The Week Ahead: The Yield Question Driving Nigerian Assets This Week

Ranora Market Outlook - Nigeria enters the week with equities trying to stabilize, Treasury supply rising, the naira holding near recent official levels, and global investors reassessing oil and Fed

Opening View

This week begins with Nigerian markets facing a familiar but important tension: equities still offer earnings and inflation-hedge appeal, but fixed income is again becoming harder to ignore as Treasury bill supply rises and money-market rates remain elevated.

The NGX All-Share Index closed at 229,240.34 on Friday, July 3, up 2.19% on the day but still down over the past month, according to Trading Economics. That combination matters. It suggests investors are not abandoning equities, but they are becoming more selective after a strong year-to-date run and recent profit-taking.

For fixed income, the market will be watching how aggressively the authorities continue to absorb liquidity. A reported CBN Q3 Treasury bill issuance programme of ₦5.8 trillion, if sustained, could keep short-duration yields attractive and maintain competition for equity market flows.

Globally, the focus is on weaker U.S. jobs data, Fed minutes due this week, and softer oil prices after OPEC+ agreed to raise August output. For Nigeria, the oil move is especially important. Lower Brent can reduce inflation pressure globally, but it may also narrow Nigeria’s oil revenue and FX buffer if prices fall too far.

The Big Picture:

The market question for the week is not simply whether Nigerian assets rise or fall. The real question is where capital feels best compensated.

Equities have momentum from strong nominal earnings, bank recapitalisation expectations, and inflation-linked revenue growth in selected sectors. But after sharp gains earlier in the year, investors are now more sensitive to valuation, earnings delivery, and dividend visibility.

Fixed income is becoming more competitive. The CBN retained the MPR at 26.5% at its May 19-20 MPC meeting, with CRR for deposit money banks at 45%, merchant banks at 16%, and non-TSA public sector deposits at 75%. That policy mix keeps liquidity tight and preserves the appeal of short-duration government paper.

The naira remains a key portfolio variable. Access Bank’s market rates page showed the CBN NFEM closing rate at ₦1,370.1904/$ on July 3. If dollar liquidity stays steady, the naira can remain supportive for foreign portfolio interest. If oil prices weaken further or dollar demand rises, FX stability becomes harder to preserve.

