Money Monday- Nigeria Tightens Liquidity While Global Energy Markets Shift

Ranora Daily - Your daily source for reliable market analysis and news.

Market Overview

Good evening investors, and welcome to the start of a new trading week.Markets are opening the week with a mix of liquidity tightening, expansion-driven corporate activity, and rising global geopolitical risks. In Nigeria, investor focus remains on the Central Bank’s aggressive liquidity management, major industrial expansion plans, and continued pressure in the downstream energy market following another fuel price adjustment by Dangote Refinery. Globally, energy supply disruptions, sanctions-related tensions, and persistent inflation trends across major economies continue to shape investor sentiment. In today’s edition, we break down the developments influencing market positioning and the sectors likely to remain in focus as the week unfolds.

Nigerian News & Market Update

Financial Services

Group Completes SEC Recapitalisation Ahead of 2027 Deadline:

The company has completed its SEC recapitalisation requirements ahead of the 2027 deadline, strengthening its capital base and regulatory compliance position. - Leadership

CBN Sells ₦3.3trn OMO Bills to Banks, Foreign Investors:

The Central Bank of Nigeria sold ₦3.3 trillion worth of OMO bills to banks and foreign investors as part of liquidity management efforts aimed at stabilizing the financial system and controlling inflationary pressure. - Dmarketforces

Energy

Dangote Eyes Kenya for $17bn Refinery Project:

Dangote Group is considering Kenya for a proposed $17 billion refinery project as part of efforts to expand its energy footprint and strengthen refining capacity across Africa.- Punch

Construction / Infrastructure

Julius Berger Retains West Africa Construction Award

Julius Berger has retained its position as West Africa’s leading construction and infrastructure company, reinforcing its reputation for engineering excellence and regional infrastructure development. - Punch

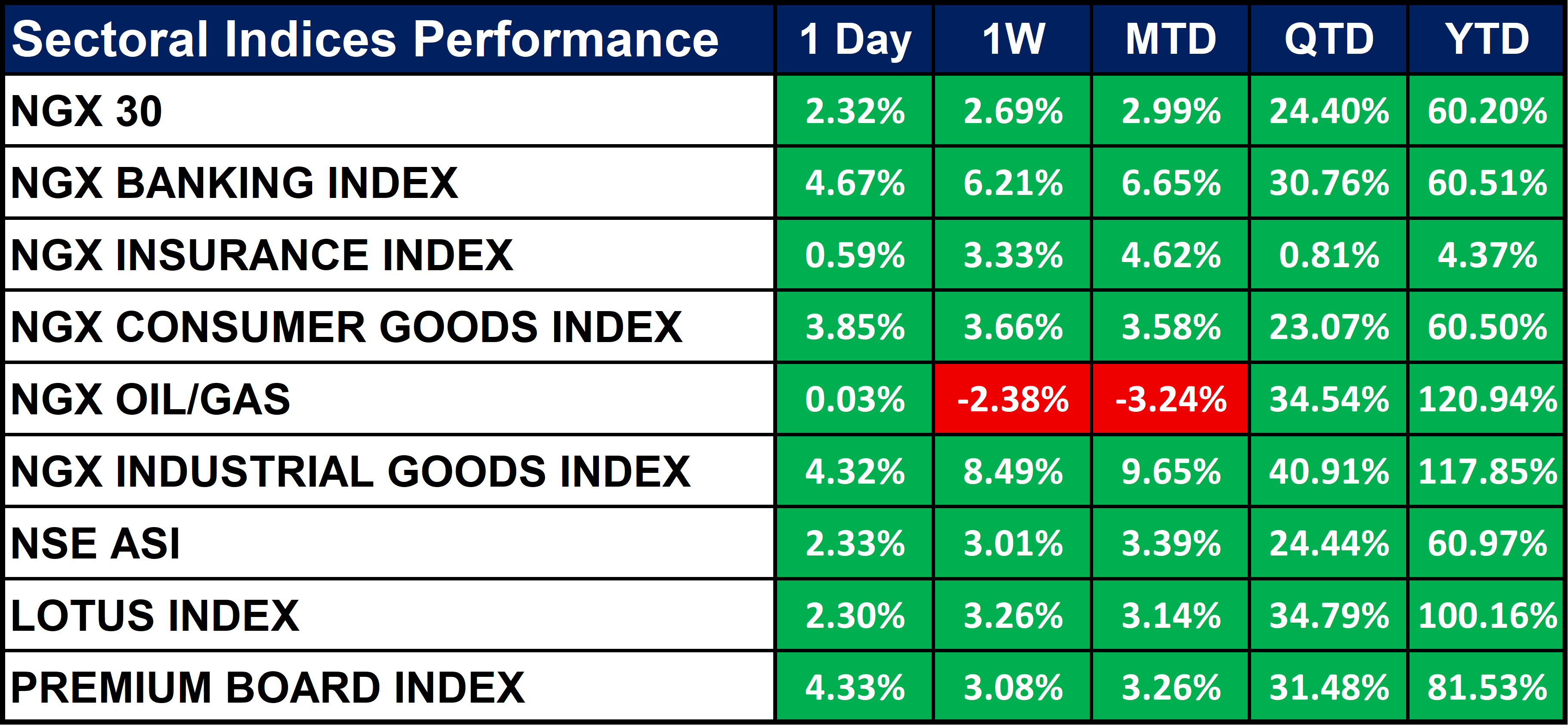

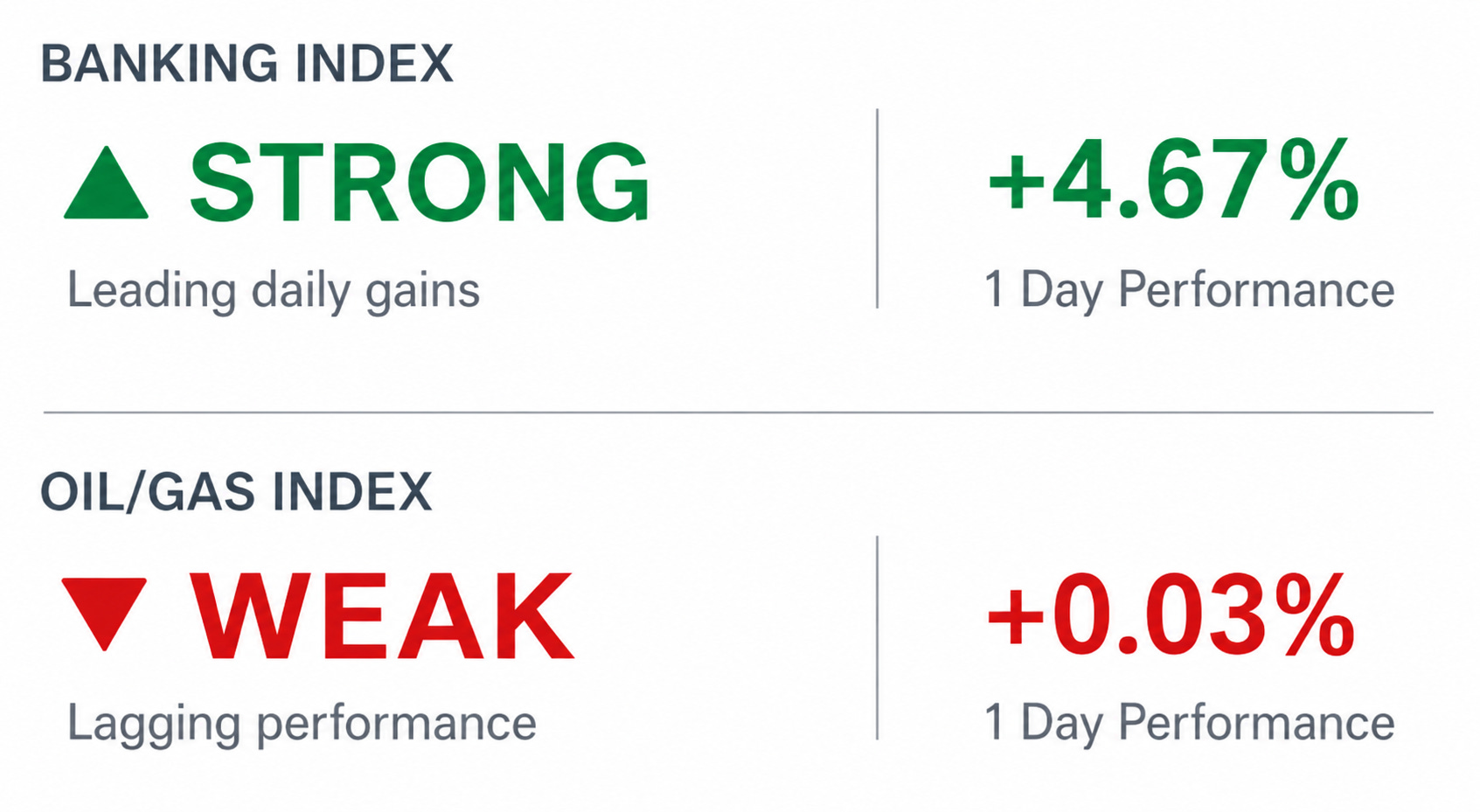

Nigeria Sectoral Indices Performance

The table below shows that the Nigerian equities closed strongly bullish, with broad-based gains across major sectors driven by renewed investor confidence and sustained buying momentum. The Banking Index emerged as the top daily performer, while Industrial Goods and the Premium Board Index also posted significant