The Week Ahead: Inflation, Liquidity and Oil Risk Set the Market Tone

Ranora Market Outlook - This week, investors should watch whether stronger reserves and oil prices can offset tighter liquidity, rising inflation pressure and a less forgiving global rates backdrop

Opening View

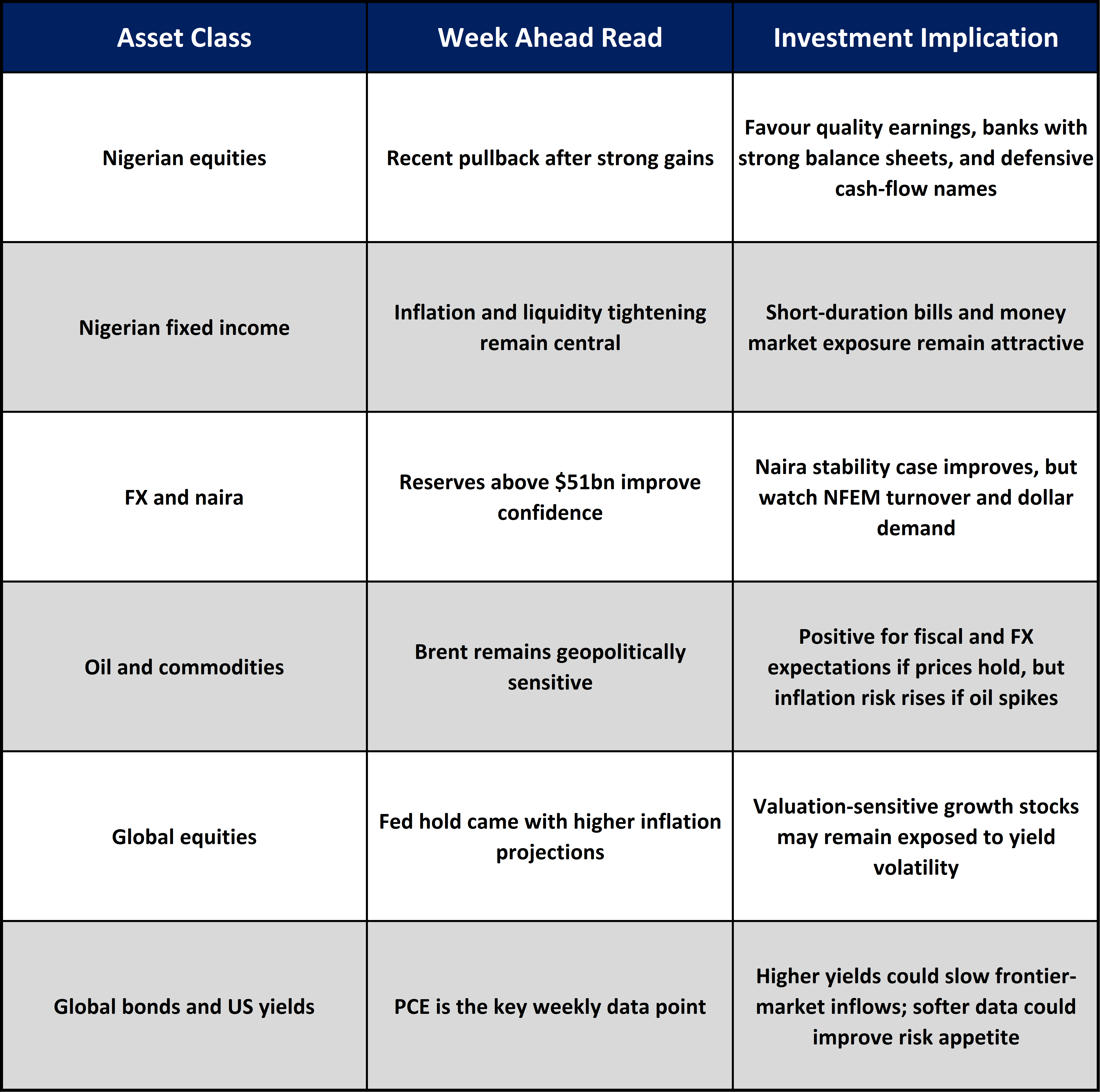

Nigeria enters the week with a stronger external buffer but a more demanding domestic policy setup. External reserves have crossed the $51 billion mark, according to reports citing CBN data, while the official NFEM rate closed around ₦1,371.50/$ on June 19. That reserve build-up gives the CBN more room to smooth FX volatility, but it does not remove the need for tight liquidity management, especially after May inflation rose to 15.93%.

For investors, the key issue is not whether the macro picture has improved. It has in some areas. The more useful question is whether the improvement is strong enough to justify taking more duration, more equity risk, or more naira exposure. At the moment, short-duration fixed income remains well supported by inflation risk and liquidity tightening. Nigerian equities still have structural support from strong nominal earnings, but the recent NGX pullback suggests investors are becoming more selective.

Globally, the Fed’s June hold at 3.50% to 3.75%, alongside higher inflation projections, keeps frontier-market investors focused on US yields, the dollar and oil. For Nigeria, Brent strength helps fiscal and FX expectations, but if oil volatility feeds global inflation and keeps US yields elevated, foreign appetite for risk assets may stay selective.

The Big Picture:

The dominant setup this week is a tug-of-war between improving Nigerian external buffers and tighter financial conditions.

On the positive side, reserves above $51 billion improve the confidence channel for the naira and provide a stronger backstop for FX market management. Q1 2026 GDP growth of 3.89% also shows that the economy is still expanding, supported by services and non-oil activity.

