The Week Ahead: Liquidity, FX Stability, and the Fed Test

Ranora Market Outlook - This week, Nigerian markets face a familiar trade-off: strong local liquidity and equity momentum against tighter monetary conditions, inflation risk, and a pivotal Fed meeting

Opening View

The market setup this week is less about one single event and more about whether investors continue to trust the current Nigerian macro stabilization story. Equities ended last week firmer after the previous week’s sharp correction, but the rally is becoming more selective. The NGX All-Share Index closed around 244,739 points on June 12, with year-to-date gains still above 57%, supported by large-cap buying in telecoms, banking, oil and gas, and insurance names. That is a strong signal, but also a valuation discipline test.

In fixed income, the CBN’s continued liquidity absorption through OMO auctions keeps naira yields relevant for cash-heavy investors. The message from policy remains clear: excess liquidity is still being sterilized, and short-duration instruments remain useful for investors who want income without taking too much duration risk.

Globally, the main event is the June 16-17 Federal Reserve meeting. US inflation is still above target, while oil prices have moved sharply on Middle East de-escalation hopes. For Nigeria, lower Brent would reduce inflation pressure globally but could also soften oil-revenue expectations if the decline is sustained. The naira remains supported by stronger reserves, but FX stability still depends on dollar supply, portfolio confidence, and CBN liquidity management.

The Big Picture:

The dominant market question this week is whether Nigerian assets can hold their recent strength while global risk pricing adjusts around the Fed, oil, and the dollar.

Nigeria’s market has three supports: high naira yields, firmer external reserves, and still-strong equity momentum. But each support has a condition attached. High yields remain attractive only if inflation does not accelerate further. Strong reserves help FX confidence only if dollar liquidity remains visible. Equity momentum can continue only if earnings and sector rotation justify the speed of the year-to-date move.

Globally, the Fed meeting matters because US rate expectations influence frontier-market flows. The Fed’s current target range is 3.50% to 3.75%, and the June meeting includes updated economic projections. If the Fed sounds more hawkish after May US CPI rose 4.2% year-on-year, the dollar and US yields could remain firm, reducing appetite for higher-risk emerging and frontier markets. If the tone is more balanced, Nigerian local-currency assets may benefit from improved risk appetite.

Nigeria Market Intelligence

Nigerian equities: momentum is intact, but leadership is narrowing

What happened: The NGX recovered last week, with the All-Share Index up 0.6% week-on-week despite a softer final session. The index closed at 244,738.74 points on June 12, with market capitalisation around N156.97 trillion. Year-to-date return stood at about 57.27%. The weekly advance was supported by Airtel Africa, First HoldCo, Oando, MTN Nigeria, and GTCO, while consumer goods and industrial goods remained under pressure.

Why it matters: The market is still rewarding liquidity, earnings visibility, and large-cap positioning, but the rotation is becoming more important than the headline index. After such a strong year-to-date rally, investors should be less focused on “the market is up” and more focused on which sectors can still justify fresh capital.

What to watch: Watch whether banks and telecoms continue to absorb flows, whether profit-taking returns in cement and consumer goods, and whether market breadth improves beyond a small number of heavyweight names.

Fixed income: CBN liquidity tightening keeps short-duration yields relevant

What happened: The CBN absorbed N1.689 trillion through a June 8 OMO auction after offering N600 billion across 8-day and 134-day instruments. Demand was concentrated in the longer OMO bill, which attracted about N1.6045 trillion in subscriptions and cleared at a 20.02% stop rate. FMDQ data also showed elevated money-market rates as of June 11, with overnight around 22.16% and open repo around 22.00%.

Why it matters: The CBN is still signalling that liquidity control remains central to inflation and FX management. For investors, this keeps short-duration fixed income attractive because yields remain high without requiring large exposure to long-bond price volatility.

What to watch: Watch OMO auction sizes, stop rates, and whether system liquidity tightens enough to push short-term rates higher.

Inflation: April CPI remains the latest confirmed anchor

What happened: Nigeria’s latest confirmed headline inflation reading is April 2026 at 15.69%, up from 15.38% in March. Food inflation was reported at 16.06% year-on-year. As of this Monday morning, the latest reliable data I found remains the April release; May CPI should be watched closely when published.

Why it matters: The direction matters more than the absolute level. Two consecutive monthly increases would make it harder for the CBN to relax policy conditions and would keep real-yield calculations under pressure. If May inflation surprises higher, it strengthens the case for sustained tight liquidity and supports short-tenor fixed income.

What to watch: Watch food prices, transport costs, energy pass-through, and whether May CPI confirms or interrupts the recent upward drift.

