The Week Ahead: Rates, Rotation, and the Naira Stability Test

Ranora Market Outlook - This week, investors should watch whether Nigeria’s equity pullback becomes healthy rotation, while global markets reprice U.S. inflation and Fed risk.

Opening View

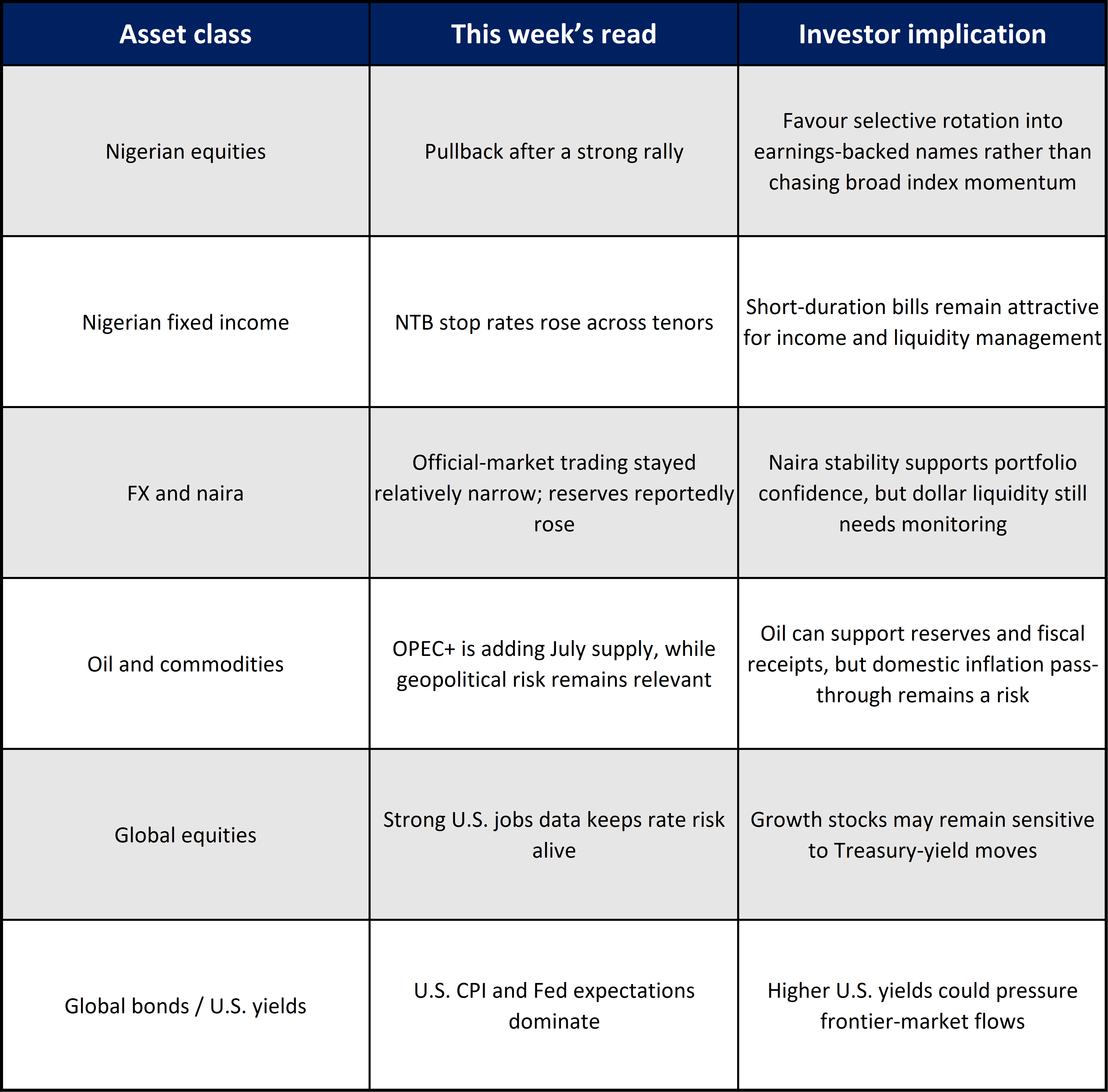

Nigeria enters the week with a more balanced market setup than the headline equity decline suggests. The NGX All-Share Index fell 3.11% last week to 242,593.31 points after a powerful rally, but turnover stayed strong, which points less to market abandonment and more to profit-taking after stretched gains. The key question is whether capital rotates into fundamentally stronger banks, cash-generative consumer names, and dividend-paying defensives, or whether the correction becomes broader.

