Midweek Review: Rates, Rotation, and the Oil Price Reset

Ranora Market Outlook -By midweek, Nigerian markets are balancing strong fixed-income demand, fragile equity momentum, steadier FX, and a global repricing of oil and rate expectations.

Opening View

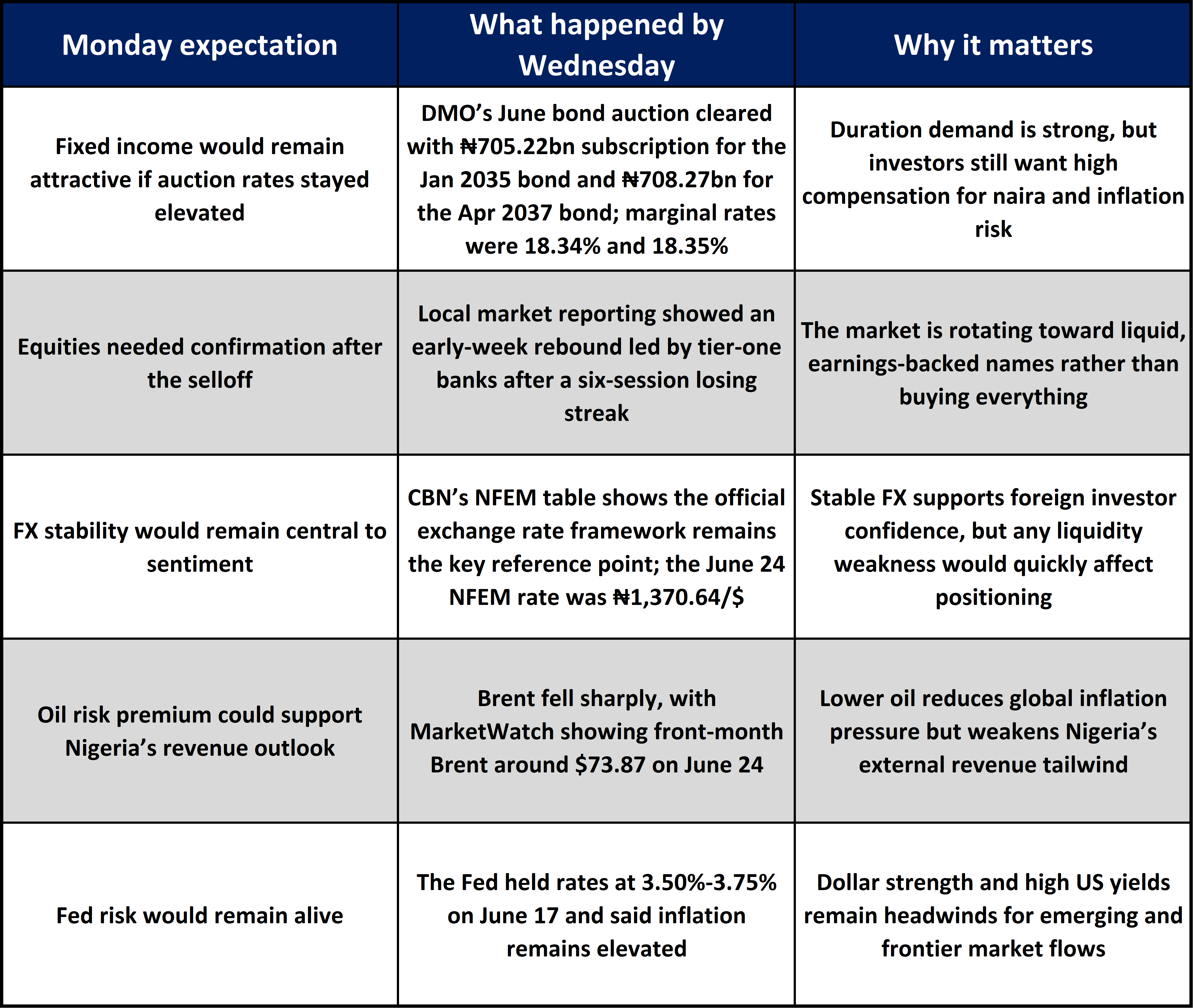

The week has changed in three important ways since Monday. First, Nigeria’s fixed-income market has given investors a clearer signal: demand for FGN bonds remains deep, but investors are still asking to be paid well for duration risk. The June FGN bond auction attracted subscriptions above the ₦1.2 trillion offer size, with marginal rates around 18.34% to 18.35%, confirming that long-term naira paper remains attractive only at elevated yields. Second, Nigerian equities have moved from panic selling into selective recovery. The early-week rebound was led by banking names, but the broader lesson is that investors are becoming more valuation-sensitive after a very strong market run. Third, oil has shifted from geopolitical risk premium to supply-normalization risk. Brent’s slide toward the mid-$70s reduces inflation pressure globally, but for Nigeria it also trims the upside from oil revenue if the decline persists.

The key investment message is straightforward: this is still a yield-led market. Equities can recover where earnings are credible, but fixed income remains the anchor for conservative naira portfolios. The global backdrop is less supportive than it looked earlier in the week because the dollar remains firm and the Fed has not opened the door to near-term easing.

