Midweek Review: The MPC Hold Changes the Tone, Not the Discipline.

Ranora Market Outlook -As of Wednesday, May 20, 2026, the week’s clearest domestic signal is that the CBN has chosen policy stability over another tightening move, even as inflation edges higher.

Opening View

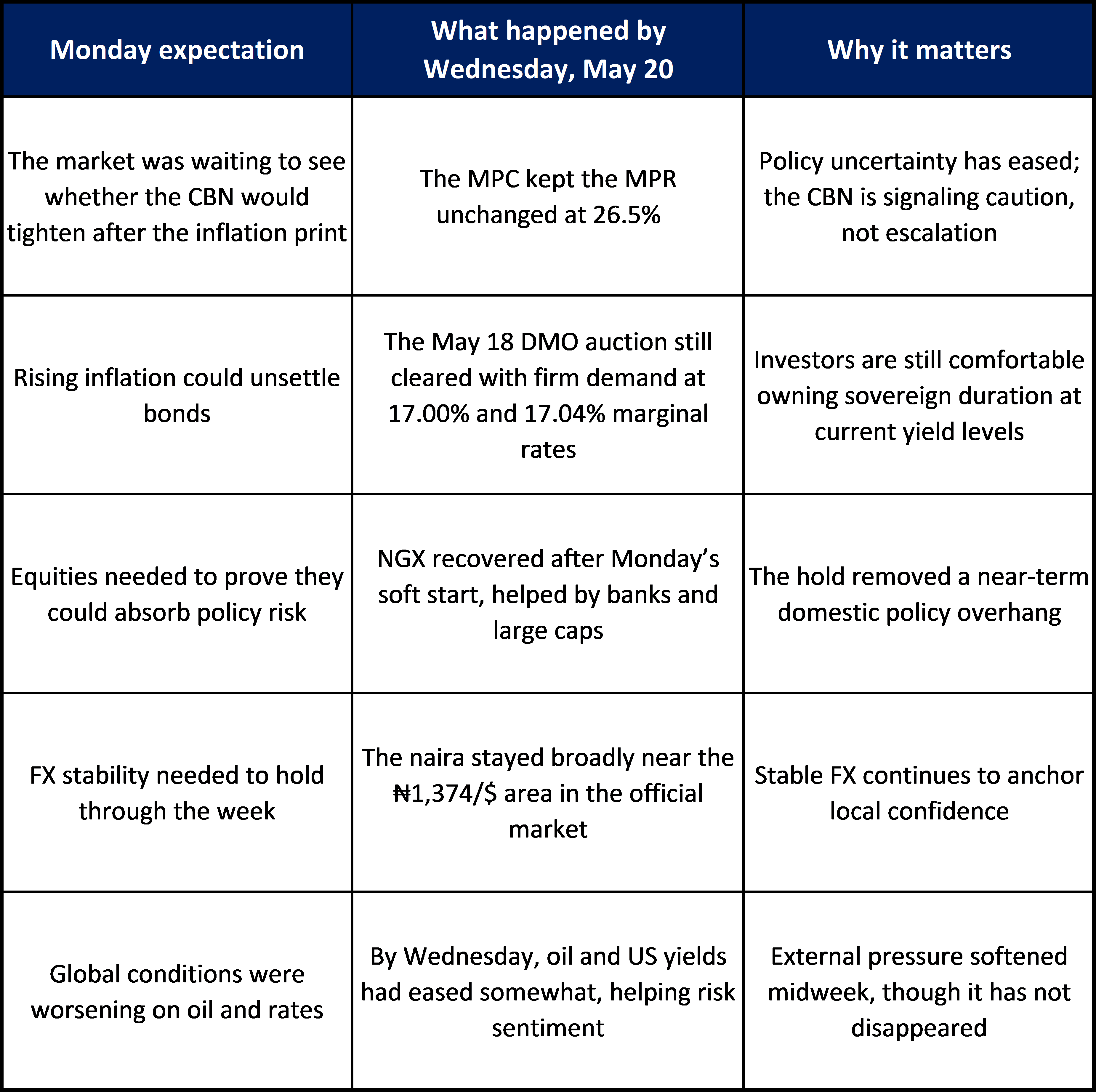

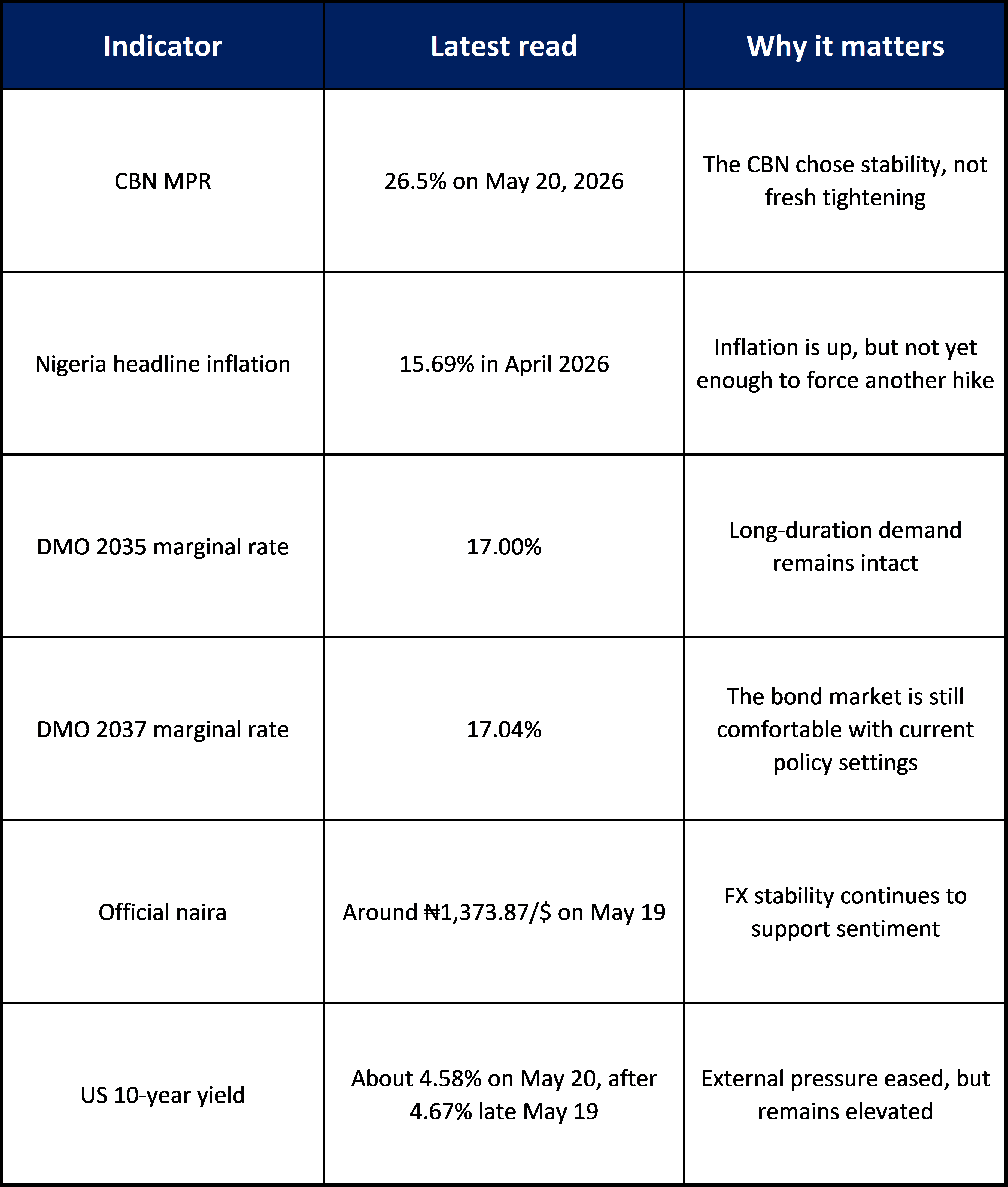

The main change since Monday, May 18, is that Nigeria’s market now has policy clarity. The Central Bank of Nigeria’s Monetary Policy Committee concluded its meeting on Wednesday, May 20, 2026, and kept the Monetary Policy Rate steady at 26.5%. That matters because the week began with a live question: would April’s inflation uptick force the CBN back into tightening mode, or would policymakers choose to wait?

They chose to wait.

That decision does not mean inflation risk has disappeared. April headline inflation still rose to 15.69% from 15.38% in March. But the hold suggests the CBN believes policy is already restrictive enough for now, and that the better course is to preserve stability while monitoring how inflation, FX conditions, and liquidity evolve. For investors, that removes one immediate domestic risk. It also helps explain why the fixed income market has remained orderly and why equities have not faced a broad repricing.

The deeper message is that Nigeria’s market is still being supported by domestic liquidity, high nominal yields, and relative FX stability. Globally, however, the backdrop is still less friendly. US yields remain elevated, the Fed looks less likely to cut this year, and oil volatility is still capable of tightening financial conditions quickly. So the week has become clearer, but not easier: local conditions are stable enough to support positioning, yet external conditions still argue for selectivity..

What Changed On Monday:

Market Pulse:

Nigerian Equities:

The market has looked resilient rather than euphoric. Monday opened softer, but Tuesday’s rebound showed that investors were willing to add selectively once policy fears eased.

Fixed Income:

This remains the strongest local signal. The DMO’s May 18 bond auction attracted solid demand despite higher inflation, and Wednesday’s MPC hold reinforces the view that yields may remain attractive without an immediate domestic shock.

FX and Naira:

The naira remains stable rather than strong. That is still useful. Stability is enough to preserve local positioning and reduce the risk of another abrupt sentiment reversal.

Oil:

Brent has eased from early-week highs, which helps reduce some inflation anxiety globally and locally. But oil is still high enough to keep energy costs and Nigeria’s external balance in focus.

Global Risk Sentiment:

The mood improved modestly by Wednesday as US yields eased and equities recovered, but the broader macro tone is still cautious.

US Yields:

The US 10-year yield pulled back from Tuesday’s highs, which gave markets some breathing room. Even so, yield levels remain elevated enough to cap enthusiasm for riskier markets.

Commodities:

Gold softened as yields and the dollar stayed firm. That tells you the market still sees inflation and rates as the dominant macro variables.

Nigeria Deep Dive: The CBN Has Chosen Stability Over Surprise

The most important Nigerian development this week is not just that the MPC held rates. It is what that hold says about the CBN’s current reaction function.

With April inflation rising to 15.69%, the committee had a case for sounding more aggressive. Instead, it kept the MPR at 26.5%. That suggests policymakers do not yet see the latest inflation move as enough to justify another tightening step. Put differently, the CBN appears to believe that the current stance is already restrictive and that the more valuable outcome now is policy continuity.

That matters for three reasons.

First, it helps the bond market. When inflation rises but the central bank does not tighten further, investors begin to focus more on carry and liquidity than on the risk of immediate policy repricing. That supports continued demand for sovereign paper.

Second, it helps equities at the margin. Nigerian stocks do not need lower rates to keep working, but they do need predictability. A steady MPR is easier for the market to digest than another hike.

Third, it supports the naira indirectly. A hold at 26.5% still leaves Nigeria with a very restrictive nominal policy rate. That gives the CBN room to argue that it is not easing prematurely and helps preserve the yield support behind local assets.

The implication is straightforward: the CBN is not pivoting, but it is also not escalating. For investors, that is a stabilizing outcome.

Global Markets Deep Dive: The Fed Still Matters More Than One Good NGX Session

The midweek relief in global markets should not be mistaken for a broader turn. Yes, oil eased. Yes, US yields came off their highs. Yes, equities found some support. But the bigger global message this week remains that the Fed is less likely to cut rates in 2026 than markets had previously hoped.

A Reuters poll published on Tuesday, May 19, showed most economists now expect no Fed cut this year. That matters directly for Nigeria because higher US rates keep the hurdle high for frontier-market inflows. Nigeria can still attract capital if the naira stays stable and local returns remain compelling, but the external environment is not doing any favors.

That is why the MPC hold is important. Nigeria does not currently have a benign global backdrop. What it does have is enough domestic policy continuity to stop local risk from being undermined by its own central bank. In this phase of the cycle, that is valuable

Chart or Table of the Day:

Ranora View:

The key investment implication from the week so far is that Nigeria’s domestic market has absorbed a potentially awkward combination of higher inflation and a high policy rate without breaking. The MPC hold at 26.5% confirms that the CBN wants to preserve restrictive conditions, but it does not see the need to tighten further yet. That is supportive for carry trades in local fixed income and constructive for selective exposure to Nigerian equities, especially where earnings resilience and liquidity support still matter more than valuation expansion.

The caution is external. US rates remain high, Fed easing expectations have been pushed back, and oil can still reprice quickly on geopolitical headlines. So this is not a week for broad risk chasing. It is a week for staying invested, but staying disciplined.

What We Are Watching Before Friday:

Whether secondary bond market yields remain stable after the policy hold.

Whether the naira stays within its recent narrow range.

Whether Brent remains contained or moves higher again on geopolitical headlines.

Whether US yields continue to ease or resume climbing.

Engagement Question:

Does the MPC’s decision to hold at 26.5% increase your confidence in Nigerian assets, or does it simply reinforce a “high rates for longer” market that requires more selective positioning?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.