Fixed income remains difficult to ignore. The June 3 NTB auction cleared at higher stop rates across tenors, with the 364-day bill at 16.35%, reinforcing the case for short-duration yield while inflation is still above comfort levels. FX is also central: the naira traded in a relatively narrow official-market range last week, while reserves reportedly rose to about $50.04 billion by June 4.

Globally, the U.S. jobs report has reduced the urgency for Fed easing, and Wednesday’s U.S. CPI release may determine whether Treasury yields and the dollar add pressure to emerging and frontier market flows. For Nigeria, the most important link is clear: stable reserves, attractive yields, and credible FX liquidity remain essential for foreign portfolio appetite.

The Big Picture:

The market setup is no longer simply “risk-on Nigeria.” It is becoming more selective.

Nigerian equities are still sitting on strong year-to-date gains, but last week’s pullback shows that valuation discipline is returning. That matters because the next leg of the market will likely be led by earnings quality, liquidity, dividend visibility, and sector-specific catalysts rather than broad index momentum.

In fixed income, the CBN’s continued liquidity absorption and higher NTB stop rates keep short-duration paper relevant for investors who want income without taking excessive duration risk. The May MPC decision to hold the MPR at 26.5%, alongside a 45% CRR for commercial banks, reinforces that monetary conditions remain tight even after earlier easing hopes.

Globally, the stronger U.S. jobs print and the upcoming U.S. CPI report keep the dollar and U.S. yields at the centre of frontier-market risk. If U.S. inflation surprises higher, global capital may demand more compensation for risk, which could reduce appetite for naira assets unless domestic yields and FX liquidity remain compelling.

Nigeria Market Intelligence

Nigerian equities: profit-taking, not yet a broken trend

What happened: The NGX All-Share Index declined 3.11% last week to 242,593.31 points, with market capitalisation down to N155.59 trillion. The fall followed strong earlier gains, including an all-time high in May. Trading activity remained robust, with turnover rising to 3.97 billion shares valued at N175.66 billion.

Why it matters: The correction may be healthy if it removes excess from high-flying names and allows investors to rotate toward companies with stronger earnings visibility. Banks remain important because high rates can support asset yields, but investors should watch funding costs, impairments, and recapitalisation execution.

What to watch: Watch whether banking, industrials, and oil and gas counters stabilise after last week’s selling. A rebound with narrow breadth would suggest tactical buying; broader participation would suggest renewed institutional confidence.

Fixed income: short-duration yield remains attractive

What happened: At the June 3 NTB auction, the CBN raised N1.457 trillion against N2.160 trillion in subscriptions. Stop rates rose to 16.05% for 91-day bills, 16.19% for 182-day bills, and 16.35% for 364-day bills.

Why it matters: This keeps short-duration fixed income attractive for investors seeking income while avoiding long-duration mark-to-market volatility. It also shows the authorities are still actively managing liquidity, especially with large OMO maturities and banking-system liquidity flows expected in June.

What to watch: Watch stop rates at the next primary market auction, secondary-market yield movement, and whether liquidity conditions force banks and fund managers to bid more aggressively.

FX and reserves: naira stability is still the main confidence anchor

What happened: The naira reportedly closed around N1,365/$ in the official market on Friday after trading in a narrow range during the week. External reserves were reported to have risen from $49.80 billion at the start of the week to about $50.04 billion by June 4.

Why it matters: FX stability matters more than the exact daily rate. If the naira remains relatively stable while reserves rise, foreign investors have a stronger case for naira fixed income and equities. For businesses, a steadier FX market improves pricing, import planning, and working-capital decisions.

What to watch: Watch official FX turnover, reserve movement, oil receipts, and whether dollar liquidity remains strong enough to prevent renewed pressure from importers and portfolio outflows.

Inflation and monetary policy: the easing story is not automatic

What happened: Nigeria’s April headline inflation rose to 15.69% from 15.38% in March, while food inflation stood at 16.06%. In May, the CBN MPC retained the MPR at 26.5%, with the commercial-bank CRR at 45%.

