Money Monday

Ranora Daily - Your daily source for reliable market analysis and news.

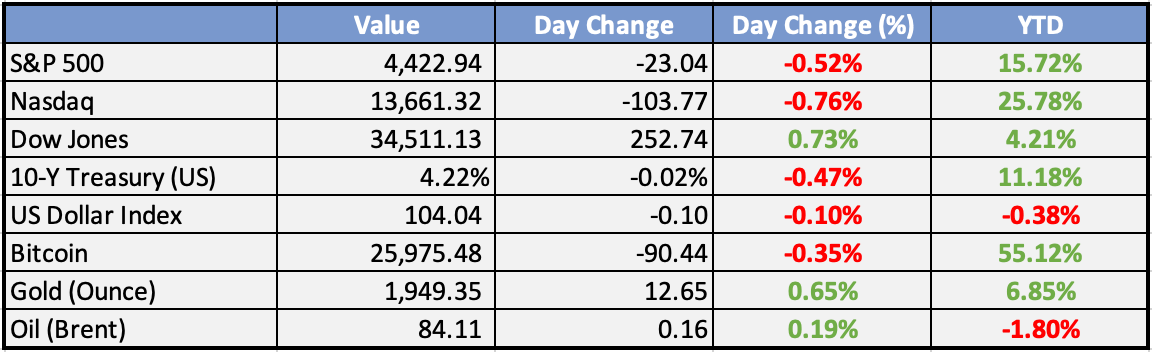

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Impact of Fuel Subsidy removal: Transport Sector GDP contracts by 50.64% in Q2 2023 - Naira Metrics

The removal of fuel subsidies has led to a 50.64% contraction in the transport sector's GDP during Q2 2023, as per the article. This substantial decline underscores the significant impact of the subsidy removal on the sector's economic performance.

Nigeria’s domestic investors dominate as portfolio investments surge by 72.83% in July - Naira Metrics

In July 2023, Nigeria experienced a notable surge of 72.83% in portfolio investments, with domestic investors taking the lead in this growth trend. The article highlights the increasing dominance of domestic investors in driving the country's portfolio investment landscape.

Global

India’s moon landing made history at a low cost - CNBC

India successfully landed its Chandrayaan-3 spacecraft on the moon, making it the fourth country to achieve this feat and the first to land near the lunar south pole. Despite a history of lunar landing challenges, India's achievement is notable due to its relatively low-cost mission, estimated at $75 million.

Labor unions are pushing hard for double-digit raises and better hours. Many are winning - CNBC

Workers across industries are demanding better pay and conditions, emboldened by job security shifts, pandemic impacts, and increasing profits. Over 320,000 workers in 230 strikes this year seek improved quality of life and reflect higher labor union approval and income inequality.

Weekly Investment Watchlist

Market Commentary

Asia and Australia:

Asian stock markets concluded Monday with gains. Hang Seng exhibited a 3% gap up at the open but moderated throughout the day to close around 1% higher, following a similar pattern in mainland markets. Japan saw gains leading the way.

At Jackson Hole, BOJ Governor Ueda mentioned on Saturday that Japan’s inflation remains slightly below the 2% target. He continued to justify the maintenance of easing policies, aligning with our earlier expectations. We anticipate minimal policy changes through the end of the year.

China implemented a 50% reduction in stock taxes and urged banks to purchase stocks. However, the market response was underwhelming. Despite an initial gap up, the gains were almost entirely reversed.

After a 17-month trading suspension, Evergrande, a major Chinese developer, witnessed its shares plummet by nearly 87%. The company also reported a loss of 39.25 billion yuan ($5.38 billion) for the six months ending in June, accompanied by total liabilities amounting to 2.39 trillion yuan.

Profits for industrial firms in China declined by 15.5% year-on-year from January to July, a slower rate compared to the 16.8% drop observed from January to June. Solely for July, profits fell by 6.7% year-on-year, in contrast to an 8.3% drop in June.

Australian retail sales in July rose by 0.5% month-on-month, surpassing the consensus estimate of a 0.3% increase. This rebound follows a contraction of 0.8% in June. The gain was led by discretionary goods categories, including a 2.0% rise in clothing, footwear, and personal accessory retailing, as well as a 3.6% increase in department store retailing.

Europe, Middle East, Africa:

European equity markets showed gains but retreated from their best levels. This followed the first positive close in four weeks on Friday.

Eurozone’s July M3 witnessed a decline of 0.4% year-on-year, differing from the expected 0.0% figure. This marked the first negative reading for broad money growth.

At Jackson Hole, ECB President Lagarde expressed concerns about the need for a new central bank playbook due to factors such as tighter labor markets, the green transition, and economic fragmentation into competing blocs.

The probability of an ECB hike in September is considered uncertain. Leading indicators indicate the potential for lower inflation ahead.

Germany’s ruling Social Democratic Party plans to vote on a proposal for a rent freeze as a measure to curb inflation.

The EU gas market remains tense due to factors such as Norway’s flows and potential strikes in Australia.

The Americas:

Anticipated growth of US payrolls for August is expected to slow to 170,000, which would result in the lowest three-month average since the beginning of 2021.

Hostess Brands is contemplating a sale after receiving takeover interest from major snack food manufacturers.

The trucking industry forecasts an increase in demand during the second half of the year, as the trend of retailer de-stocking largely concludes.

Realty Income confirms its acquisition of a 21.9% stake in Bellagio from BREIT.

Bullish sentiment among AAII respondents fell by 3.6 percentage points to 32.3% in the week ending on August 23. This is below the historical average of 37.5% for the second consecutive week.

The Week Ahead:

Monday:

China PBOC Interest Rate Decision

Tuesday:

US Existing Home Sales Change (MoM)(Jul)

Wednesday:

S&P Global/CIPS Composite PMI (Aug) PREL (UK)

Retail Sales (MoM)(Jun) (Canada)

S&P Global Manufacturing PMI (Aug) PREL(US)

Consumer Confidence (Aug) PREL (EU)

Thursday:

ECB Monetary Policy Meeting Accounts (EU)

Durable Goods Orders (Jul)

Friday:

GFK Consumer Confidence (Aug) (UK)

Investment Tip of The Day

Capitalizing on Market Volatility: During volatile periods, consider deploying capital into quality assets at attractive prices. Maintaining a long-term perspective helps capitalize on short-term market fluctuations.

Meme of the Day