The Big Picture:

Monday’s setup was dominated by three questions: would Nigerian equities stabilise after last week’s selloff, would the bond auction clear cleanly, and would oil remain supported by geopolitical risk?

By Wednesday, the answers are more balanced. The bond auction cleared with strong demand, but at rates that confirm investors still require a meaningful inflation and policy-risk premium. Equities have shown signs of rebound, especially in banks, but the market is no longer moving as one broad rally. Oil has weakened as concerns around Strait of Hormuz disruption eased, reducing one source of global inflation pressure while also lowering a potential revenue cushion for Nigeria.

What Changed On Monday:

Nigeria Market Intelligence:

Fixed income is still the cleanest market signal

What happened: The DMO’s June 2026 FGN bond auction reopened the 22.60% Jan 2035 and 16.2499% Apr 2037 bonds. Each had ₦600bn offered. Subscriptions came in at ₦705.22bn and ₦708.27bn, with marginal rates of 18.34% and 18.35%.

Why it matters: Investors are still willing to extend duration, but only at yields that compensate for inflation, liquidity, and policy uncertainty. This keeps medium-to-long duration bonds investable, but the entry point matters.

What to watch next: Watch whether secondary-market yields compress after settlement or stay near auction-clearing levels. If yields remain sticky, it suggests investors are still cautious about inflation and supply risk.

Equities have moved from broad momentum to selective rotation

What happened: Nigerian equities rebounded early in the week after a six-session losing streak, with market reports pointing to banking stocks, including First HoldCo and GTCO, as key drivers of the Monday recovery.

Why it matters: This is not just a bounce; it is a test of market quality. After a strong 2026 rally, investors are becoming more selective. Banks remain important because recapitalization, earnings strength, and liquidity make them the market’s main risk barometer.

What to watch next: Watch whether gains broaden beyond banks into consumer, telecoms, industrials, and oil and gas names. A narrow banking-led rally is less durable than a multi-sector recovery.

Inflation remains a policy constraint

What happened: Nigeria’s headline inflation rose to 15.93% in May 2026 from 15.69% in April, while food inflation also increased to 16.96% from 16.06%.

Why it matters: Even though inflation is far below last year’s level, the month-to-month direction matters for policy. Rising annual inflation makes it harder for the CBN to ease aggressively and supports the case for elevated naira yields.

What to watch next: Watch June inflation and food price momentum. If food inflation keeps rising, fixed-income investors may continue demanding high real-yield protection.

FX stability is helpful, but liquidity remains the real test

What happened: CBN’s NFEM data show the official market remains the key reference point, with the June 24 NFEM rate at ₦1,370.64/$.

Why it matters: A relatively stable official naira rate supports portfolio sentiment, import planning, and equity valuations. But the market will care less about the headline rate and more about whether dollar liquidity is deep enough for repatriation and trade demand.

What to watch next: Watch NFEM turnover, external reserves, and any widening gap between official and street-market pricing.

Global Market Intelligence:

The Fed is still not offering relief

What happened: The Federal Reserve held the federal funds target range at 3.50%-3.75% on June 17 and said inflation remains elevated.

Why it matters: For Nigeria and other frontier markets, the Fed’s stance matters through dollar strength, US yields, and global risk appetite. If US rates remain high, foreign investors will require more compensation to hold naira assets.

What to watch next: Watch US PCE inflation and Fed communication. Softer inflation could help frontier-market flows; sticky inflation would keep pressure on duration and FX.

US yields remain a global valuation anchor

What happened: US 10-year Treasury yields were around the mid-4% area on June 24, with market data showing yields easing but still elevated.

Why it matters: High US yields raise the hurdle rate for global equities and emerging-market debt. For Nigeria, this means domestic yields must remain attractive enough to compete for capital.

What to watch next: Watch whether the US 10-year moves closer to 4.25% or back toward 4.50% and above. That range will shape global risk appetite into month-end.

Oil has lost part of its geopolitical premium

What happened: Brent crude fell sharply on June 24, with MarketWatch showing front-month Brent around $73.87, down more than $3 on the day.

Why it matters: Lower oil helps reduce global inflation risk and could ease pressure on central banks. For Nigeria, the implication is more complicated: lower Brent can reduce revenue upside and FX inflow expectations if prices remain weak.

What to watch next: Watch whether Brent stabilizes above $75 or drifts toward $70. Nigeria’s fiscal and FX assumptions become more vulnerable if the decline extends.

Dollar strength remains a pressure point

What happened: Market reports showed the dollar firming as investors priced global risk, high US yields, and Fed caution.

Why it matters: A stronger dollar tightens financial conditions for emerging and frontier markets. For Nigeria, this can affect foreign portfolio appetite, imported inflation, and the naira’s room to remain stable.

What to watch next: Watch the dollar index and US inflation data. A stronger dollar would make local FX liquidity more important for investor confidence.