Why it matters: Inflation is lower than 2025 levels but still high enough to make aggressive policy easing difficult. This supports a higher-for-longer domestic yield environment and may keep money market instruments competitive against equities.

What to watch: Watch May inflation data, food-price trends, and whether the CBN prioritises disinflation and FX stability over faster rate cuts.

Growth: Nigeria’s non-oil economy remains the key earnings driver

What happened: NBS reported that real GDP grew 3.89% year-on-year in Q1 2026, above the 3.13% recorded in Q1 2025. The non-oil sector contributed 96.08% of real GDP, while the oil sector grew 2.57%.

Why it matters: For equities, this keeps attention on banks, telecoms, consumer staples, trade, manufacturing, and services rather than only oil-linked revenue. For policy, it suggests growth is holding up, but the quality of growth still depends on inflation, credit conditions, and household purchasing power.

What to watch:Watch whether corporate earnings confirm the GDP story, especially in banks, telecoms, consumer goods, cement, and industrial names.

Global Market Intelligence:

U.S. jobs reset the Fed conversation

What happened: U.S. nonfarm payrolls rose by 172,000 in May, while unemployment held at 4.3%.

Why it matters: A stronger labour market reduces pressure on the Fed to ease quickly. For Nigeria, that matters because higher U.S. yields and a firmer dollar can reduce appetite for frontier-market risk unless domestic yields remain sufficiently attractive.

What to watch: Watch U.S. Treasury yields, the dollar index, and how markets price the June 16-17 FOMC meeting.

U.S. CPI is this week’s global macro trigger

What happened: The May U.S. CPI report is scheduled for Wednesday, 10 June 2026.

Why it matters: A higher inflation print could push yields upward and strengthen the dollar. That would matter for Nigeria through portfolio flows, FX expectations, and the risk premium demanded on naira assets.

What to watch: Watch core CPI, energy-price pass-through, and the bond-market reaction immediately after the release.

Fed meeting risk is moving closer

What happened: The Federal Reserve’s next FOMC meeting is scheduled for 16-17 June 2026, with Summary of Economic Projections attached.

Why it matters: The dot plot and tone of the Fed communication may matter as much as the rate decision. If the Fed signals tighter-for-longer policy, global liquidity conditions may become less supportive for emerging and frontier markets.

What to watch: Watch whether the Fed acknowledges stronger labour data as an inflation risk, and whether markets price higher real yields.

Oil remains a two-sided Nigeria story

What happened: OPEC said Saudi Arabia, Russia, Iraq, Kuwait, Kazakhstan, Algeria, and Oman agreed on 7 June to implement a 188,000 barrels-per-day production adjustment in July.

Why it matters: For Nigeria, higher oil prices can support fiscal revenue expectations and reserves, but they can also complicate inflation through fuel and logistics costs. The investment implication is that oil strength is positive for external buffers only if production, exports, and domestic pass-through are managed well.

What to watch: Watch Brent crude, OPEC+ compliance, Middle East supply risk, and Nigeria’s own production/export performance.

Asset Class Implications:

Ranora View:

This week is less about whether Nigerian assets are attractive and more about which assets are being paid enough for their risk.

Our view is that short-duration naira fixed income remains compelling while inflation is still sticky and the CBN is actively absorbing liquidity. In equities, the recent correction should improve entry discipline, but investors should avoid treating every dip as an automatic buying opportunity. The better approach is to prioritise companies with pricing power, strong balance sheets, visible dividend capacity, and exposure to sectors that can withstand high funding costs.

The naira remains the most important market signal. If reserves stay firm and official-market liquidity remains orderly, Nigeria can continue to attract portfolio interest into both bills and selected equities. If U.S. CPI or Fed messaging pushes global yields higher, Nigeria may need to preserve a sufficient yield premium to keep foreign appetite intact.

What to Watch Next:

U.S. CPI on Wednesday, 10 June, and its effect on U.S. yields and the dollar.

Official FX turnover and whether the naira holds near last week’s range.

Next NTB and OMO activity, especially whether stop rates continue to rise.

NGX market breadth after last week’s correction.

Brent crude, OPEC+ supply execution, and Nigeria’s reserve trajectory.

Question of the day:

If Nigerian equities pull back further while Treasury bill yields remain elevated, would you rather add selectively to equities or lock in short-duration fixed-income returns?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.