The Week Ahead: Liquidity, Oil and the Naira Set the Tone

Ranora Market Outlook - This week, investors should watch how Nigerian markets absorb tight monetary conditions, stronger reserves, oil volatility, and a global calendar led by US jobs data.

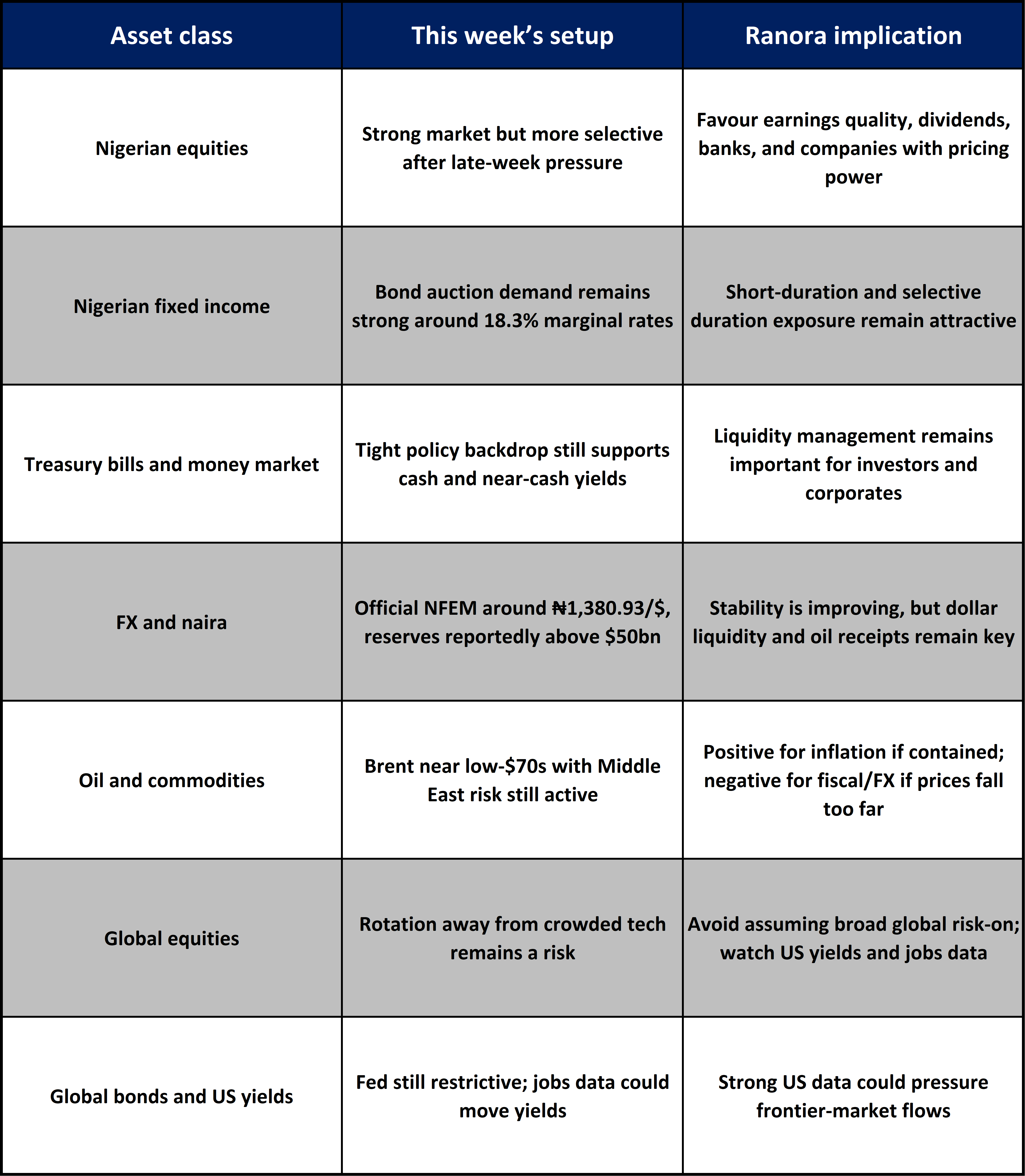

Opening View

Nigerian markets enter the week with three forces shaping positioning: inflation is still rising on a year-on-year basis, fixed income remains supported by high nominal yields, and the naira is being helped by stronger reserves but still exposed to dollar demand and oil-market volatility.

