The Week Ahead: Rates, Reserves and Risk Appetite Face a Jobs-Tested Week

Ranora Market Outlook - Nigeria enters June with stronger growth data, elevated yields, firmer reserves and a still-powerful equity rally, while global markets look to US jobs and oil risk.

Opening View

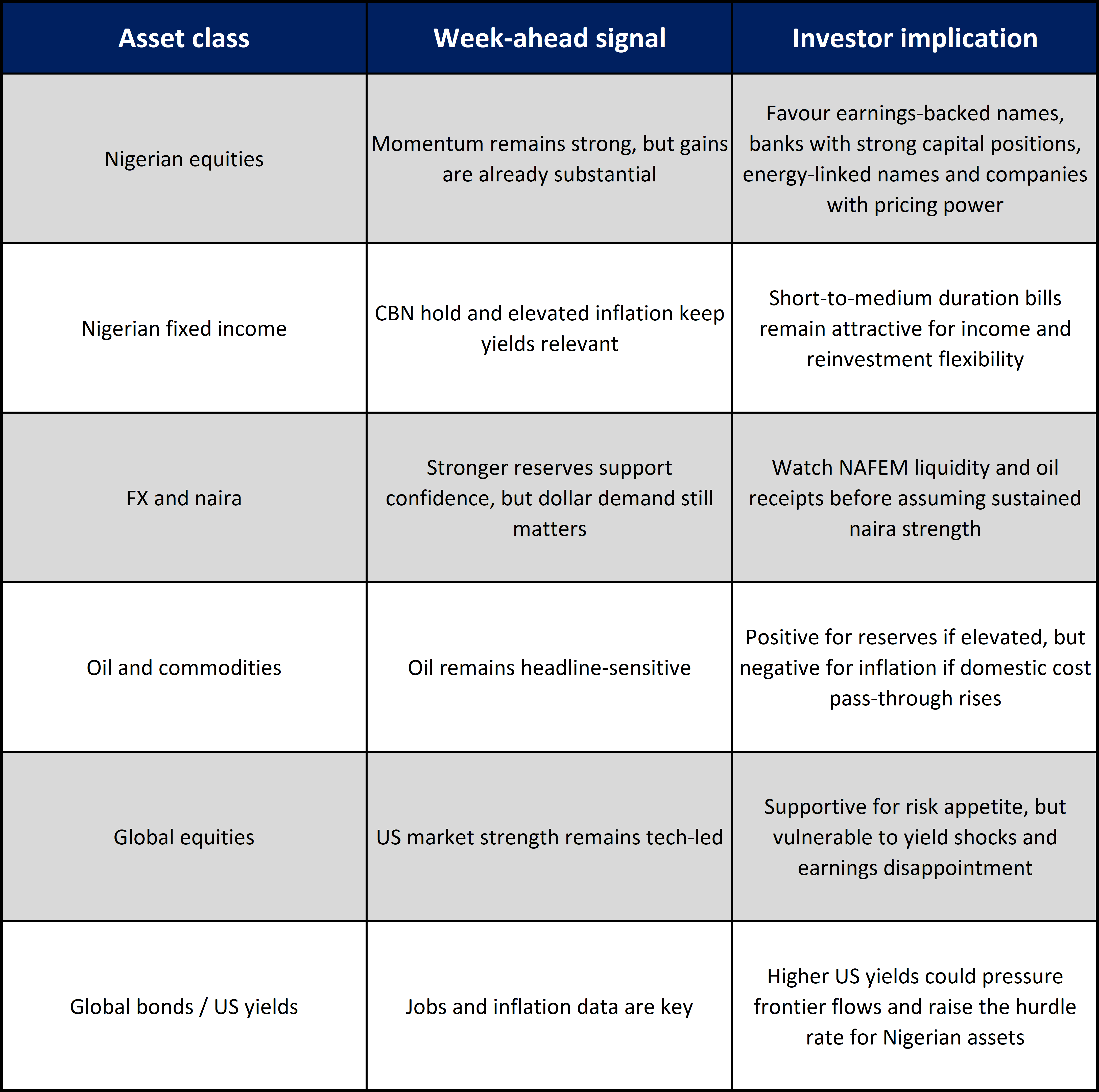

This week starts with Nigerian markets balancing three forces: growth resilience, tight money and external liquidity support. Q1 2026 GDP growth of 3.89% confirms that the economy is still expanding at a respectable pace, helped by services, agriculture and non-oil activity. But April inflation rising to 15.69% and the CBN’s decision to hold the MPR at 26.5% show that the policy room for aggressive easing remains limited. For investors, this keeps the fixed income market relevant, especially where treasury bill yields still compensate for inflation and liquidity risk.

Equities remain the more interesting valuation question. The NGX All-Share Index closed around 250,385 points after a modest weekly gain, with year-to-date returns above 60%, according to recent market reports. That is strong momentum, but it also raises the bar for earnings delivery and sector selection. Banks, energy-linked names and companies with pricing power remain better positioned than weaker consumer-facing businesses exposed to still-high input costs.

Globally, the key test is whether US labour data supports or challenges the market’s optimism. US equities are at record highs, yet April PCE inflation remains above the Fed’s target. For Nigeria, the link is direct: US rates, oil prices and dollar sentiment will affect foreign portfolio appetite, naira stability and domestic yield expectations.

The Big Picture:

Nigeria’s near-term market setup is not weak, but it is tight. Growth is holding up, reserves are stronger, and equities are still attracting capital. The constraint is inflation. The CBN’s May hold at 26.5% suggests policymakers are not ready to restart easing while inflation has risen for two consecutive months.

That matters because the market is now pricing a more complicated balance. Lower rates would support equities and reduce sovereign funding costs, but premature easing could weaken real returns and pressure the naira if global dollar conditions tighten. The practical implication is that Nigerian assets may continue to reward selectivity rather than broad risk-taking.

