The Week Ahead: Oil Near $80 Puts Nigeria’s Yield Trade Back in Focus

Ranora Market Outlook - This week, investors should watch whether higher oil, U.S. inflation data, and domestic liquidity conditions reinforce demand for short-duration Nigerian assets.

Opening View

The new week opens with a familiar but important tension for Nigerian markets: domestic yields remain high enough to attract defensive capital, but global conditions are becoming less forgiving. Brent crude moved close to $80 per barrel on renewed U.S.-Iran tensions, giving Nigeria a potential fiscal and external-account tailwind if prices hold, but also raising the risk of imported inflation and tighter global financial conditions.

At home, the latest official NBS inflation reading still shows inflation rising to 15.93% in May, with food inflation at 16.96%. That keeps the CBN’s policy stance relevant even after the MPC held the MPR at 26.5% in May. The naira has been broadly steadier than last year’s stressed levels, supported by stronger reserves, but investors should not confuse improved buffers with permanent FX comfort.

The key market question this week is not whether Nigerian assets can still offer yield. They can. The question is whether inflation, oil, and dollar conditions allow investors to keep extending duration and equity risk, or whether cash, treasury bills, and selective defensive equities remain the better risk-adjusted position.

The Big Picture:

Nigeria enters the week with three forces working at once.

First, high domestic rates continue to support the fixed income carry trade. The CBN’s May MPC decision retained the MPR at 26.5%, the CRR for deposit money banks at 45%, and the standing facilities corridor at +50/-450 basis points. That keeps liquidity management tight and preserves the appeal of short-duration instruments for investors who want yield without taking heavy mark-to-market risk.

Second, inflation remains the domestic constraint. NBS data show headline inflation at 15.93% in May, up from April, with food inflation at 16.96%. Until food-price momentum slows more convincingly, the room for aggressive monetary easing remains limited.

Third, the global backdrop has become more oil-sensitive. AP reported that Brent crude rose 4.7% to $79.59 on Monday after renewed U.S.-Iran strikes, while Asian equities weakened and U.S. futures declined. For Nigeria, higher Brent can support oil revenue expectations, but if it strengthens the dollar or U.S. yields, it may also reduce foreign appetite for frontier-market risk.

Nigeria Market Intelligence

Nigerian equities: strong level, thinner margin for error

What happened: The NGX All Share Index closed at 243,954.45 on July 10, with Trading Economics showing a marginal daily decline and a 93.39% year-on-year gain. After such a large annual move, investors should watch whether buying remains broad-based or becomes concentrated in banks, telecoms, and cash-generative defensive names.

Why it matters: A market that has already rerated sharply needs earnings confirmation. Without that, investors may rotate from expensive momentum names into sectors with clearer dividend capacity, FX-linked earnings, or stronger balance sheets.

What to watch: Q2 and half-year corporate reporting dates, especially banks and consumer names where higher funding costs, recapitalisation plans, and household pressure may show up clearly.

Fixed income: short duration still has a strong argument

What happened: With the CBN still holding a tight policy stance, short-tenor fixed income remains attractive for investors who want income and flexibility. The risk is that if inflation surprises higher or liquidity tightens more aggressively, longer bonds may face renewed repricing.

Why it matters: Investors do not need to reach too far on duration when policy rates remain elevated. Treasury bills and short bonds may continue to offer a better balance between carry and liquidity than long-duration exposure.

What to watch: Primary market stop rates, system liquidity, OMO activity, and whether real yields improve after the next inflation print.

FX and reserves: better buffers, but oil and dollar strength still matter

What happened: USD/NGN traded around 1,380.84 on July 13, according to Trading Economics. Separately, CBN data cited by PM News showed external reserves at $51.74 billion as of July 10, up from $49.80 billion at the start of June.

Why it matters: Higher reserves improve the CBN’s capacity to manage FX volatility, but the naira still depends on dollar supply, portfolio flows, oil receipts, and confidence in policy consistency. A stronger dollar or higher U.S. yields could make naira assets work harder to attract foreign capital.

