Money Monday

Ranora Daily - Your daily source for reliable market analysis and news.

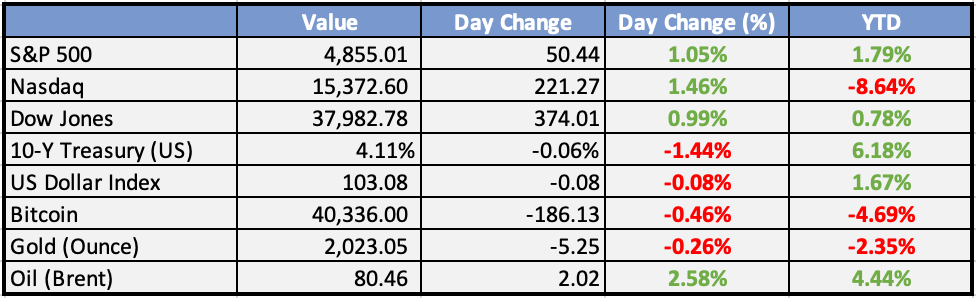

Market Data

Local

Global

*Data as of 6pm WAT

Market News

Local

Tinubu tax panel asks states to suspend low-revenue taxes - Punch

The Presidential Committee on Fiscal Policy and Tax Reforms says it is meeting with state governors in order to reach an agreement for states to suspend some low-revenue taxes.

Odu’a Investment eyes NGX listing - Punch

Odu’a Investment Company Limited has revealed plans to list on the Nigerian Exchange. The Chairman of the conglomerate, Bimbo Ashiru, disclosed this on the floor of the exchange during a closing-gong ceremony on Friday.

CBN still short of forex to clear backlog (Fitch) - Vanguard

Fitch, one of the leading global credit rating agencies, has said that the Central Bank of Nigeria (CBN) still lacks sufficient foreign exchange (forex) to clear the backlog of demand in the country.

CBN to hold first monetary policy meeting under new gov in February - BusinessDay

The Central Bank of Nigeria will hold its Monetary Policy Meeting in 2024 on Monday and Tuesday , February 26 and 27, according to a one-paged confidential document seen by BusinessDay.

Global

Market Commentary:

Overview:

Upbeat sentiment prevailed in equities, propelling the S&P500 to a record-high gain of 1.2%. Notably, US consumer inflation expectations declined, contributing to a generally softer US dollar. The current market calendar appears notably light.

Currencies/Macro:

The US dollar showed signs of softening, with EUR/USD marking a 0.2% increase to 1.0895.

Other currency movements included GBP/USD slightly softening to 1.2700.

US consumer sentiment, as measured by the University of Michigan, sharply rose to 78.8 (est. 70.1, prior 69.7).

Expectations surged from 67.4 to 75.9, and current conditions rose from 73.3 to 83.3.

Inflation expectations were below expectations, with the 1yr ahead measure at 2.9%, the lowest in three years, and the 5-10yr at 2.8%.

US home sales in December fell by -1.0% (est. +0.3%), while the median price reached a record high of USD 389k.

Various Fed officials provided insights, including Chicago Fed president Goolsbee emphasizing the need to consider unexpected progress in inflation. Atlanta Fed president Bostic reiterated a potential for rate cuts in Q3, contingent on reaching a 2% target before moving away from a restrictive stance.

San Francisco Fed president Daly deemed it premature to anticipate policy adjustments, emphasizing the absence of consistent evidence on inflation or early labor market challenges.

Swiss National Bank Chair Jordan noted their battle against inflation, indicating no forecasted rate increases and an independent stance from expected Fed easing. He highlighted the impact of CHF strength on their inflation outlook.

Interest Rates:

The US 2yr treasury yield initially rose from 4.34% to 4.42%, retracing to 4.38%, while the 10yr yield fell from 4.16% to 4.12% via 4.19%.

Markets priced the Fed funds rate, currently 5.375% (mid), to remain unchanged at the next meeting on February 1, with a 45% chance of a cut in March. Noteworthy is the absence of Australia-related rate information.

Credit spreads remained positive, with Main tightening to 60 and CDX slightly tighter at 54.5. US IG credit was flat to a bp better, extending the strong start to the year.

Notably, primary markets saw little activity, with La Banque Postale’s EUR750M covered deal being the only notable transaction.

Euro supply reached ~EUR257bn (including SSA), and the US closed last week at USD149bn of IG supply YTD, requiring ~USD26bn to reach the January 2017 record.

Commodities:

Geopolitical tensions in the Middle East escalated, affecting crude markets despite supply concerns. The February WTI contract closed down 0.9% at $73.41, and the March Brent contract closed down 0.68% at $78.56.

Notably, Libya restarted oil exports, while disruptions in US oil production occurred due to extreme cold weather. Estimates suggested significant idling of crude and refining capacity.

A fire broke out at a Baltic Sea terminal belonging to Novatek, Russia’s largest LNG producer, following a suspected drone attack.

Metals experienced mixed movements, with copper up 0.8% at $8,380 and aluminum rising 0.4% to $2,172. Nickel fell 0.7% to $16,040.

The Sulawesi Mining Investment plant in Indonesia shut down a nickel smelter due to an overflow of hot slag. Andrew Forrest’s Wyloo private company planned to put the Kambalda nickel mine into care and maintenance from May 31.

Iron ore markets regained ground, with the February SGX contract up $2.15 at $129.70. Tata announced the shutdown of two blast furnaces in the UK, aiming to reverse a decade of losses at the Port Talbot plant. China Steelhome reported a rise in iron ore port inventory for the 9th consecutive week.

Day ahead:

Eurozone:

US:

December’s leading index in the US is likely to show signs of activity dampening (market f/c: -0.3%).

The Week Ahead:

Monday:

Tuesday:

Wednesday:

Flash Manufacturing PMI (UK)

Flash Services PMI (UK)

Flash Manufacturing PMI (US)

Flash Services PMI (US)

Thursday:

Main Refinancing Rate (EA)

Advance GDP q/q (US)

Unemployment Claims (US)

Friday:

Core PCE Price Index m/m (US)

Investment Tip of The Day

Monitor Regulatory Scrutiny in Tech: Given increased regulatory scrutiny in the tech sector, assess how companies manage regulatory challenges and potential impacts on their operations and market share.

Service Spotlight of the week - Advisory Services

Meme of the Day