Globally, investors are entering the week with US stocks near records, oil markets still shaped by OPEC+ supply decisions and Middle East disruption risk, and the Federal Reserve on hold at a 3.50% to 3.75% target range. The US May jobs report due Friday is the main macro event. A stronger labour print could keep US yields firm and reduce foreign appetite for frontier market risk; a softer print could support risk assets and give emerging-market currencies some breathing room.

Nigeria Market Intelligence

CBN holds rates, keeping the yield floor high

What happened: The CBN retained the Monetary Policy Rate at 26.5% at its May 19-20 MPC meeting, alongside other key parameters including CRR and liquidity ratio settings.

Why it matters: The hold confirms that the February rate cut has not become a fast easing cycle. With inflation edging higher, the CBN appears focused on protecting price stability and naira confidence.

What to watch: Watch whether treasury bill stop rates remain attractive enough to hold domestic liquidity, especially if inflation rises again in May..Inflation complicates the easing story

What happened: Nigeria’s headline inflation rose to 15.69% in April 2026 from 15.38% in March, while month-on-month inflation slowed to 2.13% from 4.18%.

Why it matters: The annual rate is moving in the wrong direction, but the slower monthly pace gives the CBN some reason to avoid tightening further. For investors, this supports a “carry still matters” approach in short-to-medium duration fixed income.

What to watch: May CPI will determine whether April was a temporary bump or the start of renewed price pressure. Food and energy components matter most.GDP growth supports the equity story, but not all sectors equally

What happened: Nigeria’s economy grew 3.89% year-on-year in Q1 2026, above the 3.13% recorded in Q1 2025. Services remained the largest contributor, while agriculture and industry also expanded.

Why it matters: Growth resilience supports earnings expectations, but investors should separate broad GDP improvement from company-level profitability. Firms with pricing power, strong balance sheets and FX discipline should benefit more than volume-dependent businesses.

What to watch: Q2 corporate earnings and management commentary on margins, input costs and consumer demand.NGX momentum remains powerful but valuation discipline matters

What happened: The NGX All-Share Index closed around 250,385.47 points, with market capitalisation near N160.51 trillion and year-to-date return around 60.9%, based on recent market reports.