The CBN’s latest published inflation data shows headline inflation at 15.93% in May, up from 15.69% in April, while food inflation also rose to 16.96%. That keeps the policy backdrop tight and reduces the probability of a near-term easing signal. For investors, this means short-duration fixed income should remain attractive, especially where yields compensate for reinvestment and inflation risk.

Equities may remain selective. The market’s broader rally has created valuation discipline: banks, dividend-paying names, and companies with pricing power should attract more attention than speculative growth stories. On FX, the official NFEM rate stood around ₦1,380.93/$ on June 26, while reserves have reportedly moved above the $50 billion mark. That improves confidence, but it does not remove the need to watch liquidity and import demand.

Globally, oil and US rates matter most for Nigeria this week. Brent around the low-$70s reduces immediate imported inflation pressure versus earlier oil spikes, but Middle East risk keeps energy assumptions fragile.

The Big Picture:

The market setup is not bearish, but it is becoming more selective.

In Nigeria, the key issue is whether improving FX reserves and still-high local yields can keep investor confidence intact while inflation remains sticky. The CBN held the MPR at 26.50% at its May meeting, which means liquidity conditions are still being managed from a restrictive policy stance. That supports fixed-income yields and helps anchor the naira, but it also keeps funding costs elevated for corporates.

The June FGN bond auction reinforced investor appetite for duration at the right price. The DMO offered ₦600 billion each across the 2035 and 2037 reopenings, with subscriptions of ₦705.22 billion and ₦708.27 billion respectively. Marginal rates cleared at 18.34% and 18.35%. That tells us there is still strong demand for sovereign paper, but investors are not buying blindly; they are demanding yields that reflect inflation, liquidity, and policy risk.

Globally, the Fed held rates at 3.50% to 3.75% on June 17, while US CPI rose 4.2% year-on-year in May. This keeps US yields and the dollar relevant for frontier-market flows. If this week’s US jobs data is strong, investors may reduce expectations for easier global financial conditions, which could limit appetite for higher-risk emerging and frontier assets.

Nigeria Market Intelligence

Inflation remains the anchor for policy expectations

What happened: Nigeria’s headline inflation rose to 15.93% in May from 15.69% in April. Food inflation rose to 16.96%, according to CBN-published inflation data.

Why it matters: The year-on-year increase keeps pressure on the CBN to maintain tight policy. Even though inflation is far lower than the same period last year, the recent month-to-month direction matters for market expectations.

What it means for investors: Short-duration fixed income remains compelling. Equity investors should favour companies with pricing power, strong cash generation, and limited exposure to expensive borrowing.

What to watch: June inflation expectations, food-price pressure, energy costs, and whether the CBN continues using liquidity tools aggressively

Fixed income demand remains strong, but yield discipline is visible

What happened: At the June 22 FGN bond auction, the DMO allotted ₦600.90 billion on the 2035 reopening and ₦621.00 billion on the 2037 reopening. Marginal rates cleared at 18.34% and 18.35%.

Why it matters: The result shows there is still deep demand for Nigerian sovereign debt, but investors are asking to be paid properly for duration risk.

What it means for investors: The long end may appeal to institutions locking in yield, but for many investors the short and intermediate parts of the curve may offer a cleaner risk-reward balance until inflation direction becomes clearer.

What to watch: Secondary-market yield movement, system liquidity, OMO activity, and whether future auctions continue clearing near current levels.

The naira has support, but liquidity still matters

What happened: CBN’s NFEM page showed the official rate at ₦1,380.9329/$ on June 26. CBN data also indicate external reserves crossed the $50 billion level in June.

Why it matters: Higher reserves improve confidence and give the CBN more room to manage volatility. But the naira still depends on market liquidity, portfolio flows, oil receipts, and corporate dollar demand.

What it means for investors: A more stable naira supports foreign investor confidence and reduces translation pressure for companies with imported inputs. But businesses should not treat recent stability as a guarantee; FX planning still needs buffers.

Nigerian equities need earnings support after strong gains

What happened: The NGX listed its weekly market report for the week ended June 26. Secondary market trackers showed late-week pressure, with the ASI reported around 232,049.02 on June 26 after a daily decline.

Why it matters: After a strong run, the equity market is likely to reward earnings delivery rather than broad optimism. Sector rotation may become more important than index direction.

What it means for investors: Banks, insurance, select consumer names, and dividend-paying stocks may remain in focus. Highly valued names without clear earnings momentum may face more scrutiny.

What to watch: Banking-sector liquidity, recapitalisation updates, H1 earnings guidance, dividend expectations, and foreign participation.

