The Week Ahead: MPC Week Meets a Hotter Oil Market.

Ranora Market Outlook - Nigeria enters the week with stronger market credibility and firm equity momentum, but rising inflation and higher global yields raise the bar for an easy policy pivot.

Opening View

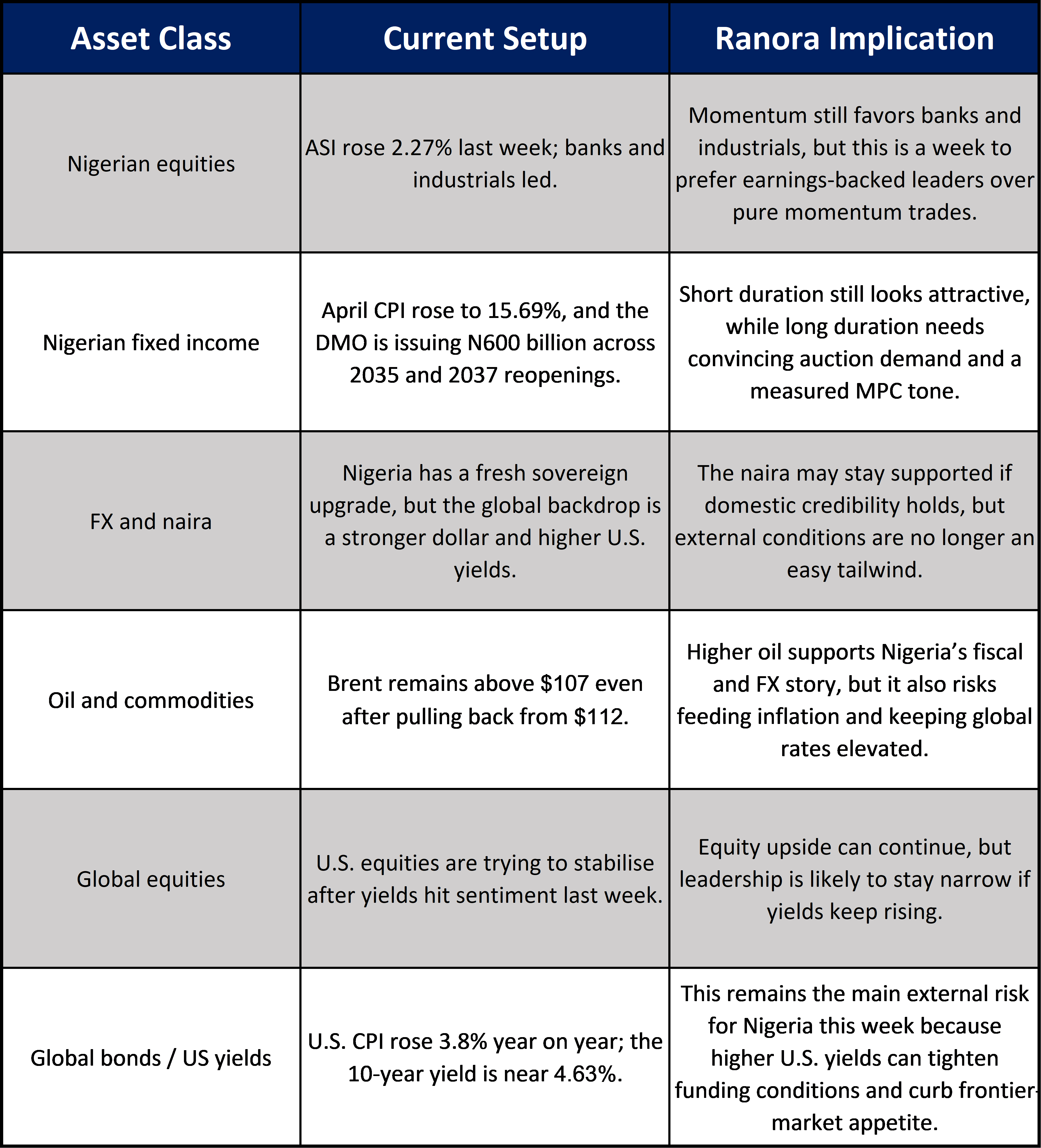

Nigeria starts the week with a better macro narrative than it had a year ago, but the market is no longer trading only on reform optimism. The immediate issue is sequencing. April headline inflation rose to 15.69%, with food inflation at 16.06% and core inflation at 15.86%, just days before the Central Bank of Nigeria’s May 19-20 MPC meeting. That matters because the CBN already cut the MPR by 50 basis points to 26.5% in February, so this meeting arrives with less room for another dovish surprise. At the same time, the domestic risk backdrop is not weak: S&P upgraded Nigeria to B from B- on May 15, citing stronger macro-outcomes, while the NGX All-Share Index closed last week at 250,330.92, up 2.27% week on week and 60.87% year to date.

The complication is global. U.S. April CPI accelerated to 3.8% year on year, oil remains elevated despite intraday volatility, and U.S. 10-year yields are hovering around recent highs near 4.63% as markets reprice inflation and rate expectations. For Nigeria, that combination matters more than the headline noise: it affects imported inflation, frontier-market appetite, dollar liquidity, and how much support the naira can count on if external conditions harden. Our base case for the week is selective risk-taking, not broad risk-on positioning.

The Big Picture:

The domestic story is still constructive, but it is shifting from pure reform relief to execution risk. Nigeria has a stronger sovereign story, a buoyant equity market, and a live fixed income calendar this week, with the DMO offering N300 billion of the 22.60% FGN JAN 2035 and N300 billion of the 16.2499% FGN APR 2037 at auction on May 18. But a firmer oil market and higher global yields mean the CBN now has to weigh inflation control, FX stability, and growth support at the same time. That should keep investors focused on policy tone, auction demand, and whether domestic asset strength can hold up if global duration risk keeps rising.

Five Things That Matter This Week

CBN policy tone.

What is happening: The MPC meets on May 19-20 after cutting the MPR to 26.5% in February. Why it matters: April inflation has moved higher again, so the committee may have less room to emphasize easing. What to watch: whether the CBN treats the latest inflation move as temporary or as a reason to pause.The inflation-fixed income link.

What is happening: Nigeria’s latest CPI print came in at 15.69%, while the DMO is in the market this week with N600 billion of FGN bond supply. Why it matters: a sticky inflation tone can keep demand concentrated in short duration and force investors to demand discipline on clearing yields. What to watch: subscription strength and the signal the bond auction sends about duration appetite.NGX leadership.

What is happening: The NGX ASI gained 2.27% last week, with banking up 2.82% and industrial goods up 4.66%. Why it matters: the market is still rewarding domestic earnings and balance-sheet strength, but a less-friendly rates backdrop could narrow leadership. What to watch: whether banks and industrials continue to carry the tape or whether breadth fades after the strong run.Nigeria’s sovereign credibility.

What is happening: S&P upgraded Nigeria to B from B- and shifted the outlook to stable. Why it matters: that supports the story around sovereign risk, foreign participation, and the relative investability of Nigerian assets, even if it does not eliminate inflation and FX risks. What to watch: whether the upgrade feeds into stronger demand for naira assets rather than just improving sentiment.Oil, U.S. yields, and global risk pricing.

What is happening: Brent fell back to about $107.78 on Monday after touching $112, while U.S. 10-year yields climbed near 4.63% and the dollar stayed near recent highs. Why it matters: for Nigeria, higher oil is revenue-positive, but the combination of firmer energy prices and higher U.S. yields can also tighten global financial conditions and pressure frontier-market flows. What to watch: whether oil stays elevated and whether U.S. yields keep repricing higher after last week’s inflation shock.

Nigeria Watchlist:

MPC decision and guidance on May 19-20. This is the week’s main domestic macro event.

DMO bond auction on May 18 for the reopened 2035 and 2037 FGN lines. Clearing levels will matter for duration sentiment.

NGX breadth after last week’s strong close at 250,330.92, especially in banking and industrials.

April inflation’s second straight uptick, especially the food print at 16.06%.

Whether the S&P upgrade changes actual capital allocation toward Nigerian assets this week.

Global Watchlist:

FOMC minutes on May 20 at 2:00 p.m. Washington time. Markets will look for how seriously the Fed is treating renewed inflation pressure.

Flash PMIs on May 21 across the U.S., eurozone, UK, Japan, and others. These releases should show how growth and pricing pressures are holding up amid the Middle East shock.

U.S. Treasury yields, with the 10-year near recent highs and the 30-year having pushed back above 5% last week.

Brent crude direction after Monday’s reversal from two-week highs.

Dollar strength and broader risk appetite, especially for emerging and frontier markets.

Asset Class Implications:

Ranora View:

This is not a week for broad, indiscriminate risk-taking. Nigeria still has a supportive domestic setup: a stronger sovereign story, firm equity momentum, and policy credibility that is better than it was a year ago. But the April inflation print, this week’s MPC meeting, and the global repricing in oil and U.S. yields mean markets now need confirmation, not just narrative. Our read is that short-duration fixed income remains compelling, banks and industrials still look better placed than weaker cyclical laggards, and naira stability should be treated as conditional on policy discipline and manageable external pressure rather than as a one-way trade.

What to Watch Next:

The CBN MPC decision and post-meeting tone on May 20.

Bond auction results and how investors price the 2035 and 2037 reopenings.

FOMC minutes on May 20.

Flash PMIs on May 21 across major economies.

Whether oil stays above current levels and keeps pressure on global yields.

Engagement Question:

If the CBN pauses while oil and U.S. yields stay elevated, does the better near-term opportunity sit in Nigerian fixed income, large-cap banks, or waiting for a cleaner entry in risk assets?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.