Why it matters: Strong equity momentum can attract more domestic and foreign interest, but it also increases the risk of crowding in high-performing sectors. Investors should focus on earnings visibility rather than simply chasing index strength.

What to watch: Banking, oil and gas, industrials and consumer goods rotation; also watch whether market breadth improves or gains remain concentrated.Reserves provide support for FX confidence

What happened: Nigeria’s gross external reserves were reported around $49.49 billion as of May 15 and around $49.34 billion as of May 26, according to reports citing CBN data.

Why it matters: Stronger reserves improve confidence in the FX market and increase the CBN’s ability to manage liquidity shocks. This is constructive for foreign portfolio investors, but it does not remove naira risk if oil prices reverse or dollar demand rises.

What to watch: NAFEM turnover, reserve trend, oil receipts and portfolio inflow behaviour.

Global Market Intelligence:

US jobs data is the week’s main global risk event

What happened: The US Employment Situation report for May 2026 is scheduled for Friday, June 5.

Why it matters: US labour data will shape expectations for the Fed’s next move. Strong jobs data could keep US yields elevated and pressure emerging and frontier market flows. Softer data may support risk appetite and ease some pressure on dollar-sensitive assets.

What to watch: Payroll growth, unemployment rate, wage growth and revisions to previous months.US inflation remains above target

What happened: The BEA reported April PCE inflation at 3.8% year-on-year, with core PCE at 3.3%.

Why it matters: The Fed is unlikely to turn meaningfully dovish while inflation remains above target. For Nigeria, this matters because high US real and nominal yields can compete with naira assets and reduce the appeal of frontier-market risk.

What to watch: Whether energy prices keep feeding into US inflation and whether Fed communication turns more hawkish before the June 17 FOMC decision.US equities are strong, but leadership is narrow

What happened: The S&P 500 closed at 7,580.06 on May 29, with the index recording a ninth straight weekly gain. The Nasdaq also advanced, supported by technology and AI-related optimism.

Why it matters: A strong US equity market supports global risk appetite, but narrow tech-led leadership can become fragile if yields rise or earnings disappoint.

What to watch: Whether the rally broadens beyond technology and how markets react to jobs data.Oil remains a Nigerian fiscal and FX swing factor

What happened: OPEC said Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria and Oman agreed to a 188,000 barrels-per-day production adjustment for June 2026, with another meeting scheduled for June 7. Oil markets remain sensitive to Middle East supply disruption risk.

Why it matters: Higher Brent prices can support Nigeria’s export receipts and reserves, but they can also raise domestic energy and logistics costs if pass-through intensifies. For investors, oil is currently both a revenue support and an inflation risk.

Asset Class Implications:

Ranora View:

Ranora’s view is that this is a week for disciplined positioning, not broad risk expansion. Nigeria’s macro picture is improving in important areas: output growth is firmer, reserves are stronger, and market confidence remains visible in equities. But inflation has not been defeated, and the CBN’s decision to hold rates at 26.5% confirms that monetary policy is still in a defensive phase.

For investors, the cleanest opportunity remains in balancing income with select equity exposure. Treasury bills and high-quality short-duration fixed income still offer useful carry while policy remains tight. Equities still deserve attention, but the market’s strong year-to-date performance means stock selection matters more than index direction. The best-positioned companies are those that can protect margins, benefit from financial deepening, or convert macro reform into earnings growth.

The key risk is external. If US jobs data keeps yields high and oil volatility persists, foreign appetite for frontier-market risk could become more selective. That would make naira liquidity, reserves and domestic investor demand even more important for Nigerian market direction.

What to Watch Next:

US May payrolls report on Friday, June 5, and its effect on US yields and dollar sentiment.

Nigeria’s next inflation print, especially food inflation and month-on-month pressure.

OPEC+ meeting on June 7 and the direction of Brent crude.

NGX market breadth after the strong year-to-date rally.

Naira liquidity and reserve movement through early June.

Question of the day:

If Nigerian yields remain elevated while equities continue to rally, where should investors place the next marginal naira: income, growth, or liquidity?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.