Midweek Review: Nigeria’s Equity Pullback Meets Higher Global Yields

Ranora Market Outlook -By midweek, the market story has shifted from waiting for direction to pricing tighter financial conditions across equities, fixed income, FX, and oil-sensitive assets

Opening View

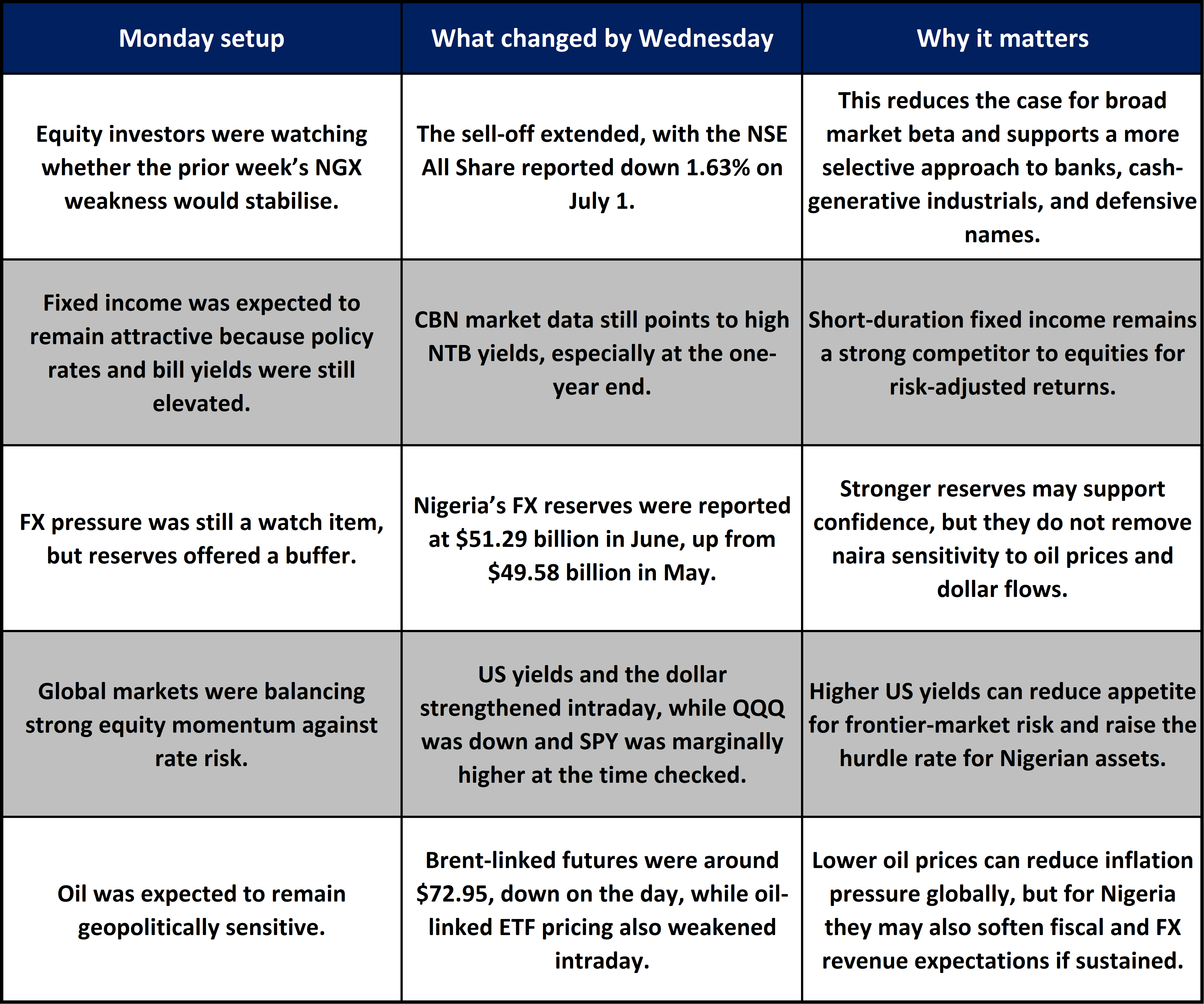

The first half of the week has clarified one point: investors are becoming more selective. Nigerian equities entered the week after a weak close in the prior week, and by Wednesday the pressure had extended. The NGX All Share Index was reported around 225,690 points on July 1, down 1.63% from the previous session, after the official NGX weekly report showed the market had already lost 1.65% in the week ended June 26. That makes the equity market less about broad momentum and more about stock selection, earnings visibility, and sector resilience.

Fixed income remains anchored by high domestic rates. The CBN’s latest published market rates show 91-day, 182-day, and 364-day NTB rates at 16.28%, 16.50%, and 17.34% respectively as of June 17, while the Monetary Policy Rate remains 26.50%.

Globally, the pressure point is US rates. The Fed held its target range at 3.50% to 3.75% in June, but inflation language remains firm, and the US 10-year yield was around 4.47% intraday on July 1.

For Nigerian investors, the implication is clear: cash yields remain difficult to ignore, equity risk needs stronger earnings justification, and naira confidence still depends on reserve strength, oil flows, and dollar liquidity.

The Big Picture:

The market is no longer trading only on hope that disinflation, liquidity, and earnings will carry risk assets. It is now testing how much valuation support exists when yields remain high.

