Money Monday

Ranora Daily - Your daily source for reliable market analysis and news.

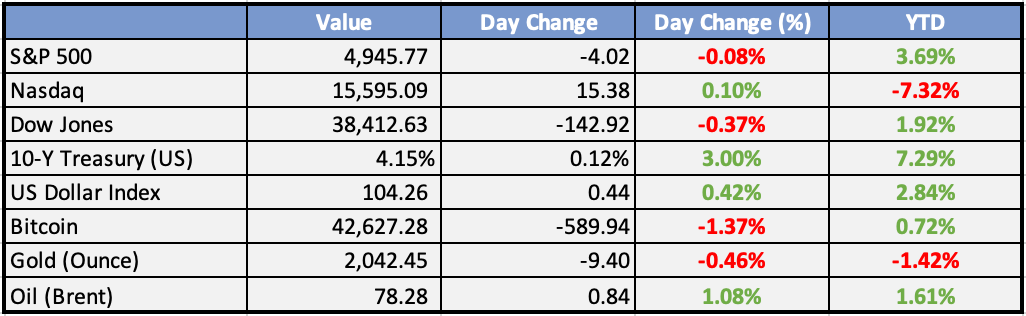

Market Data

Local

Global

*Data as of 6pm WAT

Market News

Local

NAFEM: Dollar supply rises by 180% as banks sell $440m - Punch

Dollar supply in the official foreign exchange market rose by 180.59 percent to $440.13m on Friday.

Consortium gets $5m grant to boost dairy sector - The Guardian

As part of efforts to boost the productivity and sustainability of the Nigerian dairy sector, the Bill and Melinda Gates Foundation has given the Value4Dairy Consortium led by FrieslandCampina, five million dollars grant.

Shell to build dedicated facility for gas supply to Dangote - The Guardian

hell Petroleum Development Company of Nigeria Limited (SPDC) has concluded plans to supply gas to Dangote Fertiliser and Petrochemical Plant in Lekki for 10 years.

Global

Global ESG Bond Sales Reach $150 Billion in Busiest January Ever - Bloomberg

Sustainable bond sales saw the busiest January on record as lower borrowing costs ignited a deal blitz as top underwriters of the debt line up more sales.

Market Commentary:

Asia and Australia:

S&P BSE Sensex ended down by 0.49% at 71,731.42, with the NSE Nifty settling 0.38% lower at 21,771.70.

Top performers included Tata Motors, jumping 5.8% with over a two-fold rise in December-quarter profit.

Coal India surged 5.1%, while Cipla, Sun Pharma, and BPCL all rose around 3%.

S&P ASX 200 Index slumped 1.0% to 7,625.90, and the All Ordinaries Index closed 1.0% lower at 7,855.40, driven by a decline in resources stocks.

Silver Lake Resources plummeted 11.5%, while Red 5 added 3% after a merger agreement. Evolution Mining and Northern Star lost 4.6% and 3.8%, respectively.

New Zealand's S&P/NZX 50 Index finished marginally lower at 11,928.70.

South Korea's Kospi dropped 0.9% to 2,591.31 ahead of the Lunar New Year, with Samsung Electronics falling 1.2% after Chairman Lee Jae-yong's acquittal in a financial crimes case.

Australian markets fell sharply ahead of the Reserve Bank of Australia's interest rate decision scheduled for Tuesday.

Europe, Middle East, and Africa:

The SMI ended with a 0.31% gain at 11,274.47, fluctuating between 11,227.45 and 11,295.09.

Lonza Group saw a 3.25% climb, while Alcon, Swiss Re, Nestle, and Kuehne & Nagel gained between 1.36% and 1.61%.

Zurich Insurance Group, Logitech International, Novartis, Givaudan, and Sonova gained 0.4% to 0.8%.

The pan-European Stoxx 600 slightly decreased by 0.05%, with the UK's FTSE 100, Germany's DAX, and France's CAC 40 down 0.04%, 0.08%, and 0.03%, respectively. Switzerland's SMI climbed by 0.31%.

In the UK market, Ashtead, JD Sports Fashion, Howden Joinery, Airtel Africa, Barclays, Weir Holdings, Vodafone, and Glencore experienced losses between 2% and 5%.

Lloyds Bank dropped 1.4% after reports that Iran evaded sanctions using accounts at Lloyds and Santander.

Ocado Group surged nearly 4%, while GlaxoSmithKline advanced by about 3%. Other notable gainers include Croda International, Diageo, Smith & Nephew, Informa, Unilever, Haleon, Flutter Entertainment, Burberry Group, and Scottish Mortgage, with gains ranging from 1% to 2%.

The Americas:

Chances of a March rate cut dropped to 14.5% after last week's Fed meeting and Powell's comments, per CME Group's FedWatch Tool.

ISM reported an increase in services PMI to 53.4 in January from a revised 50.5 in December, signaling sector growth.

The price index surged to 64.0 in January from 56.7 in December, indicating a substantial acceleration in price growth.

Gold stocks show significant weakness, with the NYSE Arca Gold Bugs Index slumping by 2.6%.

Investment Tip of The Day

Seek professional advice when needed. Consider consulting with a qualified financial advisor or investment professional when making complex investment decisions. Their expertise can provide valuable guidance tailored to your specific needs.Service Spotlight of the week - Wealth Management

Meme of the Day

Disclaimer: The information contained in this report is intended for informational purposes only and should not be considered as investment advice. The information is obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed.