Money Monday- Nigerian Recapitalisation Deadlines, Sectoral Shifts, and Global Energy Tensions

Ranora Daily - Your daily source for reliable market analysis and news.

Market Overview

Good morning and welcome to today’s market briefing. Investors should watch Nigeria closely as NAICOM maintains the July 2026 insurance recapitalisation deadline, while Providus Bank reassures compliance and Guinea Insurance raises ₦5.8bn in fresh capital. Globally, energy markets remain volatile with Saudi Aramco cutting crude supplies to Asia and geopolitical developments in Iran and Russia influencing commodity flows.

Nigerian News & Market Update

Insurance recapitalisation: NAICOM rules out deadline extension:

NAICOM insists the July 31, 2026 insurance recapitalisation deadline is final, urging firms to comply or consider mergers. - Punch

Guinea Insurance signs ₦5.8billion Rights Issue:

Guinea Insurance launched a ₦5.8billion rights issue to boost capital, expand operations, and enhance competitiveness. - Punch

Cutix notifies NGX of sudden executive shake-up:

Cutix Plc announced a sudden leadership shake-up, replacing its CEO and CFO with interim internal executives while searching for permanent successors. - Punch

Dangote Refinery Sells 12 Cargoes Of Petroleum Products To 5 African Countries:

Dangote Petroleum Refinery exported 12 cargoes of refined fuel to five African countries, boosting regional energy supply and trade. - Leadership

Providus Bank dismisses recapitalisation fears, cites ₦65billion capital:

Providus Bank Limited affirmed it has met recapitalisation requirements with a ₦65billion capital base, dismissing compliance concerns. - TheSun

SEC raises capital thresholds for market operators:

The Securities and Exchange Commission has sharply increased capital requirements for market operators, with broker-dealers now needing ₦2billion and top asset managers up to ₦10billion. Firms must submit compliance plans by April 2026, with a 2027 deadline, while stricter rules exclude borrowed funds and encourage mergers for weaker players. - Punch

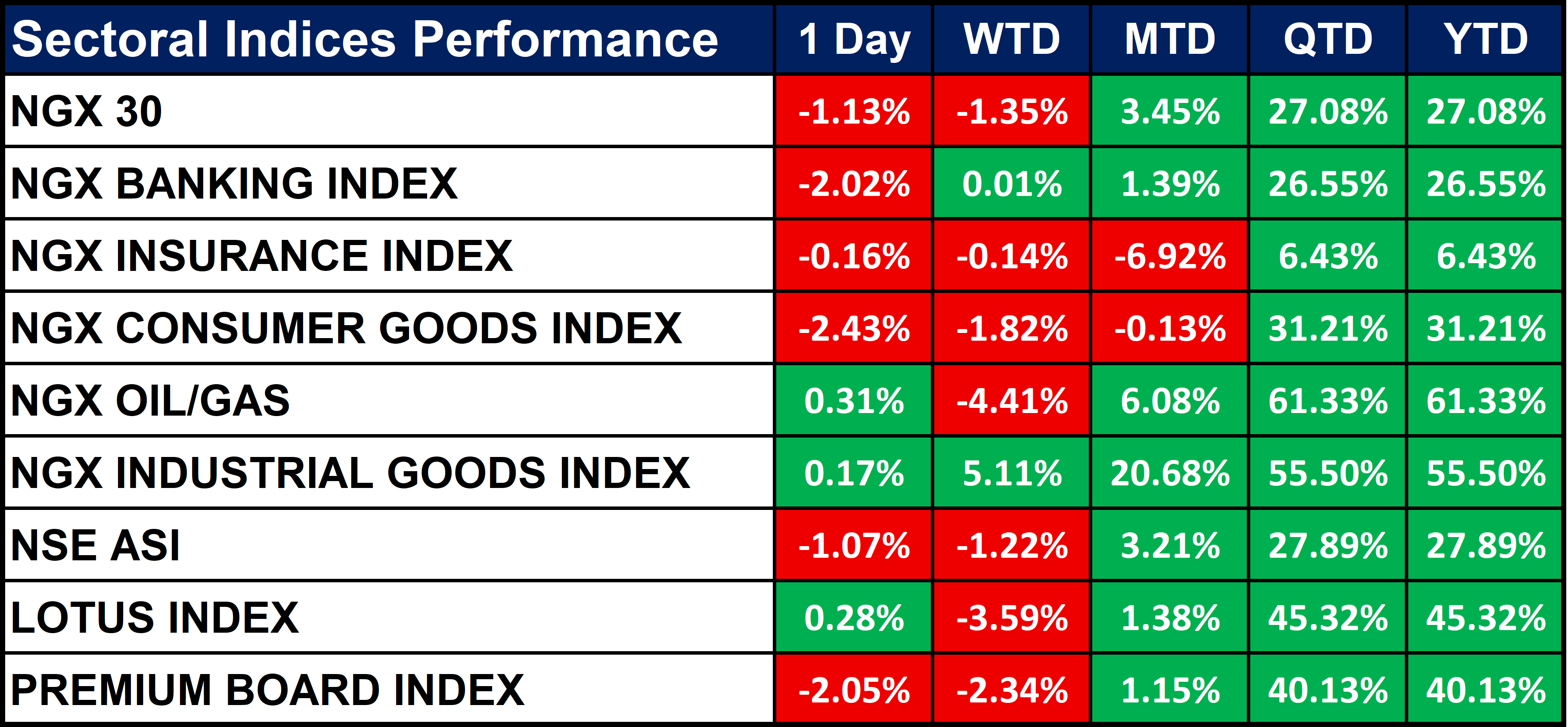

Nigeria Sectoral Indices Performance

The table below shows that the overall market declined, with NGX 30 down 1.13% and key indices like Banking (-2.02%) and Consumer Goods (-2.43%) posting notable losses. Oil/Gas (+0.31%) and Industrial Goods (+0.17%) were the only sectors showing modest gains for the day. Year-to-date, Oil/Gas (61.33%) and Industrial Goods (55.50%) remain the top-performing sectors, while Insurance shows the weakest YTD gain at 6.43%.

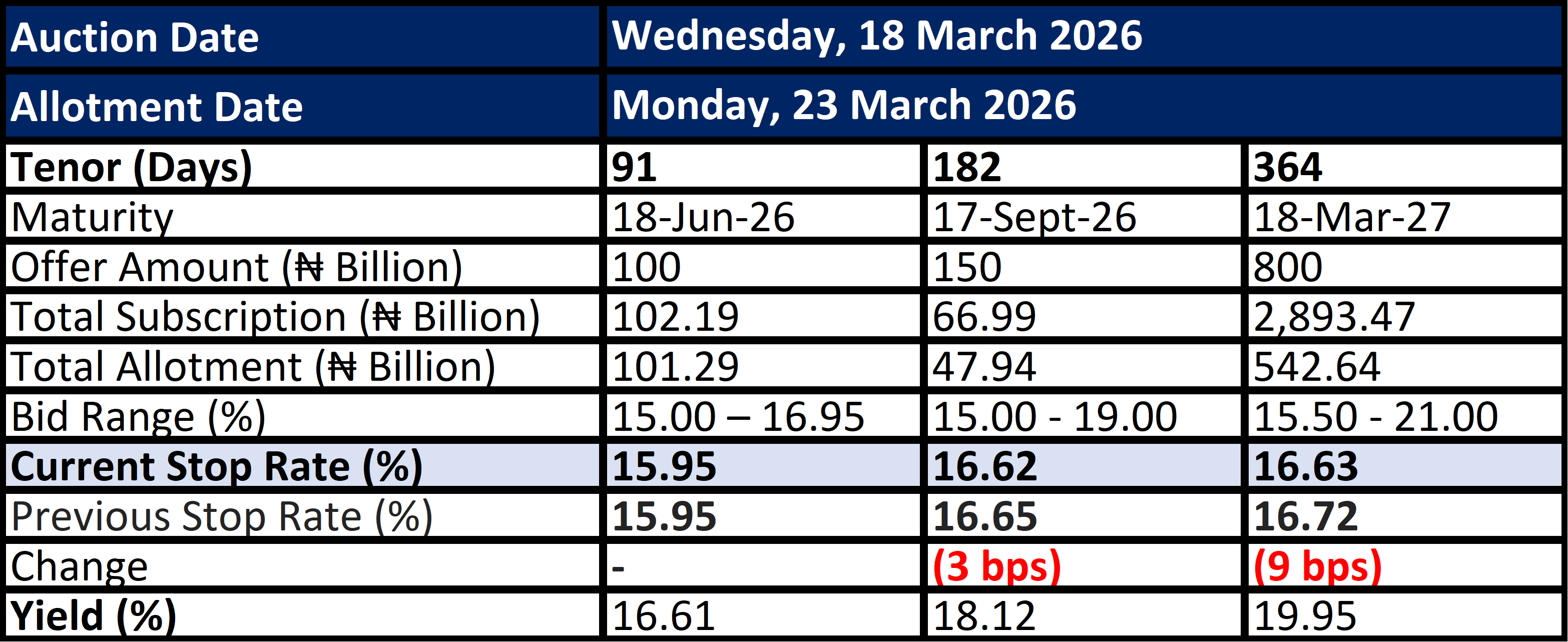

TBills Auction Result

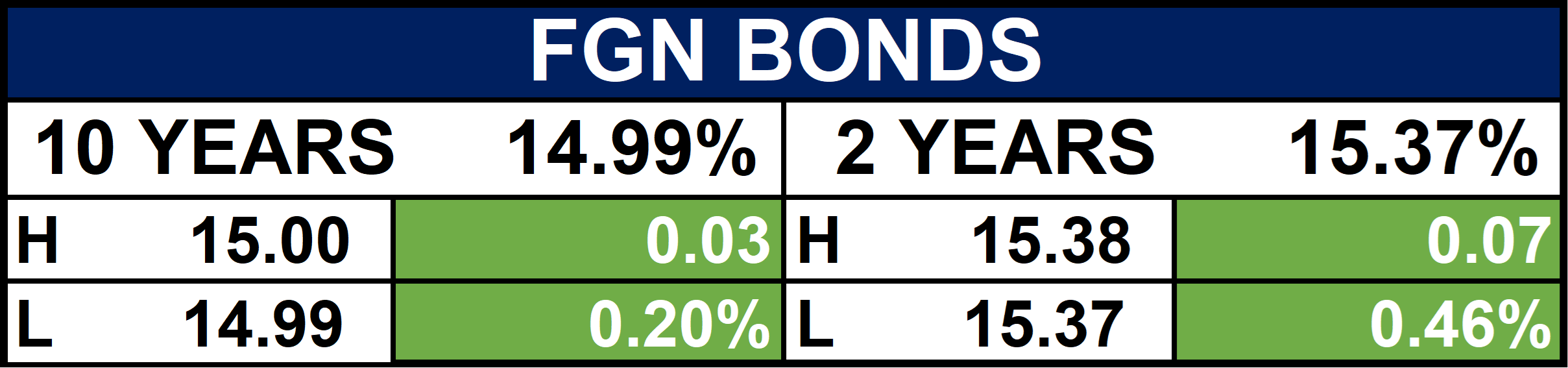

Fixed Income (FGN Bonds)

Global News & Market Update

Russia’s Novatek strikes a preliminary deal on LNG supply to Vietnam:

Novatek signed a preliminary deal to supply LNG to Vietnam, signaling Russia’s shift toward Asian energy markets. - Reuters

Trump says US has ‘major points of agreement’ in talks with Iran:

Donald Trump said the US and Iran have reached major points of agreement in talks, raising prospects of a near-term deal. - Reuters

Saudi Aramco cuts oil supply to Asia for second month in April:

Saudi Aramco cuts crude oil supplies to Asian buyers in April for the second consecutive month due to Strait of Hormuz disruptions. - Reuters

UK’s Starmer calls emergency meeting on economy as Iran war risks mount:

UK Prime Minister Keir Starmer convenes an emergency meeting as the Iran war drives up energy prices and spikes Britain’s government borrowing costs. - Reuters

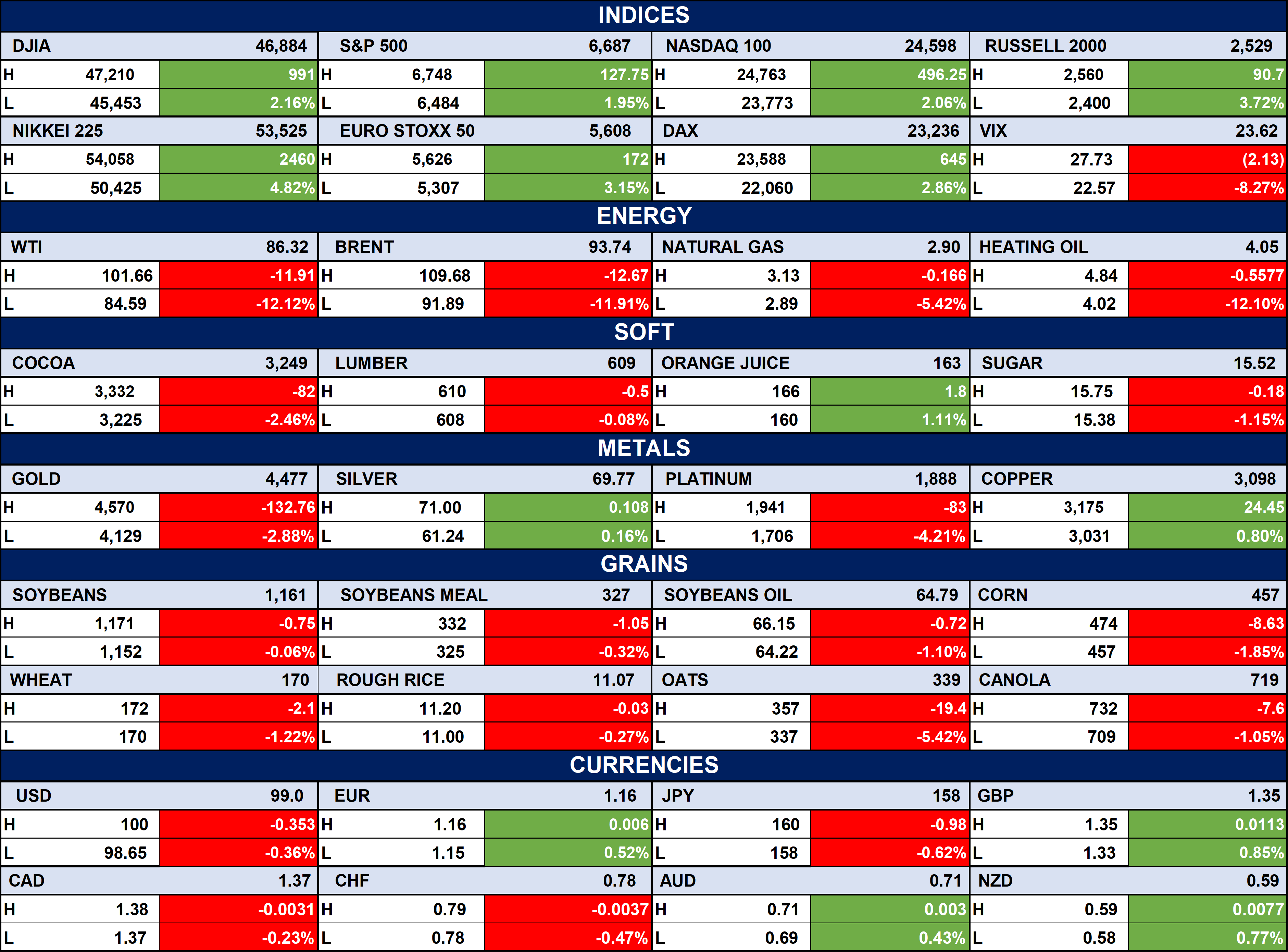

Indices, Commodities & Currencies

The table below depicts that the Global markets show mixed performance, with equities like the S&P 500 Index and NASDAQ 100 holding gains, while volatility remains elevated as seen in the CBOE Volatility Index. Energy prices are under pressure, with WTI Crude Oil and Brent Crude declining sharply, alongside weakness across most agricultural commodities. Meanwhile, metals are mixed gold retreats while copper strengthens and currency markets remain relatively stable with only modest movements across major FX pairs.

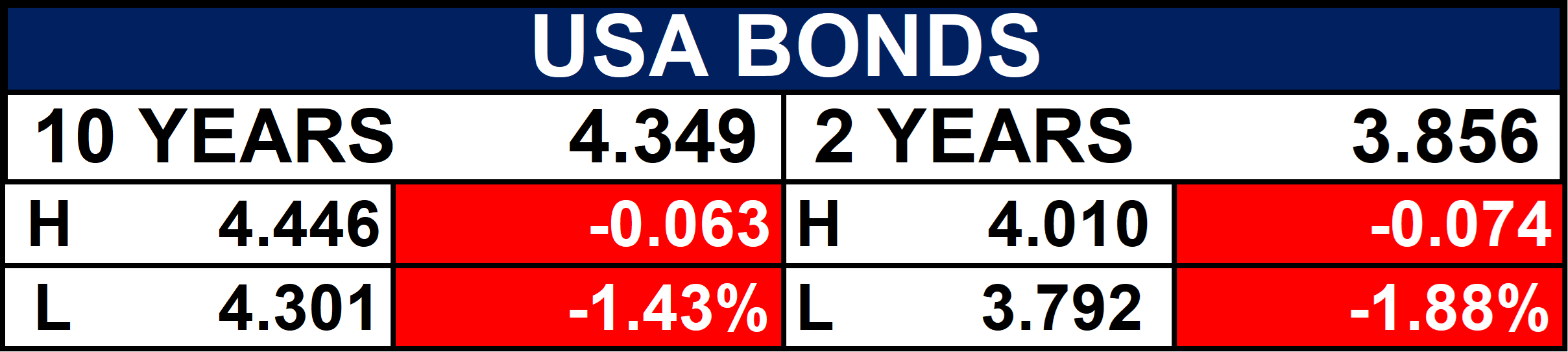

Fixed Income (USA Bonds)

Conclusion

Investors could expect continued sectoral divergence in Nigeria, with Oil/Gas and Industrial Goods leading gains while Banking and Consumer Goods face pressure. Globally, energy price swings and geopolitical developments may drive short-term volatility, presenting opportunities for strategic portfolio adjustments.

Thanks for reading Ranora Consulting! Subscribe for free to receive new posts and support my work.