Oil remains a two-sided variable for Nigeria

What happened: Brent crude was reported near $72.57 early on June 29 after renewed US-Iran tensions, while the IEA’s June report warned that oil supply recovery would not be immediate even with an interim agreement.

Why it matters: For Nigeria, oil affects fiscal receipts, reserves, FX supply, and inflation expectations. Lower oil prices can reduce imported energy pressure, but weaker oil revenue can also reduce dollar inflows if sustained.

What it means for investors: Oil volatility should be treated as an FX and fiscal variable, not only an energy-sector story. A stable Brent price with improved Nigerian production would be constructive for reserves and budget expectations.

What to watch: Brent direction, Strait of Hormuz risk, Nigeria’s production levels, and government revenue assumptions.

Global Market Intelligence:

US jobs data is the main global macro event

What happened: The US jobs report is expected on Thursday, July 2, one day earlier than usual because US markets are closed on Friday for the Independence Day holiday.

Why it matters: A strong labour-market print could keep US yields elevated and reduce expectations for Fed easing. That usually makes frontier-market carry less attractive at the margin.

What it means for Nigerian investors: If US yields rise, foreign appetite for naira assets may become more selective. Nigeria will need to keep offering credible real returns and FX stability to compete for capital.

What to watch: Nonfarm payrolls, unemployment rate, wage growth, US 10-year yield reaction, and dollar index movement.

The Fed is still in wait-and-see mode

What happened: The Federal Reserve held the target range for the federal funds rate at 3.50% to 3.75% on June 17.

Why it matters: With US inflation still above target, the Fed is unlikely to rush into easier policy. That keeps global liquidity conditions tighter than many risk assets would prefer.

What it means for investors: Global equities may remain sensitive to rate expectations. For Nigeria, the key risk is that higher US yields could compete with naira fixed-income assets and slow foreign portfolio inflows.

What to watch: Fed communication, US inflation data, jobs numbers, and Treasury yield movement.

US inflation is still above target

What happened: US CPI rose 4.2% year-on-year in May, with core CPI up 2.9%.

Why it matters: Inflation above target keeps policy restrictive and limits the room for aggressive rate cuts.

What it means for Nigerian investors: A strong dollar or higher US yields can reduce risk appetite for emerging and frontier markets. Nigerian assets remain attractive where yield, liquidity, and FX confidence are strong enough to compensate.

What to watch: US jobs data this week and June CPI scheduled for July 14..

Global equities are more fragile beneath the surface

What happened: Major US indices finished last week mixed, with weakness in large-cap technology and AI-related shares weighing on the Nasdaq and S&P 500, while small caps and the Dow performed better.

Why it matters: This suggests investors are rotating rather than simply adding risk. If tech weakness deepens, global sentiment may become less supportive for emerging-market flows.

What it means for Nigerian investors: Local equities may still perform if domestic earnings and liquidity are supportive, but foreign risk appetite could become more selective.

What to watch: Nasdaq direction, AI/technology earnings revisions, US yields, and global fund flows.

Asset Class Implications:

Ranora View:

The main investment message for the week is that Nigerian assets still offer opportunity, but the easy part of the trade is behind us.

For fixed income, yields remain high enough to justify attention, especially at the short end where investors can earn attractive income without taking excessive duration risk. The June bond auction confirms that institutions still want sovereign paper, but the clearing rates also show that investors are pricing risk carefully.

For equities, the market should increasingly separate companies with genuine earnings support from those moving mainly on momentum. Banks remain important because high rates, balance-sheet scale, and recapitalisation themes can support earnings and investor interest. Consumer and industrial names need more selective treatment because funding costs, demand pressure, and input costs still matter.

For FX, stronger reserves are constructive, but not a final victory. The naira’s next test is whether dollar supply remains consistent while demand from importers, corporates, and investors builds into the second half of the year.

The practical stance is clear: stay invested, but be selective. Prioritize yield quality, balance-sheet strength, dividend visibility, and FX resilience.

What to Watch Next:

US nonfarm payrolls on Thursday, July 2, and the reaction in US yields.

CBN liquidity operations and any change in money-market rates.

NFEM turnover, official naira direction, and the parallel-market premium.

NGX sector rotation, especially banks, insurance, consumer goods, and industrials.

Brent crude direction and any renewed disruption around Middle East shipping routes.

Question of the day:

If Nigerian fixed-income yields remain elevated while the naira stabilizes, would you rather increase exposure to short-duration fixed income or selectively add Nigerian equities?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.