The Week Ahead: Tight Liquidity, Sticky Inflation, and the Next Test for Risk Appetite

Ranora Market Outlook - Nigeria enters the week with policy rates on hold, liquidity under pressure, and strong fixed-income demand, while global markets wait for U.S. PCE data and the next signal ..

Opening View

This week opens with one clear message for Nigerian investors: the Central Bank is not ready to ease financial conditions meaningfully. The CBN held the MPR at 26.5% on May 20, just days after April inflation ticked up to 15.69%, and it followed that decision with an aggressive liquidity mop-up through OMO. That combination matters. It suggests policymakers are trying to preserve naira stability and contain renewed price pressure rather than support lower domestic yields in the near term.

The fixed-income market is already responding. The May 20 Treasury bills auction drew N1.11 trillion in subscriptions, with the 364-day bill clearing at 20.69%, while the May 18 DMO bond auction cleared around 17.00% to 17.04% on the 2035 and 2037 reopenings. Investors are still willing to lock in sovereign yields, especially where they see policy discipline and relative FX stability. The naira has remained broadly steady around the high-N1,300s in the official market, while external reserves rebounded to $49.49 billion as of May 15.

Globally, the market tone is less comfortable. U.S. yields have pushed higher, oil remains elevated, and April U.S. inflation re-accelerated to 3.8%. That raises the stakes for Thursday’s U.S. PCE release. For Nigeria, this week is not just about local policy. It is about whether the external backdrop keeps rewarding high-yield frontier assets or starts to challenge them again.

The Big Picture:

Nigeria is starting the week with a relatively constructive policy-credibility story, but not yet a benign macro story. The CBN’s posture is helping sustain demand for naira assets, yet the inflation re-acceleration and continued liquidity tightening mean investors should not assume a smooth glide path to lower rates.

The global backdrop is also turning more selective. Higher U.S. Treasury yields, firmer oil prices, and a still-restrictive Federal Reserve outlook could keep the dollar supported and make foreign capital more discriminating. That does not automatically hurt Nigeria, but it raises the bar. Nigeria now needs to keep delivering on FX stability, reserve resilience, and policy consistency to hold investor confidence.

Five Things That Matter This Week

Monetary policy and liquidity

What is happening: The CBN held the MPR at 26.5% on May 20 and then mopped up N3.69 trillion in OMO on May 21.

Why it matters: This is a strong signal that the Bank is still prioritizing inflation control and FX stability over easier system liquidity.

What to watch: Whether money-market tightness pushes more demand into short-duration sovereign paper and keeps front-end yields elevated.Treasury bills and bonds

What is happening: Demand for government paper remains strong. The May 20 NTB auction was heavily oversubscribed, especially at the 364-day tenor, and the May 18 bond auction cleared at 17% area yields.

Why it matters: Investors still see value in locking in sovereign yields, particularly if policy remains tight and naira volatility stays contained.

What to watch: Whether stop rates continue to drift lower on demand or remain sticky because inflation risk has turned up again.FX and external reserves

What is happening: The naira has been relatively stable in the official market, while reserves rose to $49.49 billion by May 15 after an earlier drawdown.

Why it matters: FX stability is one of the main reasons local fixed income and financial assets remain investable for both domestic and offshore accounts.

What to watch: Whether reserve support continues without a renewed depletion cycle if external conditions tighten.Nigerian equities

What is happening: The NGX is coming off a very strong early-2026 run, but recent trading has shown more profit-taking and greater stock selectivity.

Why it matters: The market is moving from broad rerating into a phase where earnings durability, dividend visibility, and sector positioning matter more.

What to watch: Whether banks, industrials, and select telecom names continue to attract rotation, or whether higher fixed-income yields cap further upside.Global macro and oil

What is happening: U.S. CPI rose 3.8% year-on-year in April, Treasury yields have pushed to multi-month highs, Brent settled at $103.54 on May 22, and U.S. PCE data are due on May 28.

Why it matters: Higher U.S. yields can tighten global financial conditions, while elevated oil supports Nigeria’s revenue outlook but also risks imported inflation through energy and freight costs.

What to watch: Thursday’s U.S. PCE release, Fed commentary, and whether oil holds above $100 ahead of the June 7 OPEC+ meeting

Nigeria Market Intelligence:

CBN held the MPR at 26.5% on May 20, signalling that February’s 50bp cut was not the start of a rapid easing cycle.

April headline inflation rose to 15.69% from 15.38% in March, interrupting the earlier disinflation trend.

The CBN’s May 20 NTB auction drew N1.11 trillion in subscriptions; the 364-day stop rate came in at 20.69%, reinforcing demand for duration at the short end.

The CBN’s N3.69 trillion OMO mop-up on May 21 points to continued liquidity tightening rather than accommodation.

External reserves stood at $49.49 billion as of May 15, while the naira remained broadly stable around N1,372/$ in the official market.

Global Market Intelligence:

U.S. April CPI rose 3.8% year-on-year, with core CPI at 2.8%, keeping inflation concerns alive.

Fed minutes released on May 20 showed policymakers still navigating inflation, labour-market, and financial-stability trade-offs.

The U.S. 10-year yield hit 4.663% on May 19, its highest since January 2025, while the 30-year yield touched its highest since 2007.

China’s April data disappointed: industrial output growth slowed to 4.1%, while weak retail momentum reinforced concern around domestic demand.

