Money Monday

Ranora Daily - Your daily source for reliable market analysis and news.

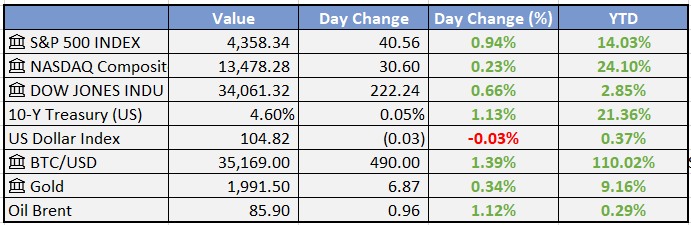

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Fitch affirms Nigeria’s rating, retains stable outlook on reforms - Business day

Fitch Ratings has affirmed Nigeria's credit rating and maintained a stable outlook, citing the country's ongoing reform efforts as a key factor. This affirmation suggests confidence in Nigeria's economic policies and reforms, despite challenges faced in areas like security and fiscal management.

Japanese Govt Upbeat about Nigeria’s Economy, Task FG on Sound Economic Policies - This Day

The Japanese government is optimistic about Nigeria's economic prospects and has encouraged the Nigerian government to implement sound economic policies. Japan sees Nigeria as a key economic partner in Africa and is keen on fostering stronger economic ties between the two nations. This positive outlook is indicative of Japan's interest in Nigeria's economic growth.

Nigeria fails global money laundering review at FATF plenary - Punch

Nigeria failed its global money laundering review at the Financial Action Task Force (FATF) plenary. The FATF expressed concerns about the country's progress in addressing anti-money laundering and counter-terrorism financing issues. This outcome could have implications for Nigeria's international financial standing.

Global

Elon Musk debuts ‘Grok’ AI bot to rival ChatGPT - CNBC

Grok, the first AI technology from Elon Musk's new company, xAI, is designed to be witty and answer "spicy questions" other AIs might avoid. While xAI hails Grok's capabilities, they acknowledge its potential to generate false or contradictory information. The prototype, in early beta, has been training for two months and is currently available to a limited number of users.

Bankers seek legal cover after backing $1.5T of ESG debt - Bloomberg

Bankers in the rapidly growing ESG (Environmental, Social, and Governance) debt market are increasingly seeking legal safeguards against potential greenwashing accusations. Sustainability-linked loans (SLLs), a $1.5 trillion market, allow borrowers and lenders to tie loans to environmental or social metrics.

Oil up 1.5% as Saudi Arabia and Russia stick to supply cuts - Reuters

Oil prices surged after Saudi Arabia and Russia confirmed extended voluntary oil supply cuts until year-end, lifting Brent crude by 1.47% to $86.14 and West Texas Intermediate by 1.6% to $81.80. Both countries pledged to maintain voluntary cuts – Saudi Arabia with an extra 1 million bpd and Russia with an additional 300,000 bpd until December.

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian stocks ended higher across the region on Monday. South Korea’s Kospi stood out, ending 5.7% higher, with this surge occurring alongside the re-imposition of a short selling ban. Hong Kong also had a strong day but was overshadowed by Shenzhen. Japan stocks reached a six-week high, while Taiwan, Southeast Asia, and India all recorded solid gains. Australia, although higher, underperformed.

The South Korean government announced the re-imposition of its short-selling ban following naked short selling accusations against foreign brokers and retail investor pressure. This led to the surge of recently sold-off stocks with high short positions, such as battery-makers and industrials, by double-digit percentages.

Indonesia’s Q3 GDP Growth rate declined to +1.6% quarter-on-quarter from 3.86% in Q2, which brought the year-on-year GDP down to 4.94%. This represents the weakest growth since 2013 and was driven by a drop in household consumption and declines in government spending and exports.

BOJ Governor Ueda noted that the likelihood of sustained 2% inflation is rising but considered it too early to draw a definitive conclusion. The BOJ September meeting minutes featured discussion on upside risks to the inflation outlook. Japan’s services activity fell to a year-to-date low due to softening demand and a pickup in input costs.

Stocks of Chinese brokerages surged after the securities watchdog vowed to support M&A of leading firms in a bid to create top-ranked investment banks.

Australia was awaiting its Central Bank interest rate decision, scheduled for tonight at 10:30pm ET, which would be early Tuesday in Australia and Asia. Consensus favored a 25-bp hike to 4.35% after hotter-than-expected inflation numbers in Q3. The new governor has remained cautious with hikes in the face of the deteriorating housing market.

Europe, Middle East, Africa:

European equity markets trimmed earlier gains to trade lower. Real Estate, Chemicals, and Construction & Materials were the worst performers, while Travel & Leisure, Basic Resources, and Oil & Gas performed the best.

German Factory order continued to decline, coming in at 0.2% compared to 1.9% in the previous month. The number came in better than expected, primarily led by machinery and equipment, while autos and transport equipment took a hit. Given the PMIs and GDP Growth seen, there remained caution regarding European equities, particularly industrials.

Mixed Services and Composite HCOB PMI data emerged from Europe on Monday. Spain and France showed slight improvements, but Germany and Italy reported lower figures. Overall, Euro Area Services PMI declined to 47.8 from 49.7, and the Composite PMI dropped to 46.5 from 47.2. While not great for growth, this was seen as positive for sticky core inflation, which has posed challenges to inflation control.

In EU trade, Travel & Leisure was the top-performing sector, driven by airlines. Performance was reportedly boosted by strong H1 results from Ryanair and upbeat comments on pricing power. The company forecast a record annual profit after airfares soared 24% during the summer season.

The Americas:

Depressed sentiment and positioning indicators were noted as facilitators of this week’s significant rebound. The AAII bull-bear spread fell 12.1pp to -26.0%, reaching its lowest level since late March. The AAII bull-bear ratio stood at 0.48. According to Goldman Sachs, since 1987, the ratio has been below 0.5 102 times, or 5.39% of observations. It was pointed out that the average S&P return for the next one month following such cases is +2.6%, with a 74% positive hit rate.

Data from the Federal Reserve H.8 last week showed slightly higher securities and solid loan growth compared to the prior week. Total securities increased by $3.4 billion, with Treasury/agency securities rising by $6.5 billion, while other securities decreased by $3.9 billion. Overall, loans rose by $25.1 billion compared to the prior week, with commercial loans declining by $6.2 billion, while residential loans increased by $3.3 billion.

The Week Ahead:

Monday:

Tuesday:

Wednesday:

Thursday:

Unemployment Claims (US)

Friday:

GDP m/m (UK)

Prelim UoM Consumer Sentiment (US)

Investment Tip of The Day

Assess Management Succession: For individual stock investments, assess the quality and transparency of a company's management succession plan. An orderly transition can mitigate uncertainty and risks.

Meme of the Day