What to watch next: NFEM turnover, reserve movement, parallel-market spread, and whether oil strength translates into visible FX liquidity.

Inflation: food prices remain the real policy test

What happened: The latest official NBS data show headline inflation at 15.93% in May and food inflation at 16.96%. The direction of the next inflation reading matters more than the headline alone: investors should focus on food, core inflation, and month-on-month momentum.

Why it matters: If inflation keeps rising, the CBN has less room to cut rates and bond investors may demand higher term premia. If inflation softens convincingly, demand could move further along the yield curve.

What to watch: The next NBS CPI release, food-price drivers, fuel and transport costs, and imported inflation from oil and FX.

Global Market Intelligence:

U.S. CPI is the week’s main global data point

What happened: The U.S. Bureau of Labor Statistics is scheduled to release June CPI on Tuesday, July 14, 2026. This matters because the Fed’s June minutes show policymakers held the federal funds target range at 3.50%-3.75%, but several participants saw scenarios where policy firming could be warranted if inflation remains elevated.

What it means for Nigerian investors:

Higher U.S. inflation could lift U.S. yields and strengthen the dollar. That would raise the hurdle rate for Nigerian assets and may keep foreign investors selective despite high local yields.

Oil is now both a support and a risk

What happened: Brent near $80 can improve Nigeria’s oil revenue expectations if production and export receipts hold up. But a geopolitically driven oil rally can also raise fuel, freight, and inflation risks globally.

Why it matters: Oil strength is not automatically bullish for Nigerian markets. It is bullish only if it improves dollar supply and fiscal receipts faster than it worsens inflation expectations and global risk appetite.

The dollar and U.S. yields remain the pressure points

What happened: The Fed minutes show policymakers are divided between inflation eventually easing and scenarios requiring further firming. Trading Economics showed the Dollar Index around 101.107 on July 13, up on the session.

Why it matters: A firmer dollar can pressure emerging and frontier currencies. For Nigeria, that means the naira’s recent stability still needs reserve support, oil inflows, and credible monetary policy.

Global equities face an earnings and valuation test

What happened: U.S. equities ended the prior week higher, with AP reporting the S&P 500 up 1.2% for the week and Nasdaq up 1.7%. The problem for investors is that higher oil and sticky inflation can quickly change the discount-rate argument behind expensive growth stocks.

Why it matters: If global risk appetite weakens, frontier flows may slow. Nigerian equities with strong earnings visibility may still attract local demand, but broad foreign participation would likely become more selective.