Nigeria Market Intelligence

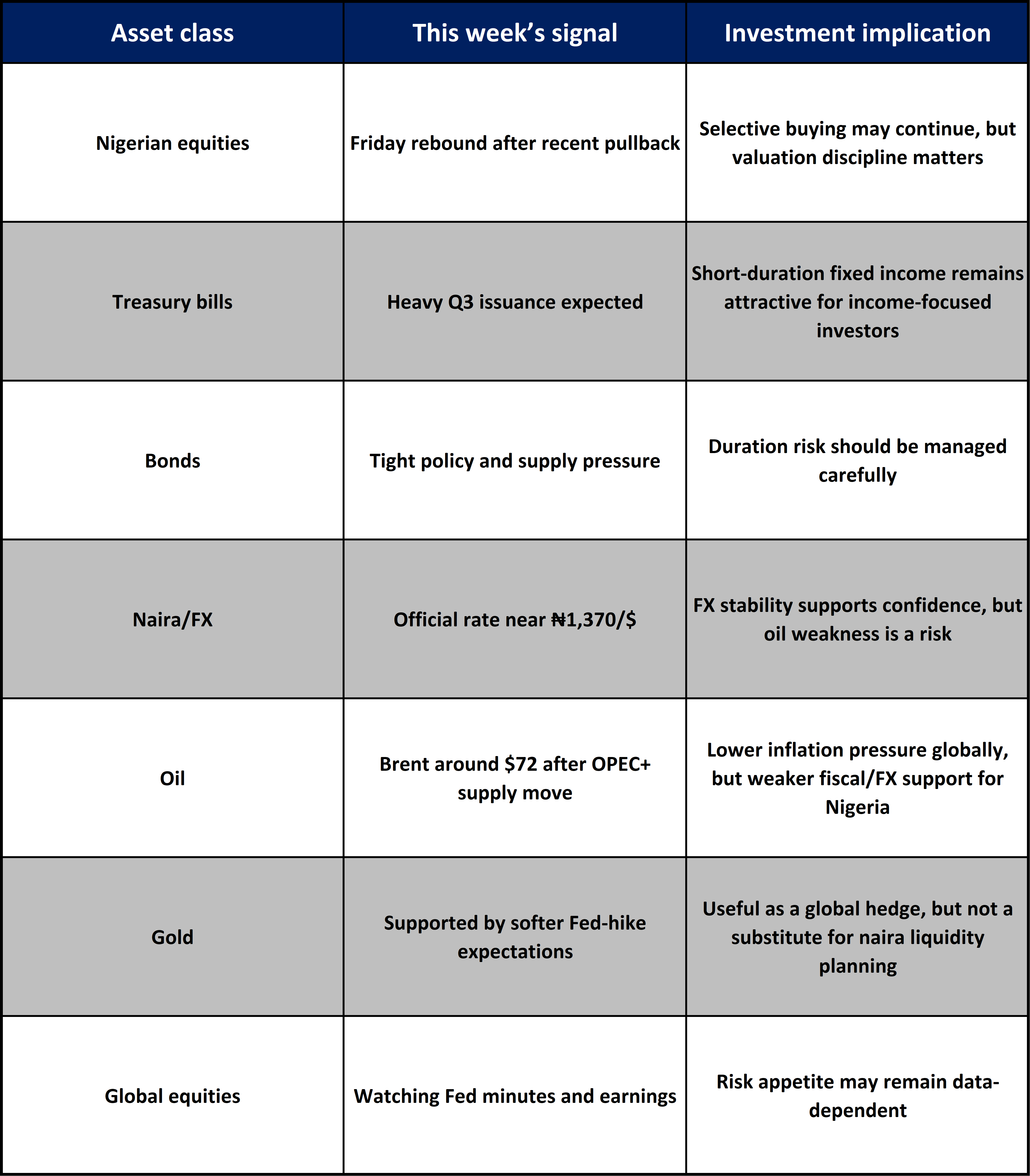

Equities: Friday’s rebound does not erase the recent correction

What happened: The NGX ASI rose 2.19% on July 3 to 229,240.34, but was still down 5.37% over the past month.

Why it matters: The rebound suggests bargain hunting, but the monthly decline shows investors are now testing whether earlier gains were overextended.

What it means for investors: This favours selective positioning over broad index chasing. Banks, telecoms, energy names, and high-cash-flow industrials should be judged by earnings resilience, dividend capacity, and FX sensitivity.

What to watch: Whether large-cap banks and telecoms continue to absorb liquidity or whether profit-taking returns after short rallies.

Fixed income: Treasury supply could anchor short-duration demand

What happened: CBN plans ₦5.8 trillion in Treasury bill auctions for Q3 2026, with ₦4.0 trillion reportedly in 364-day bills.

Why it matters: Heavy issuance can keep yields attractive and absorb system liquidity. It also means fixed income will remain a serious competitor to equities.

What it means for investors: Short-duration bills may remain attractive for investors prioritising cash yield, liquidity, and lower mark to market risk. Longer-duration bonds need more care because supply pressure and inflation uncertainty can affect pricing.

What to watch: Stop rates at upcoming NTB auctions, subscription levels, and whether banks and pension funds continue to support demand.

Inflation: The latest verified data still argues against an early policy pivot

What happened: Nigeria’s headline inflation rose to 15.93% in May from 15.69% in April. Food inflation was reported at 16.96% year-on-year in May, while month-on-month headline inflation eased to 1.75%.

Why it matters:he monthly slowdown is encouraging, but the annual rise means the CBN has limited room to ease too quickly.

What it means for investors: High nominal yields remain defensible, and equities with pricing power remain relevant. Consumer-facing companies without pricing flexibility may still face margin pressure.

