Midweek Review: T+1 Friction, Naira Firmness, and Oil-Led Global Rate Risk

Ranora Market Outlook -Nigeria’s market week has shifted from operational optimism to a sharper test of liquidity, settlement discipline, and investor risk appetite

Opening View

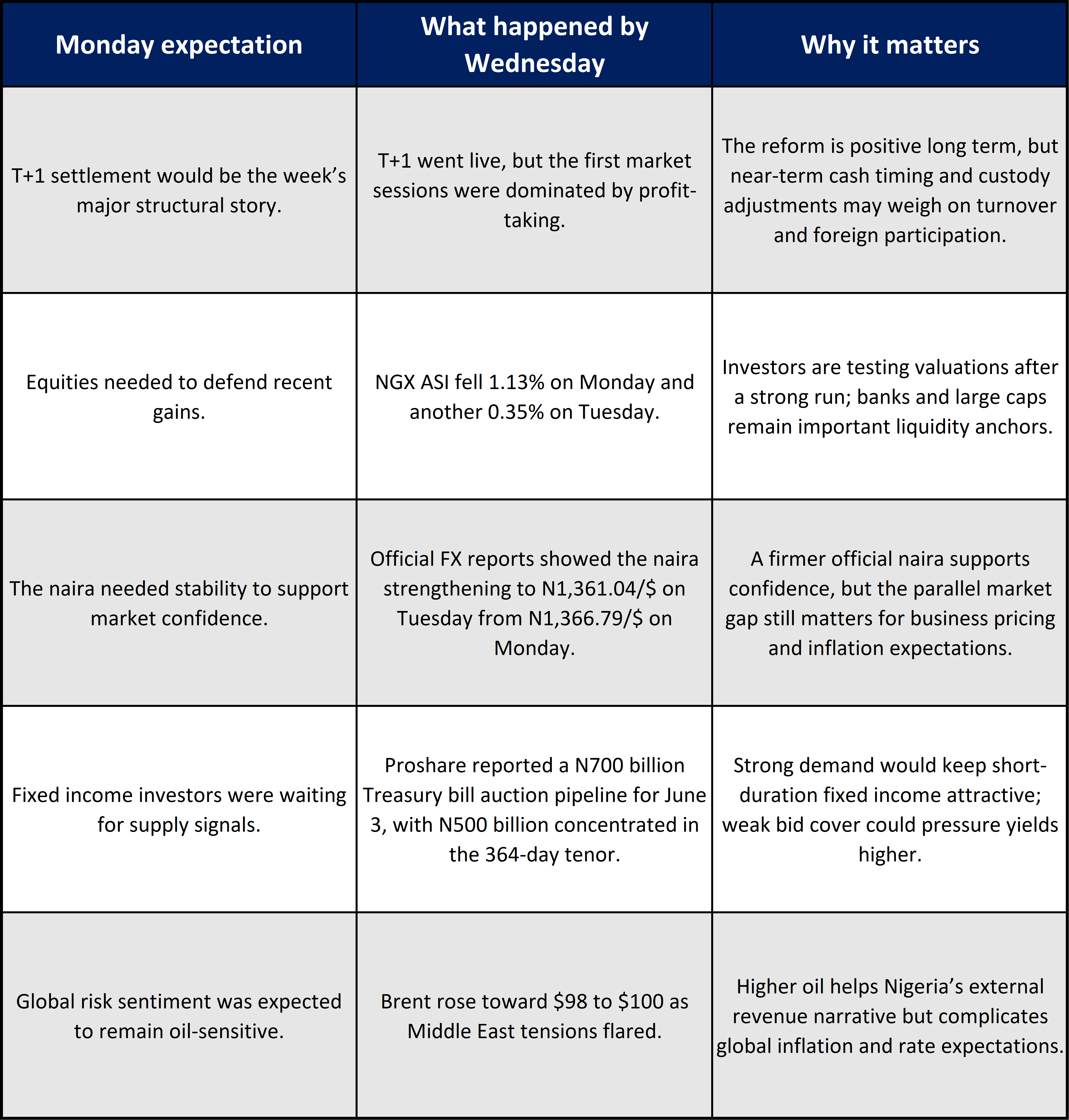

The main change since Monday is that Nigeria’s market setup has moved from expectation to execution. The T+1 settlement cycle is now live, but the first sessions of June have also exposed near-term friction in equities: the NGX opened the month with a sharp decline on Monday and extended losses on Tuesday as investors took profit in large and mid-cap names. That does not necessarily signal a broken market. It signals that a faster settlement regime is arriving at the same time as investors are reassessing valuations, cash timing, and capital-raise opportunities.