gains, reflecting strong institutional participation. Meanwhile, the Oil & Gas Index recorded the weakest performance despite remaining marginally positive, indicating cautious positioning in the energy sector amid ongoing market rotation.

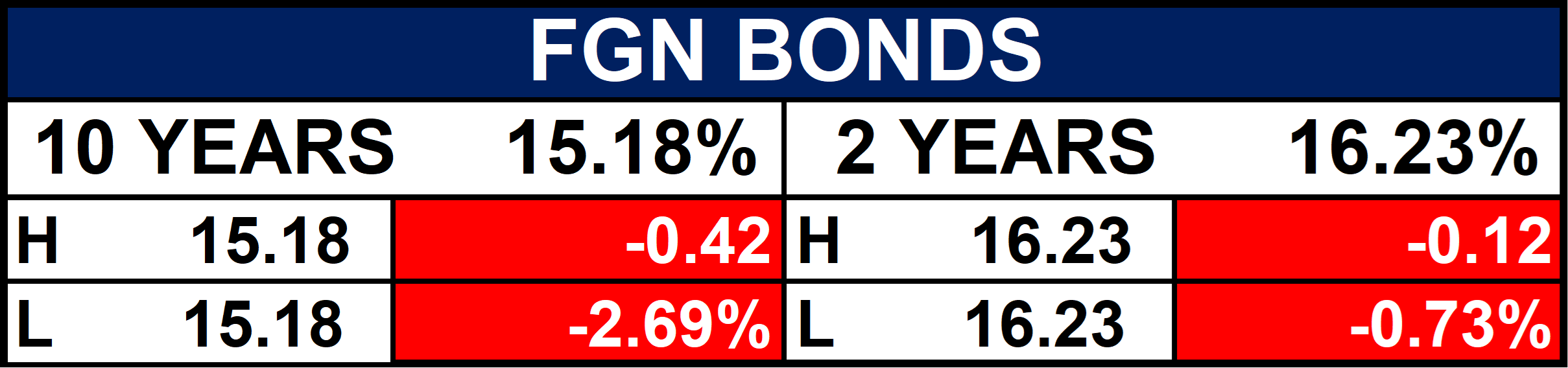

Fixed Income (FGN Bonds)

Corporate Action

Global News & Market Update

Geopolitics (Middle East & Europe)

UK Sanctions Iran-Linked Network Over Security Threats:

The United Kingdom imposed sanctions on an Iran-linked network accused of supporting attack plots and financing operations, escalating geopolitical tensions and increasing pressure on Iran. - Reuters

Energy (Asia / Middle East)

Japan to Receive First Central Asian Crude Since Iran Conflict:

Japan is set to receive its first crude oil shipment from Central Asia following disruptions linked to the Iran conflict, as importers seek alternative energy supply sources.. - Reuters

Macroeconomy (South America)

Colombia’s Inflation Edges Higher in April:

Colombia’s annual inflation rate rose slightly in April, highlighting persistent price pressures despite ongoing monetary tightening efforts by policymakers. - Reuters

Macroeconomy (Europe)

Norway’s Core Inflation Rises in Line With Expectations:

Norway’s core inflation increased in April in line with market expectations, reinforcing expectations that policymakers may maintain a cautious monetary policy stance. - Reuters

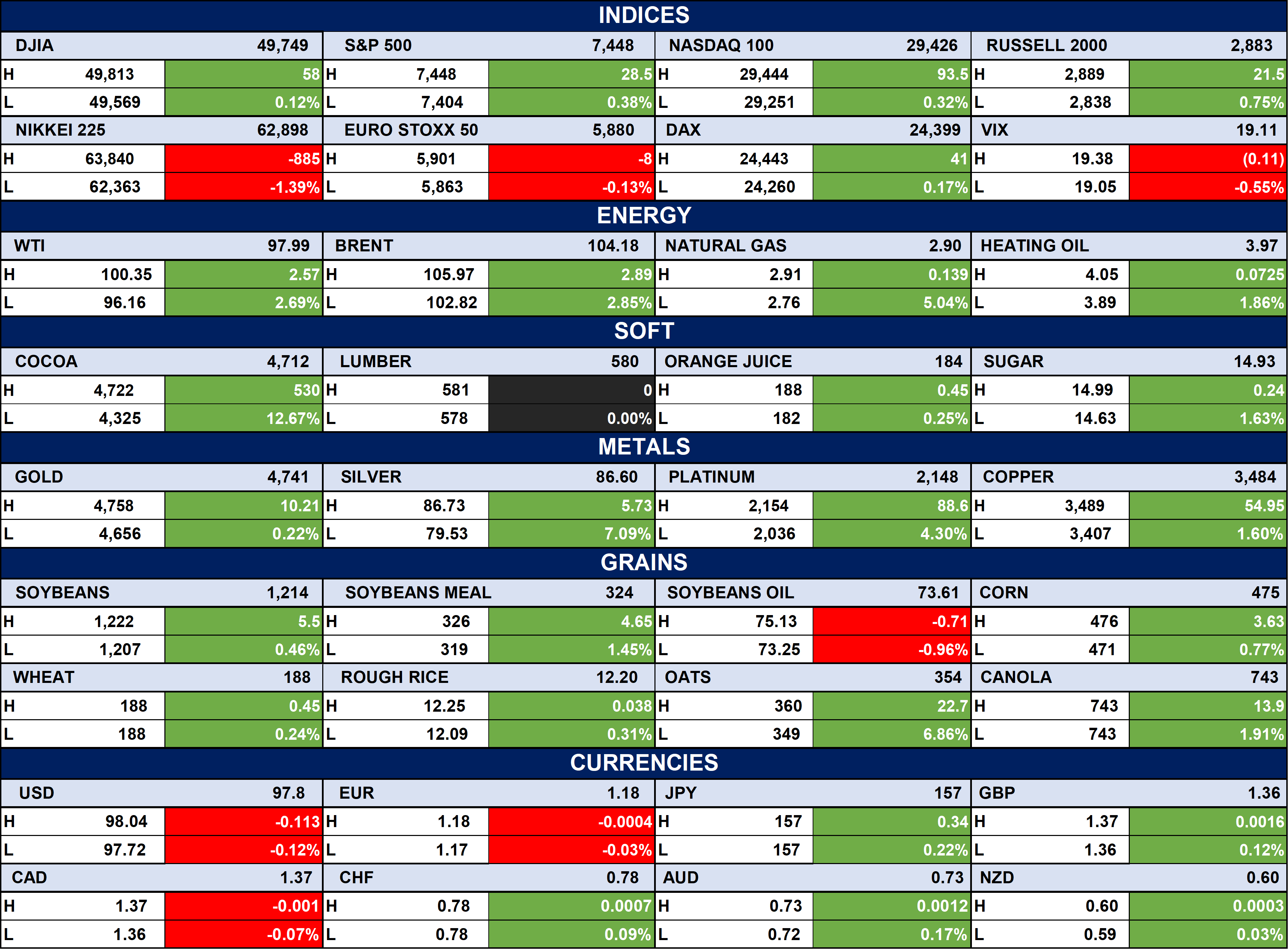

Indices, Commodities & Currencies

The table below shows that the Global markets closed with a cautiously positive tone, supported by gains in major U.S. indices and strong momentum across energy, metals, and agricultural commodities. Oil prices and natural gas advanced sharply amid ongoing supply concerns, while