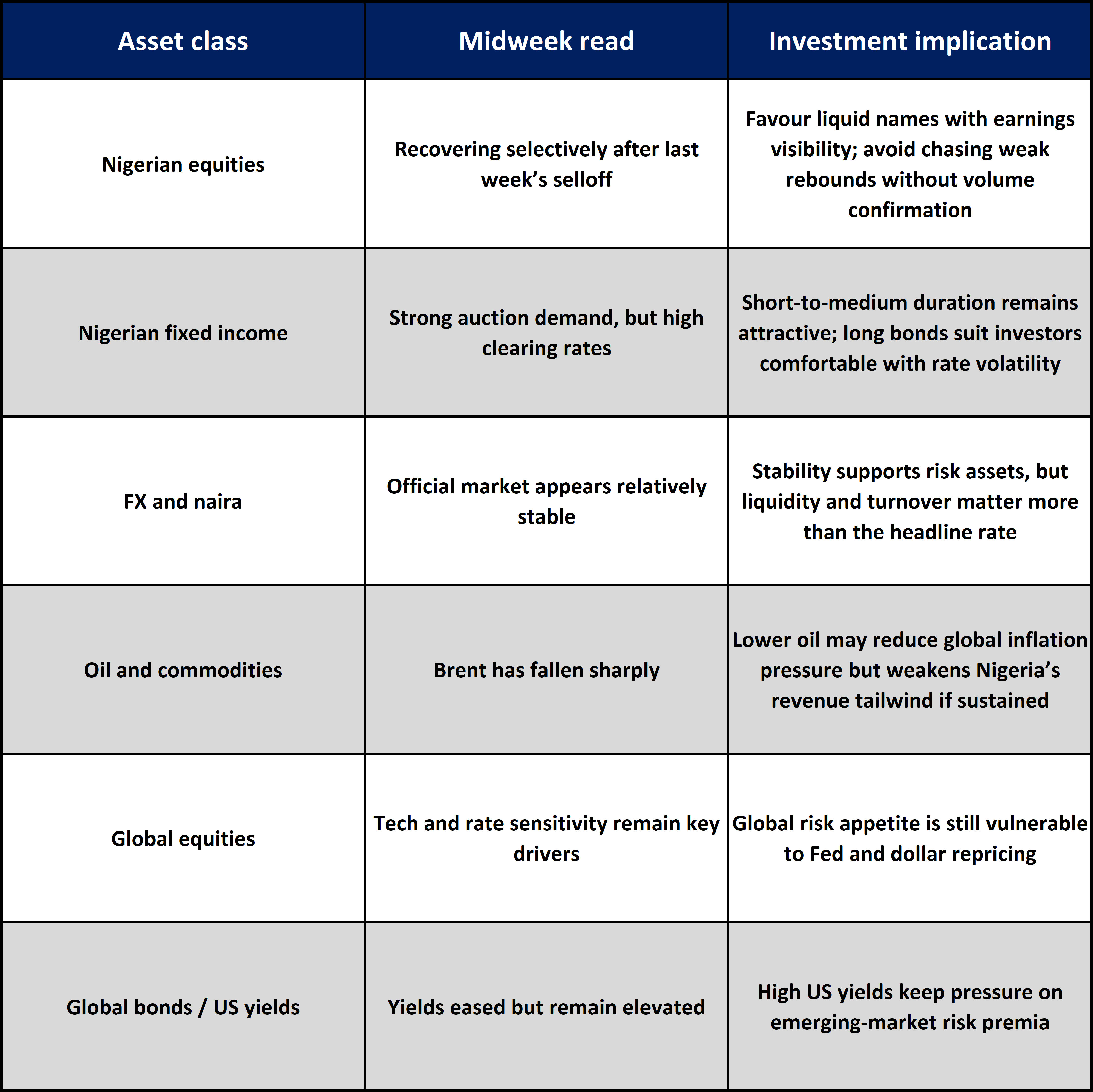

Asset Class Implications:

Ranora View:

Ranora’s view is that the week has become more favorable for disciplined income investors than for broad equity risk-taking. The Nigerian bond auction confirms that there is still meaningful appetite for sovereign naira assets, but it also confirms that the market is not ready to accept low compensation for duration. That keeps fixed income central to portfolio construction.

For equities, the recovery should be treated as selective rather than automatic. Banks remain strategically important because they sit at the intersection of recapitalization, credit growth, high interest income, and investor liquidity. But after the strength already seen in 2026, earnings delivery now matters more than index momentum.

The biggest external change is oil. A lower Brent price reduces global inflation risk, but it also removes some support from Nigeria’s external account narrative. If oil remains weak while the dollar stays firm, Nigeria will need FX liquidity, portfolio inflows, and confidence in policy execution to do more of the heavy lifting.

What to Watch Next:

Whether NGX gains broaden beyond banks before Friday.

Secondary-market movement after the June FGN bond auction settlement.

NFEM turnover and any sign of pressure in dollar liquidity.

Brent crude’s ability to hold above the mid-$70s.

US PCE inflation and its effect on Fed rate expectations.

Question for the day:

If Nigerian yields stay elevated while equities become more selective, would you rather add duration in fixed income or rotate into high-quality dividend-paying stocks?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.