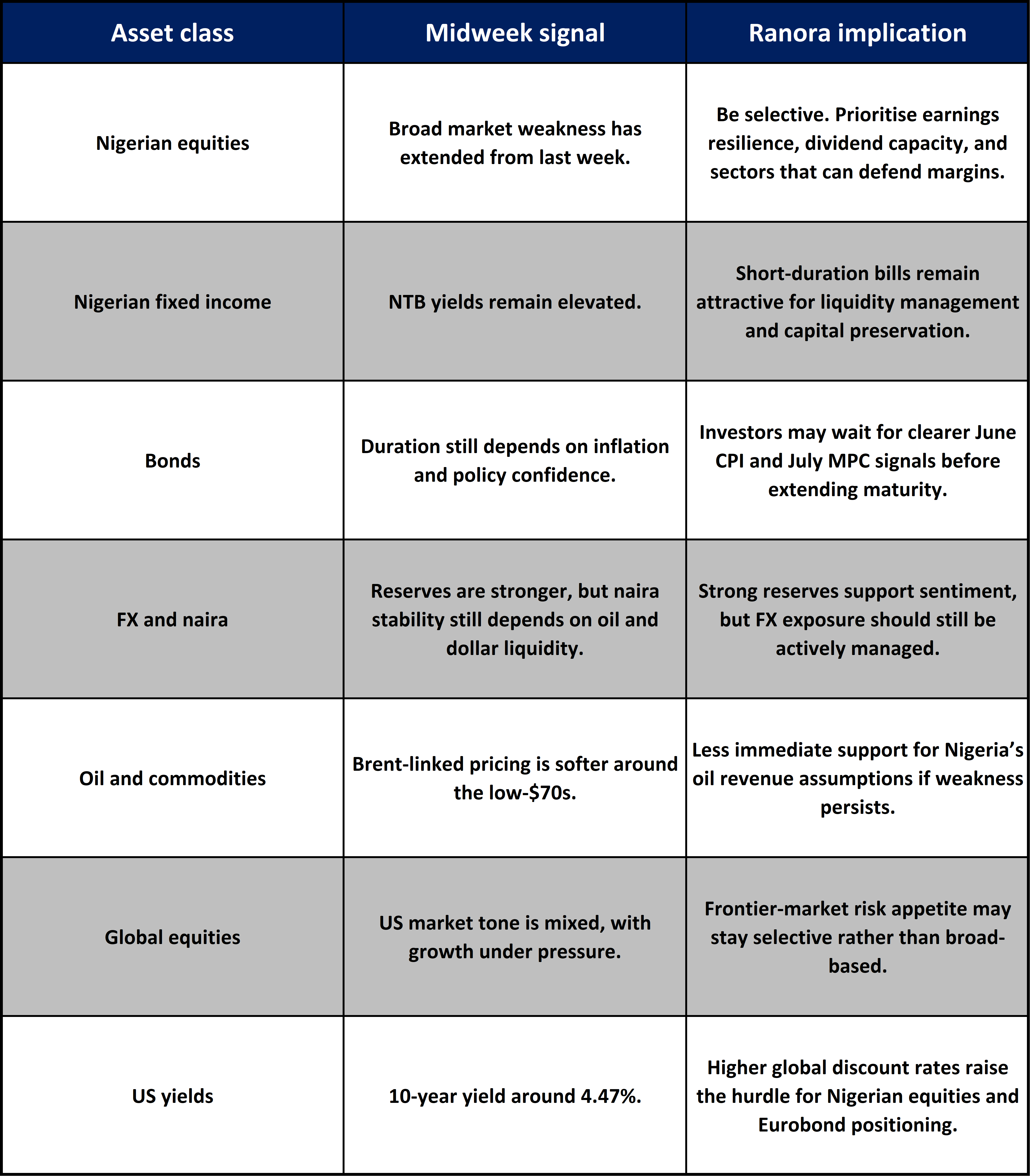

In Nigeria, the key tension is between equity valuations and fixed-income alternatives. A 364-day NTB rate above 17% means investors need a clear earnings or dividend story to justify equity risk. That does not make equities unattractive, but it narrows the acceptable universe. Banks may still benefit from high-rate income dynamics, but investors will increasingly separate strong balance sheets and capital adequacy from weaker names.

The second tension is FX. Nigeria’s reserves have improved, but the naira remains exposed to oil receipts, portfolio flows, import demand, and CBN intervention capacity. Strong reserves are supportive, but they are not a full substitute for durable dollar supply.

Globally, the Fed remains the anchor. The June FOMC statement kept rates unchanged but still described inflation as elevated relative to the 2% goal. That keeps US yields relevant for emerging and frontier markets. When US yields rise, investors demand more compensation for naira assets, Nigerian Eurobonds, and equity exposure.

What Changed On Monday:

Nigeria Market Intelligence:

Equities: the broad market is under pressure

What happened: The official NGX report showed the All Share Index fell 1.65% in the week ended June 26 to 232,049.02. By July 1, Trading Economics reported Nigeria’s main stock index around 225,690, down 1.63% from the previous session.

Why it matters: This suggests the weakness has moved beyond a one-session correction. Investors are reassessing valuation after a strong prior run, especially where earnings upgrades are not keeping pace with prices.