The constraint is inflation and liquidity. May headline inflation rose to 15.93%, food inflation remains a pressure point, and the CBN has kept policy tight. That means the fixed income market is still likely to reward cash discipline and short-tenor positioning more than aggressive duration risk.

Globally, the Fed held rates steady on June 17, but its projections showed higher 2026 inflation and a median federal funds rate of 3.8% by year-end. That matters for Nigeria because higher US yields can reduce appetite for emerging and frontier assets unless local yields, FX stability and policy credibility remain compelling.

Nigeria Market Intelligence

Inflation Is Moving Back Into The Policy Conversation

What happened: Nigeria’s headline inflation rose to 15.93% in May 2026 from 15.69% in April, according to CBN data. Food inflation remains the main risk channel.

Why it matters: This reduces the space for a quick policy pivot. It also keeps real returns under scrutiny, especially for investors holding naira cash, short bills and money market funds.

What to watch: June food prices, fuel-related transport costs, and whether the CBN continues to use liquidity tools aggressively.

FX Reserves Are Now A Stronger Confidence Anchor

What happened: Nigeria’s gross external reserves reportedly rose to about $51.04 billion as of June 19, 2026, with citing CBN data. The official NFEM closing rate was ₦1,371.50/$ on June 19.

Why it matters: Higher reserves can improve confidence in the CBN’s ability to manage FX liquidity. For investors, this supports the case for naira stability, but only if dollar supply remains steady and demand pressures do not re-accelerate.

What to watch: NFEM turnover, reserve movement through month-end, and whether oil receipts or portfolio flows remain supportive.

Fixed Income Still Favours Short Duration

What happened: The CBN conducted a large Treasury bills auction on June 17, reporting a ₦1.00 trillion offer across tenors. The CBN’s government securities page also lists primary market data fields for the June 17 auction.

Why it matters: Large issuance and continued liquidity absorption reinforce the attractiveness of short-tenor yields. Investors extending duration too quickly may face mark-to-market risk if inflation or liquidity pressure keeps yields elevated.

What to watch: Stop rates, subscription levels, OMO activity and whether system liquidity tightens again after recent inflows.

Nigerian Equities Are Entering A More Selective Phase

What happened: The NGX All Share Index pulled back to about 235,941 points on June 19, according to Trading Economics, after a strong year-on-year performance.

Why it matters: The equity market is no longer just a broad liquidity story. Investors may start rotating toward sectors with clearer earnings resilience, dividend visibility and pricing power.

What to watch: Banks, consumer names exposed to input costs, industrials tied to infrastructure and cement demand, and whether foreign participation improves as reserves strengthen.

Global Market Intelligence:

The Fed Has Not Given Risk Assets A Clean Green Light

What happened: The Federal Reserve held the target range for the federal funds rate at 3.50% to 3.75% on June 17. Its projections showed median 2026 PCE inflation at 3.6%, core PCE at 3.3%, and the median federal funds rate at 3.8%.

Why it matters: This keeps US yields relevant for frontier-market flows. If US rates stay higher for longer, Nigerian assets need a convincing mix of yield, FX stability and policy credibility to attract foreign capital.

What to watch: US PCE inflation on June 25, jobless claims and US Treasury yield movement.

Oil Is A Support and A Risk For Nigeria

What happened: Brent has remained sensitive to Middle East developments, with reports showing prices moving around the high-$70s to low-$80s as markets reassess supply risk and diplomatic signals.

Why it matters: Higher Brent can support Nigeria’s export receipts, reserves and fiscal expectations. But if oil strength feeds global inflation, it could also keep US yields higher and reduce global risk appetite.

What to watch: Brent direction, OPEC supply signals, shipping risk around major chokepoints and Nigeria’s actual production levels..

US Inflation Data Is This Week’s Global Trigger

What happened: The BEA’s next PCE price index release is scheduled for June 25. April PCE inflation was 3.8% year-on-year.

Why it matters: A hotter reading could lift US yields and strengthen the dollar, which would pressure emerging and frontier market flows. A softer reading would support risk assets but may not be enough to change the Fed’s posture immediately.

What to watch: Headline PCE, core PCE, personal spending and revisions.

Asset Class Implications:

Ranora View:

Ranora’s view is that this is a week for disciplined positioning, not aggressive risk chasing. Nigeria’s reserve build-up is a meaningful positive because it strengthens the confidence channel around the naira. However, inflation at 15.93%, large bill issuance and active liquidity management mean the domestic rates story is still restrictive.

For naira investors, short-duration fixed income remains a strong core allocation because it offers income while reducing exposure to duration volatility. Equity exposure should be more selective. The market’s recent pullback does not undermine the longer-term earnings story, but it does suggest that investors are becoming less willing to pay for broad market momentum without clear earnings delivery.

For foreign and dollar-aware investors, the main question is whether Nigeria’s improving reserves and policy credibility can offset a global environment where the Fed is still focused on inflation. If US PCE is hot this week, frontier-market risk appetite may weaken. If it is softer, Nigeria could benefit from a better global risk tone, especially if the naira remains stable.

What to Watch Next:

US PCE inflation release on June 25 and its impact on US yields.

NFEM turnover and whether the naira remains stable around recent official levels.

CBN liquidity operations after the large June 17 Treasury bills auction.

Brent crude direction and whether oil volatility supports or complicates Nigeria’s macro outlook.

NGX sector rotation, especially banks, consumer goods, industrials and oil-linked names.

Question of the day:

If Nigeria’s reserves continue rising while inflation remains sticky, should investors prioritize naira fixed income income, equity upside, or dollar liquidity over the next quarter?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.