FX and reserves: the naira is supported, but not free of pressure

What happened: CBN NFEM data showed official USD/NGN around N1,363.83 on June 11, while Nigeria’s external reserves were reported above $50 billion in early June. FMDQ money-market rates also remain elevated, supporting the broader policy mix around liquidity and FX stability.

Why it matters: Higher reserves improve the market’s confidence in the CBN’s capacity to manage FX volatility. But reserves alone do not guarantee naira stability. The real test is whether autonomous dollar supply, oil receipts, portfolio inflows, and CBN policy credibility remain aligned.

What to watch: Watch NFEM turnover, reserve accretion, Brent crude direction, and whether the parallel-market premium stays contained.

Oil production: better output helps, but price direction now matters more

What happened: OPEC’s June 2026 Monthly Oil Market Report showed Nigeria’s crude production rising to about 1.53 million barrels per day in May, from about 1.488 million barrels per day in April, based on direct communication data reported by The Guardian.

Why it matters: Improved production supports fiscal revenue, FX supply, and reserve confidence. But if Brent crude keeps falling on reduced geopolitical risk, Nigeria may face a different trade-off: better volume, weaker price. For fiscal planning, the mix of production and realised price matters more than either variable alone.

What to watch: Watch May-to-June production continuity, pipeline losses, export receipts, and Brent’s reaction to the US-Iran de-escalation story.

Global Market Intelligence:

Fed week: the dot plot is the global market anchor

What happened: The Federal Reserve meets on June 16-17, with the meeting tied to a Summary of Economic Projections. The Fed’s current target range remains 3.50% to 3.75%, after the April meeting left rates unchanged.

Why it matters: For Nigerian investors, the Fed affects more than US markets. A hawkish Fed can support the dollar, lift US yields, and reduce foreign appetite for frontier-market risk. A more balanced Fed could support risk assets and ease some external pressure on the naira.

What to watch: Watch the dot plot, inflation language, and whether Fed officials sound more concerned about inflation or growth.

US inflation: still above target, still shaping yields

What happened: US CPI rose 4.2% year-on-year in May 2026, up from 3.8% in April. Core CPI rose 2.9% year-on-year. Energy remained a key pressure point, with the energy index up 23.5% year-on-year.

Why it matters: This keeps the Fed from declaring victory on inflation. For frontier markets, sticky US inflation means the cost of global capital may remain high, and the dollar may stay supported if rate-cut expectations are pushed out.

What to watch: Watch whether the Fed treats the energy-driven inflation rise as temporary or broad enough to justify tighter guidance.

Oil: geopolitical risk premium is being repriced

What happened: Brent crude fell sharply into the mid-$80s area after reports of progress toward a US-Iran peace framework and possible reopening of the Strait of Hormuz. Trading Economics showed Brent near $83.46 on June 15, while recent EIA analysis still warned that oil-market volatility remained elevated and inventories had been drawn down during the disruption.

Why it matters: For Nigeria, lower Brent has two sides. It can reduce imported inflation pressure globally and support risk appetite. But if prices fall too far, Nigeria’s oil revenue assumptions and FX inflow expectations may weaken. The best outcome for Nigeria is not necessarily the highest oil price; it is stable oil prices plus reliable production.

US yields and the dollar: softer today, but not yet a full turn

What happened: The US 10-year yield eased to about 4.43% on June 15, while the DXY dollar index slipped to around 99.4. US equities also opened the week with stronger risk appetite, with the US500 CFD up around 1.25% on June 15.

Why it matters: A softer dollar and lower Treasury yields are usually supportive for emerging and frontier-market flows. But Nigeria’s benefit depends on whether global investors view local yields, FX liquidity, and policy credibility as strong enough to compensate for frontier-market risk.

What to watch: Watch the post-Fed reaction in the US 10-year yield and DXY. Those two indicators will matter for naira sentiment and foreign portfolio appetite.

