backstop.

What to watch next: Brent direction, OPEC+ supply signals, geopolitical risk and Nigeria’s production levels.

Dollar Strength Remains a Watch Item

What happened: Trading Economics showed the DXY dollar index around 99.68 on June 17, slightly higher on the session.

Why it matters: A stronger dollar typically tightens financial conditions for emerging and frontier markets. It can also raise pressure on currencies where dollar demand is structurally high.

What it means for investors: Naira stability is more valuable when the dollar is firm. If the dollar strengthens after the Fed decision, Nigerian assets may need stronger domestic yields or clearer FX liquidity to remain attractive.

What to watch next: DXY reaction after the Fed, US real yields and EM currency performance.

Asset Class Implications:

Ranora View:

The main lesson from the week so far is that Nigeria’s market setup is still yield-led. Inflation has not softened enough to justify a decisive move away from short-duration fixed income, while equities are starting to show valuation fatigue after a strong run.

For investors, the practical implication is clear: liquidity and yield still deserve a meaningful place in portfolios. Equities should not be abandoned, but exposure should be more disciplined. The best equity opportunities are likely to be in companies that can defend margins, benefit from high nominal activity, or translate balance-sheet strength into dividends.

The Fed decision is the external risk. If the Fed sounds hawkish, the dollar and US yields could pressure frontier-market flows. If the tone is balanced, Nigeria’s local story can regain attention, especially if the naira remains stable and oil does not weaken sharply.

This is not a market for broad optimism. It is a market for selective risk-taking, short-duration income, and close attention to FX liquidity.

What to Watch Next:

The June 17 FOMC statement, dot plot and Chair Warsh’s press conference.

Final result of the June 17 Nigerian Treasury bills auction.

NGX market breadth: whether selling remains mild or becomes sector-wide.

NFEM turnover and whether the naira holds around recent levels.

Brent crude direction and implications for Nigeria’s reserves and fiscal receipts.

Question for the day:

If Nigerian Treasury bill yields remain above 16% while equities continue to cool, would you increase fixed-income exposure or use the equity pullback to build positions gradually?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.