The naira has been the more constructive side of the story. Official market data reported by local outlets showed the naira strengthening from N1,366.79/$ on Monday to N1,361.04/$ on Tuesday, suggesting that FX sentiment has not deteriorated despite global oil and dollar volatility. But the positive FX read must be treated carefully: one or two sessions of naira strength do not remove the broader dependency on dollar liquidity, reserves, oil receipts, and foreign portfolio flows.

Globally, the week has become less friendly for rate-cut expectations. Brent crude moved back toward $100 as Middle East tensions escalated, while U.S. data continued to show resilience in labour demand. For Nigeria, that combination is double-edged: higher oil can support external receipts, but it can also keep global inflation, dollar strength, and imported cost pressure alive.

The Big Picture:

Monday’s setup was about whether Nigerian markets could absorb a major infrastructure change without losing liquidity. By Wednesday, the answer is more nuanced: the T+1 transition is positive for market efficiency, but early trading suggests investors are still adjusting to the funding and settlement discipline required by a shorter cycle.

The Securities and Exchange Commission confirmed that eligible equities and commodities trades cleared and settled by CSCS would move to T+1 from Monday, June 1, 2026, meaning settlement now occurs one business day after trade date. The policy objective is clear: reduce counterparty exposure, improve market efficiency, and align Nigeria more closely with global post-trade standards. The investment implication is also clear: faster settlement can improve liquidity over time, but it can tighten cash management requirements in the early phase..

What Changed On Monday:

Nigeria Market Intelligence:

Equities: profit-taking is testing the T+1 transition

What happened:

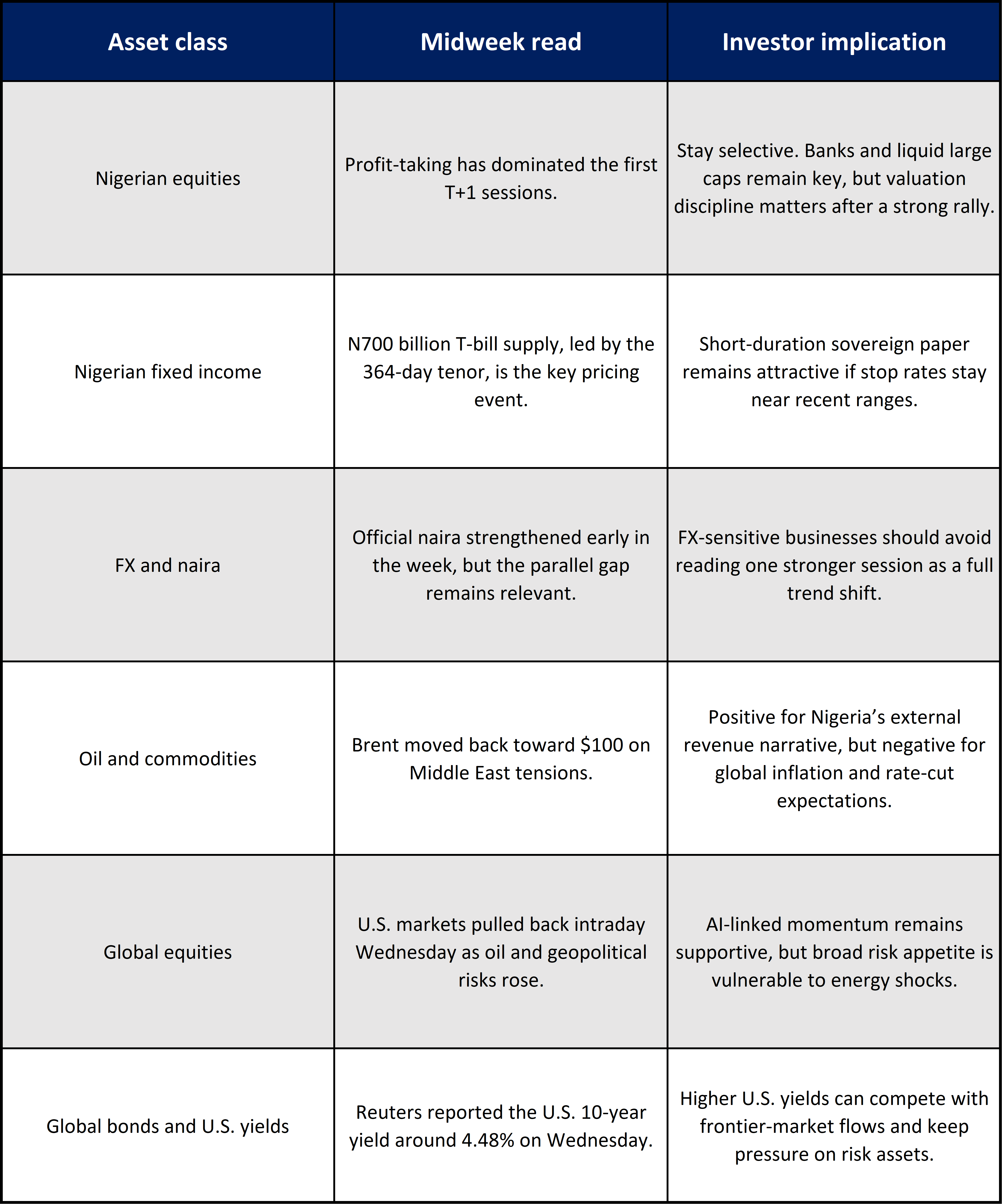

The NGX market weakened at the start of June. Monday’s session recorded a 1.13% decline, and Tuesday’s session extended the pullback with the ASI down 0.35% to 246,686.66 points. Punch reported that losses were seen in names including PZ Cussons Nigeria, NGX Group, FBN Holdings, Wema Bank, and Zenith Bank.

Why it matters:

This is not only about price declines. It is about market behaviour during a major post-trade adjustment. T+1 should improve efficiency over time, but in the first week it can force brokers, custodians, institutional investors, and foreign participants to tighten funding timelines. That may reduce speculative flexibility and reward investors with cleaner cash planning.

What to watch next:

Watch whether turnover stabilises after the first few T+1 sessions. If liquidity holds, the pullback may become a healthier repricing rather than a confidence problem.

FX: the naira improved officially, but the market still needs depth

What happened:

Nigeria reported CBN FX data showing the official naira rate at N1,361.04/$ on Tuesday, compared with N1,366.79/$ on Monday. It also reported parallel market trading around N1,395/$ on Tuesday.

Why it matters:

The official improvement helps sentiment, especially for foreign investors watching repatriation risk. But the key issue is not just the daily level. It is whether dollar supply is deep enough to support imports, portfolio flows, dividend repatriation, and corporate planning without renewed pressure.

What to watch next:

Watch official turnover, the official-parallel spread, and whether oil-related dollar inflows improve as Brent remains elevated.

Fixed income: the Treasury bill auction is the week’s yield signal

What happened:

Nigeria’s June 3 financial market pipeline includes a N700 billion CBN Treasury bill primary market auction, with N500 billion allocated to the 364-day tenor, N150 billion to 91-day paper, and N50 billion to 182-day paper.

Why it matters:

The heavy 364-day weighting is important. If demand is strong, it may reinforce the appeal of short-duration sovereign paper and keep stop rates contained. If demand is soft, the auction could reset expectations for higher yields across the short end.

What to watch next:

The bid-to-cover ratio and final stop rates matter more than the headline offer size. Strong 364-day demand would support money market funds and short-duration fixed income strategies.