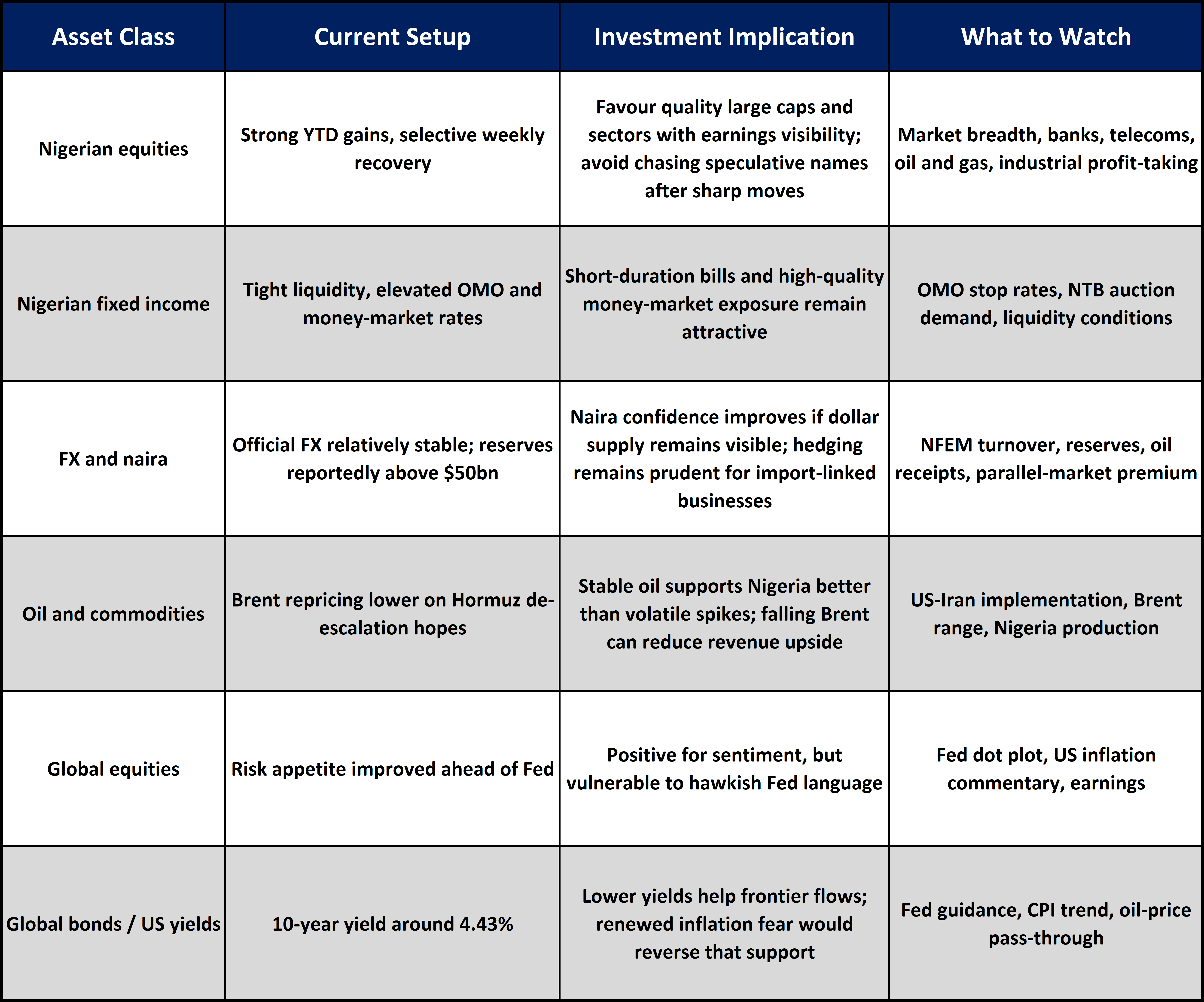

Asset Class Implications:

Ranora View:

This week favours disciplined positioning rather than broad risk-taking. Nigerian equities still have momentum, but the easy part of the rally has likely passed. Investors should focus on companies with earnings resilience, liquidity, and clear sector catalysts rather than buying the index blindly after a 57% year-to-date move.

In fixed income, the stronger signal is still coming from policy. The CBN is actively draining liquidity, and that keeps short-duration naira instruments attractive for investors seeking income and capital preservation. Longer-duration exposure should be selective because inflation has not yet given the market enough comfort.

For FX, the reserve story is supportive, but it should not be read as a guarantee of one-way naira strength. The naira’s next phase depends on dollar supply, confidence, and oil receipts. If Brent falls too quickly, the FX benefit from improved reserves could be tested.

The house view for the week: stay constructive on Nigerian assets,but be selective. Prefer short-duration fixed income, quality equities, and FX-aware portfolio construction. The Fed meeting and oil-price reaction will determine whether global conditions reinforce or challenge Nigeria’s current stabilisation narrative.

What to Watch Next:

The Federal Reserve decision and dot plot on June 17.

Nigeria’s next inflation release, especially food and transport components.

CBN OMO and treasury-bill auction stop rates.

NFEM turnover and whether the official FX market remains orderly.

Brent crude direction after the US-Iran de-escalation headlines.

Question of the day:

If Nigerian equities keep rising while short-term fixed income remains highly attractive, where should investors place fresh capital this quarter: quality stocks, treasury bills, or a balanced allocation?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.