What to watch next: Watch whether banks and consumer names continue to outperform the broader market. If defensive and high-dividend names hold better than growth-sensitive stocks, the market may be rotating rather than fully de-risking.

Fixed income: high yields remain the portfolio anchor

What happened: CBN’s published market data showed 91-day, 182-day, and 364-day NTB rates at 16.28%, 16.50%, and 17.34% respectively as of June 17. The MPR remains at 26.50% after the May MPC meeting.

Why it matters: High bill yields keep liquidity parked in short-duration instruments. This creates a valuation ceiling for equities because investors can earn attractive nominal returns without taking equity volatility.

What to watch next: The July 20-21 MPC meeting is now important. If the CBN keeps policy tight, short-duration fixed income may remain attractive. If inflation softens more convincingly, investors may start extending duration.

Inflation: the disinflation story is no longer one-way

What happened: NBS headline inflation was reported at 15.93% in May 2026, up from 15.69% in April, while food inflation was 16.96%.

Why it matters: The annual inflation rate remains far below last year’s levels, but the month-to-month direction still matters for policy. If inflation keeps rising, the CBN has less room to ease rates quickly.

What to watch next: June CPI, due in July, will be important for the July MPC. A softer print could support duration appetite. Another increase would keep the market positioned for tight liquidity and elevated yields.