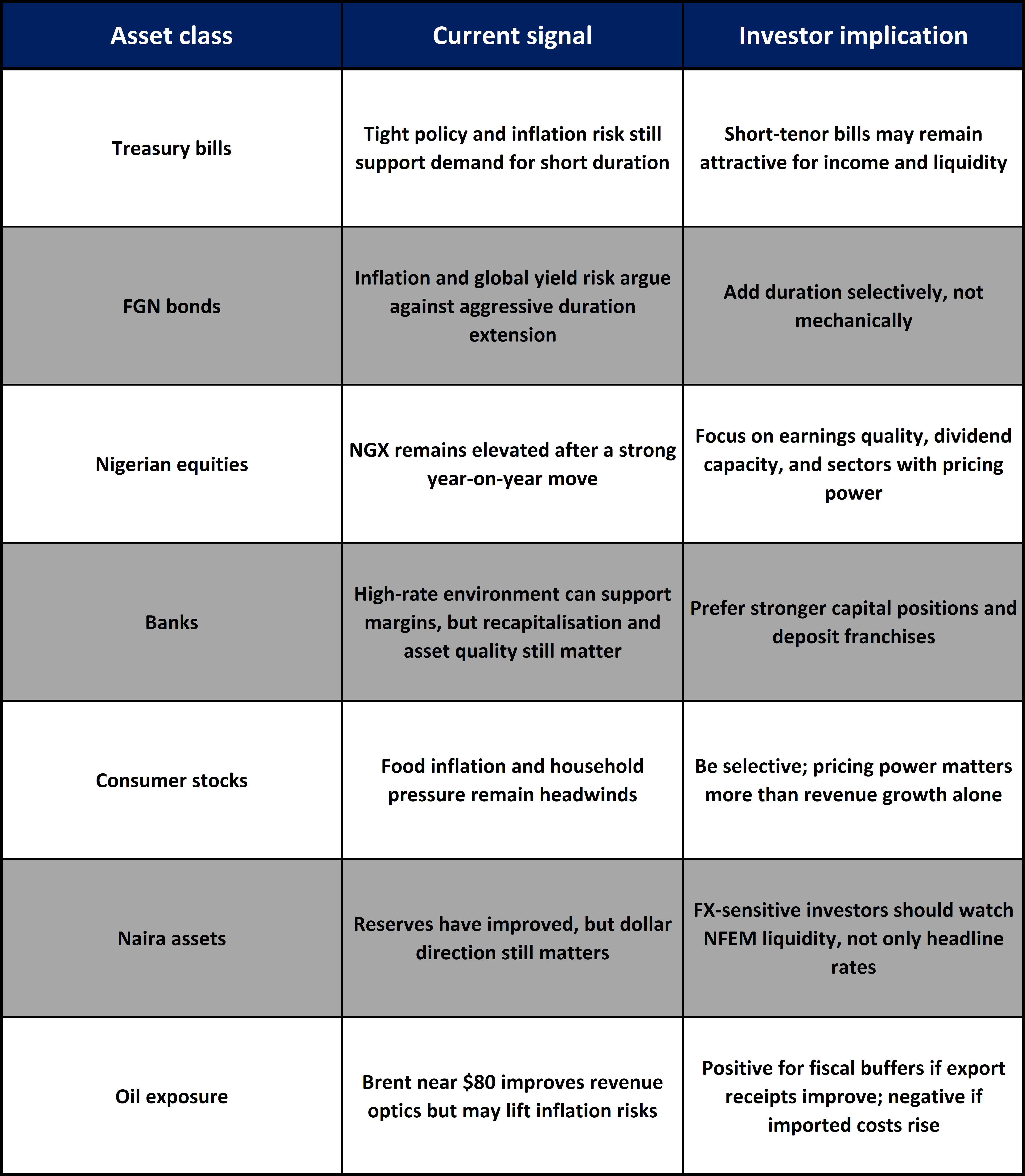

Asset Class Implications:

Ranora View:

The most important investment implication this week is that Nigerian investors are being paid to be selective.

Equities still have a role, especially in sectors with strong cash flow, pricing power, and balance-sheet resilience. But after the market’s earlier strength and recent correction, the easy broad-market trade is less compelling. Investors should be asking whether each equity position can justify its valuation through earnings, dividends, or structural growth.

Fixed income deserves serious attention. If Treasury bill issuance stays heavy and policy remains tight, short-duration instruments can offer attractive carry without forcing investors too far out on the curve. That does not mean avoiding equities. It means the hurdle rate for equity exposure is now higher.

For businesses, the key watchpoint is FX. A stable naira supports planning and margin visibility. A weaker oil backdrop, however, can quickly make FX liquidity the market’s main concern again.

What to Watch Next:

U.S. June CPI on Tuesday, July 14, and what it does to Fed rate expectations.

Brent crude’s reaction to U.S.-Iran tensions and whether prices remain near $80.

Nigeria’s next inflation update, especially food and month-on-month momentum.

CBN liquidity actions, treasury bill stop rates, and demand at primary auctions.

NGX Q2 and half-year earnings calendar, especially banks and consumer companies.

Question of the day:

If inflation remains sticky but the naira stays relatively stable, would you rather extend duration in Nigerian bonds or keep building short-term treasury bill exposure?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.