Macro: inflation and GDP still frame the policy debate

What happened:

NBS data shows headline inflation at 15.69% in April 2026, with food inflation at 16.06% and core inflation at 15.86%. NBS also reports Q1 2026 real GDP growth of 3.89% year on year, above 3.13% in Q1 2025.

Why it matters:

The growth picture gives policymakers room to stay conservative, while the renewed inflation uptick reduces the urgency for aggressive monetary easing. For investors, this keeps the short end of fixed income relevant and supports selective equity exposure rather than broad risk-taking.

What to watch next:

The May CPI print will matter because it will show whether April’s rise was a temporary interruption or the beginning of a stickier inflation phase.

Global Market Intelligence:

Oil is back at the centre of the global inflation story

What happened:

Reuters reported on June 3 that Brent crude rose about 1.8% to $97.72 per barrel as Middle East tensions escalated. A separate Reuters report earlier in the day said oil prices had risen for a third straight session.

Why it matters:

For Nigeria, higher Brent can support external revenue expectations and reserve confidence. But it can also worsen global inflation psychology, delay rate cuts, strengthen the dollar, and raise import and energy-linked costs.

What to watch next:

Watch whether Brent breaks and holds above $100. That would change the inflation discussion for central banks and could affect frontier-market flows.

U.S. rates: the Fed has less room to ease quickly

What happened:

The Federal Reserve kept the federal funds target range at 3.50% to 3.75% on April 29, citing solid activity, elevated inflation, and uncertainty linked partly to Middle East developments. The next FOMC meeting is scheduled for June 16-17, 2026.

Why it matters:

A higher-for-longer Fed backdrop affects Nigeria through dollar strength, U.S. yield competition, and frontier-market risk appetite. If U.S. yields remain attractive, Nigerian assets need either stronger yields, stronger FX credibility, or stronger earnings momentum to compete for foreign capital.

What to watch next:

The May U.S. CPI release on June 10 and the June FOMC meeting on June 16-17.

U.S. labour and inflation data are not giving markets an easy easing story

What happened:

BLS reported that U.S. CPI rose 0.6% month on month and 3.8% year on year in April 2026, while core CPI rose 2.8% year on year. U.S. job openings also rose to 7.6 million in April, according to AP’s coverage of Labor Department JOLTS data. (bls.gov) (apnews.com)

Why it matters:

If inflation remains above target and labour demand remains resilient, the Fed has less incentive to cut. That can keep U.S. yields elevated and reduce the easy-liquidity tailwind for emerging and frontier markets.

What to watch next:

Friday’s U.S. employment report and whether wage pressure confirms or contradicts the JOLTS signal.

Asset Class Implications:

Ranora View:

The week so far reinforces a simple point: Nigeria’s market story is improving structurally, but investors should separate infrastructure progress from immediate price action.

T+1 settlement is a positive reform. It can reduce settlement risk, improve market discipline, and make the Nigerian market more credible for institutional capital. But the first week of implementation is likely to reward investors who understand liquidity mechanics, not those chasing headlines. Faster settlement means cash timing matters more. That could temporarily reduce speculative turnover while improving market quality over time.

For portfolios, the near-term tilt still favours a barbell approach: keep short-duration fixed income exposure where yields remain attractive, while using equity weakness to review high-quality names with earnings visibility, liquidity, and balance-sheet strength. The equity selloff does not automatically invalidate the market’s medium-term story, but it does argue against indiscriminate buying.

The biggest external risk is oil-led inflation. Higher Brent can support Nigeria’s dollar inflow story, but if it keeps the Fed hawkish and the dollar firm, foreign appetite for frontier risk may remain selective. That makes FX credibility and policy consistency more important than headline oil prices alone.

What to Watch Next:

Final stop rates and bid-to-cover ratios from the June 3 Treasury bill auction.

Whether NGX turnover stabilises after the first T+1 settlement sessions.

The official naira rate and the official-parallel market spread before Friday.

Brent crude’s ability to hold near or above $100.

U.S. payrolls on Friday and U.S. CPI due June 10.

Question for the day:

Is Nigeria’s move to T+1 settlement more likely to attract foreign portfolio investors quickly, or will investors wait to see several weeks of smooth liquidity and FX execution first?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.