cocoa, silver, and oats led commodity gains, reflecting sustained demand and inflation-sensitive positioning. Meanwhile, mixed performances across European and Asian equities alongside a softer U.S. dollar suggest investors remain selective as they navigate global macroeconomic and geopolitical uncertainties.

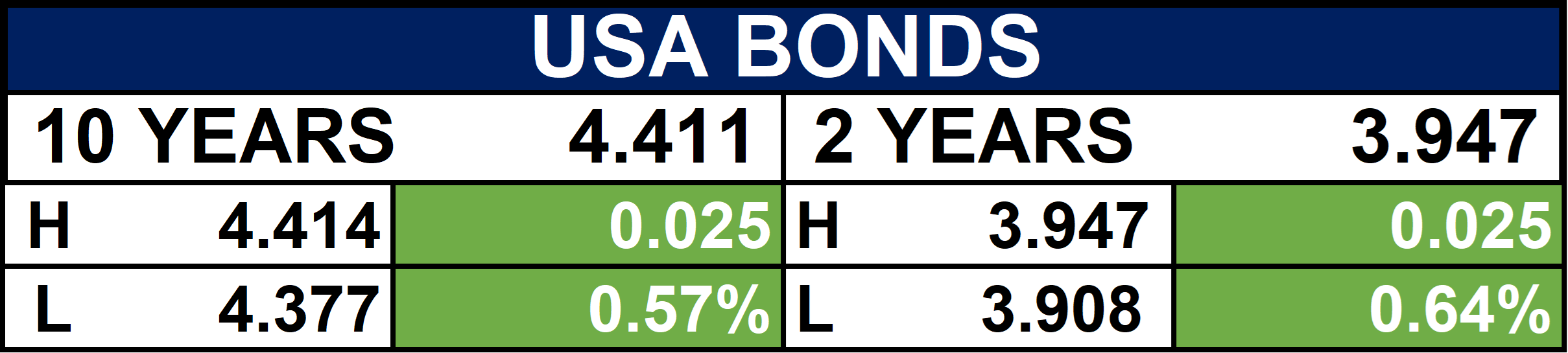

Fixed Income (USA Bonds)

Conclusion

Markets begin the week with a cautious but opportunity-driven tone, as tighter liquidity and corporate expansion support selective strength across financials, infrastructure, and industrial sectors. Globally, geopolitical tensions, energy supply shifts, and persistent inflation remain key drivers of investor sentiment and commodity prices. Overall, investors are expected to remain selective, focusing on fundamentally strong sectors while monitoring liquidity, oil prices, and global policy signals for market direction.

Will tighter liquidity in Nigeria and rising global energy tensions strengthen defensive positioning or trigger fresh opportunities across key sectors before midweek?

Stay with Ranora this Wednesday as we track how these market trends evolve and uncover the next signals shaping investor sentiment locally and globally.

Thanks for reading Ranora Consulting! Subscribe for free to receive new posts and support my work.