Euro area inflation rose to 3.0% in April from 2.6% in March, showing that Europe is also dealing with renewed price pressure.

Brent settled at $103.54 on May 22, and oil remains the most important global variable for Nigeria this week.

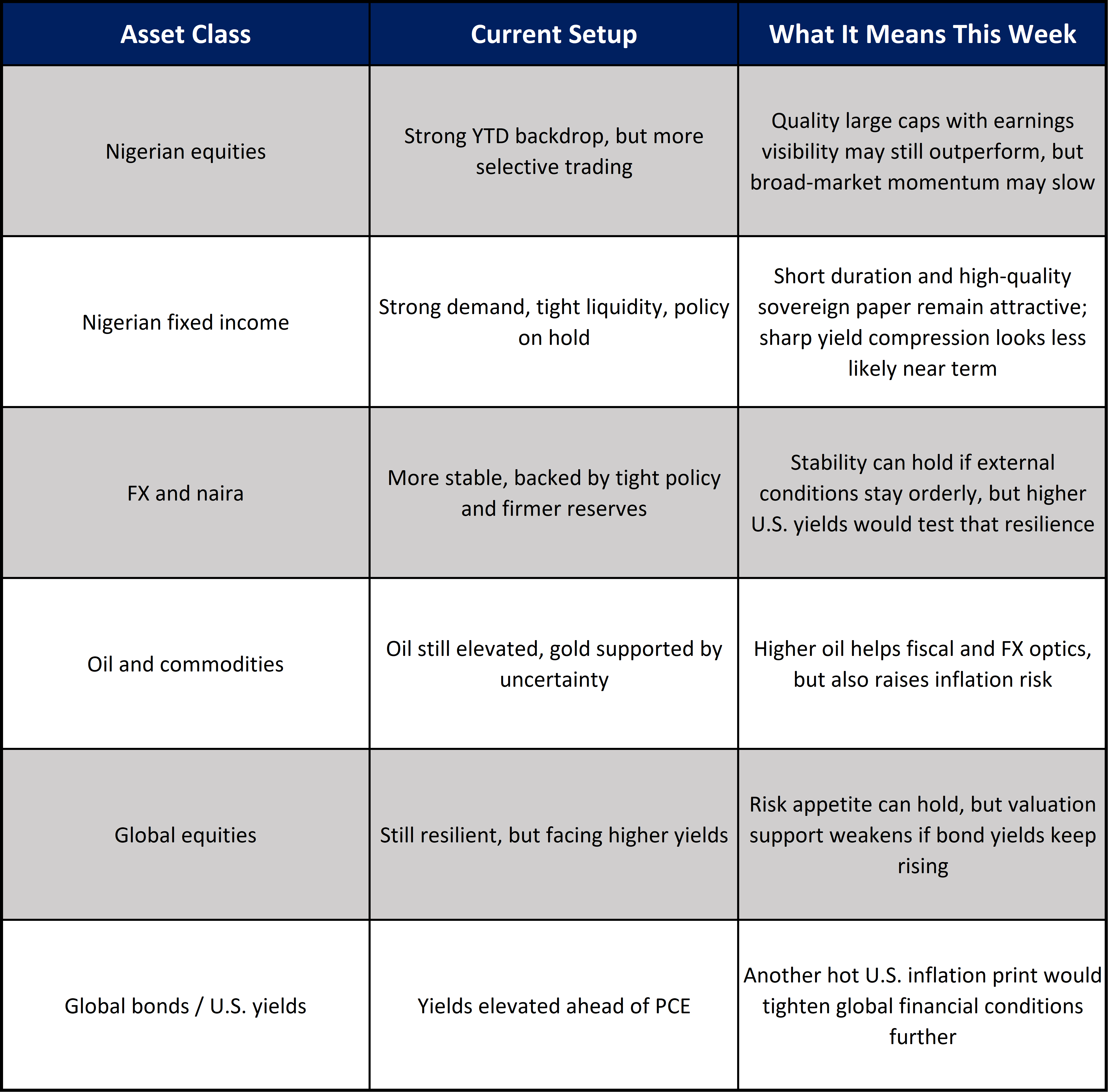

Asset Class Implications:

Ranora View:

The main market message for the week is that Nigeria’s policy mix is still supportive for local fixed income, but not yet supportive for a broad risk-on move across all asset classes. The CBN is effectively telling the market that naira stability and inflation control remain the priority. That should keep short-duration fixed income attractive and could continue to support bank earnings through strong asset yields.

For equities, the trade is becoming more selective. This is less about owning the whole market and more about owning the parts of the market that can defend margins, pay dividends, and benefit from a still-tight monetary environment. If U.S. PCE comes in hot and Treasury yields push higher again, Nigeria may still hold up better than weaker frontier peers, but the cushion will come from domestic carry, not from abundant global risk appetite

What to Watch Next:

U.S. PCE inflation and Q1 GDP revision on Thursday, May 28

Whether Nigerian money-market conditions stay tight after the latest OMO mop-up

Any follow-through in NTB and bond market pricing after last week’s strong demand

Official-market naira direction and whether reserve improvement continues

Oil price behaviour ahead of the June 7 OPEC+ meeting

Question of the day:

If U.S. yields stay elevated while the CBN keeps domestic liquidity tight, does Nigeria become more attractive as a carry market, or does that eventually cap equity upside too sharply?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.