FX and reserves: stronger reserves, but not a free pass

What happened: Nigeria’s foreign exchange reserves were reported at $51.29 billion in June, up from $49.58 billion in May.

Why it matters: Higher reserves improve confidence around external liquidity and may reduce immediate naira stress. But reserves alone do not guarantee currency stability if oil prices soften, import demand rises, or portfolio flows weaken.

What to watch next: Watch NFEM turnover, CBN intervention signals, oil prices, and whether stronger reserves translate into more stable official FX pricing.

Global Market Intelligence:

US rates remain the global anchor

What happened: The Fed held the federal funds target range at 3.50% to 3.75% in June and said inflation remained elevated relative to its 2% goal. The US 10-year yield was around 4.47% intraday on July 1.

Why it matters: Higher US yields make frontier-market assets work harder. Nigerian fixed income may still screen attractive in nominal terms, but foreign investors will compare that return against US yields, dollar strength, FX convertibility, and naira risk.

What to watch next: Fed communication, US inflation data, and whether the US 10-year yield remains above 4.4%.

US equities are mixed beneath the surface

What happened: At the time checked on July 1, SPY was slightly higher at $747.60, while QQQ was down 1.2% at $727.53.

Why it matters: This points to a market where broad US risk appetite is still present, but high-duration growth names are more sensitive to rate pressure. That matters for emerging markets because global investors often reduce higher-risk exposure when US tech and long-duration assets weaken.

What to watch next: Whether weakness in growth-heavy indices broadens into general risk reduction.

Oil remains useful but less supportive than a strong rally

What happened: Brent-linked futures were around $72.95 and down on the day, while USO was down 2.53% intraday.

Why it matters: Nigeria benefits from firm oil prices through fiscal receipts and FX inflows, but softer oil reduces that support. For businesses, lower oil can ease some global inflation pressure, but for Nigeria’s external account the revenue effect matters more.

What to watch next: Brent stability above the low-$70s, OPEC supply signals, and geopolitical headlines that could restore the risk premium.

Gold is still drawing defensive demand

What happened: GLD was up 1.36% intraday at the time checked on July 1.

Why it matters: Gold strength alongside higher yields suggests investors are still paying for hedges. That usually reflects concern about inflation, geopolitics, debt, or currency volatility.

What to watch next: Whether gold continues to rise even if US yields stay high. That would indicate persistent demand for portfolio insurance.

Asset Class Implications:

Ranora View:

The key change since Monday is that caution has become more evidence based. Nigerian equities are no longer simply vulnerable to profit-taking; they are actively repricing against high domestic yields and a firmer global rates backdrop.

Ranora’s view is that investors should treat this as a rotation environment, not a market to chase indiscriminately. Short-duration fixed income remains compelling because it offers yield, liquidity, and lower volatility. Equities still have a place, but the case must be built name by name. Banks with strong capital positions, disciplined cost control, and credible earnings visibility may continue to attract interest. Consumer and industrial names need stronger margin evidence before they deserve aggressive allocation.

For businesses, the message is also clear: funding costs are unlikely to fall quickly, FX planning remains essential, and pricing power will matter as inflation remains sticky.

The next major domestic catalyst is the June inflation print, followed by the July MPC meeting. Until then, portfolios should be built around liquidity, income, and selective exposure to companies that can convert macro stress into earnings resilience.

What to Watch Next:

June inflation data and whether headline inflation breaks the recent upward drift.

The July 20-21 CBN MPC meeting and any signal on the future path of rates.

NGX market breadth, especially whether banking and defensive sectors keep outperforming.

Brent crude direction and its effect on Nigeria’s fiscal and FX assumptions.

US yields and dollar strength, because they will shape foreign appetite for frontier-market risk.

Question for the day:

If Nigerian Treasury bills continue to offer attractive yields, what would make you increase equity exposure now: cheaper valuations, stronger earnings, higher dividends, or clearer FX stability?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.