What to watch next: June inflation data when released, especially food inflation and month-on-month momentum.

FX: Naira stability is still the market’s central confidence variable

What happened: The official NFEM closing rate was shown at ₦1,370.1904/$ on July 3, while CBN’s own exchange-rate page identifies NFEM as the official volume-weighted rate.

Why it matters: Stable FX supports foreign participation, improves planning for import-dependent businesses, and reduces the risk premium attached to Nigerian assets.

What it means for investors: A steady naira supports banks, foreign investors in local debt, and companies with imported input costs. Renewed weakness would quickly revive inflation and valuation concerns.

What to watch: NFEM turnover, external reserves, oil receipts, and any widening between official and parallel-market pricing.

Global Market Intelligence:

Fed: The jobs report has made this week’s Fed minutes more important

What happened: U.S. nonfarm payrolls rose by 57,000 in June, while unemployment was 4.2%, according to BLS. The Fed held its target range at 3.50%-3.75% on June 17.

Why it matters: Softer jobs data reduces pressure for further tightening, but the Fed still described inflation as elevated.

What it means for Nigerian investors: Lower U.S. yield pressure would be positive for frontier-market flows. But if the Fed minutes sound hawkish, the dollar and U.S. yields could regain strength, making Nigerian local assets less attractive to offshore investors.

What to watch: FOMC minutes this week and the next U.S. CPI release scheduled for July 14.

Oil: OPEC+ supply increase puts Brent under pressure

What happened: OPEC said seven OPEC+ countries agreed on July 5 to implement a 188,000 barrels per day production adjustment in August. Brent traded around $72/bbl on July 6, down sharply over the past month.

Why it matters: Lower Brent can ease global inflation pressure, but Nigeria needs healthy oil prices and production discipline to support revenue and FX inflows.

What it means for investors: Softer crude is helpful for inflation expectations but less helpful for Nigeria’s fiscal and external position. Oil-linked equities and naira sentiment may become more sensitive to further declines.

What to watch: Brent’s ability to hold above the low-$70s, OPEC+ compliance, and Nigeria’s own production/export performance.

Dollar and U.S. yields: Frontier-market flows still depend on global rates

What happened: The U.S. 10-year Treasury yield was around 4.47% on July 6, while the dollar index was around 101.

Why it matters: High U.S. yields keep a floor under global required returns. A firmer dollar can also pressure emerging and frontier-market currencies.

What it means for Nigerian investors: High U.S. yields keep a floor under global required returns. A firmer dollar can also pressure emerging and frontier-market currencies.

What to watch: Whether U.S. yields fall after softer labour data or rebound if Fed minutes reinforce inflation concern.

Asset Class Implications:

Ranora View:

The most important investment implication this week is that Nigerian investors are being paid to be selective.

Equities still have a role, especially in sectors with strong cash flow, pricing power, and balance-sheet resilience. But after the market’s earlier strength and recent correction, the easy broad-market trade is less compelling. Investors should be asking whether each equity position can justify its valuation through earnings, dividends, or structural growth.

Fixed income deserves serious attention. If Treasury bill issuance stays heavy and policy remains tight, short-duration instruments can offer attractive carry without forcing investors too far out on the curve. That does not mean avoiding equities. It means the hurdle rate for equity exposure is now higher.

For businesses, the key watchpoint is FX. A stable naira supports planning and margin visibility. A weaker oil backdrop, however, can quickly make FX liquidity the market’s main concern again.

What to Watch Next:

NTB auction stop rates and subscription levels.

NGX sector rotation, especially banks, telecoms, industrials, and oil and gas.

NFEM turnover and whether the naira holds near recent official levels.

FOMC minutes and the tone around inflation after weaker U.S. jobs data.

Brent crude, especially whether OPEC+ supply pressure pushes prices below the low-$70s.

Question of the day:

If Treasury bill yields remain attractive, would you still increase Nigerian equity exposure this quarter, or would you wait for clearer earnings confirmation?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.