NLC Rejects New NNPC Fuel Price Template - ThisDay

The Nigeria Labour Congress (NLC) has deplored the announcement of a new regime of prices for petroleum products by the Nigerian National Petroleum Corporation Limited (NNPCL). It described NNPC’s action as ambush to the ongoing meeting of stakeholders in the oil and gas sector to resolve the issue of fuel subsidy removal by the federal government

CBN multiple exchange rates may increase debt burden – World Bank - Punch

The President of the World Bank Group, David Malpass, has warned that Nigeria’s parallel exchange rate is harmful as it worsens future debt service payments and increases the risk of debt distress.

Global

The debt ceiling deal has passed through the House of Representatives with a 314-117 vote.

The deal now heads to the Senate which has 5 days to approve it before the June 5 deadline set by Treasury Secretary Janet Yellen.

Some Republican senators, however, have suggested proposing amendments to the bill aimed at extracting further spending cuts.

If any amendments are passed, the bill would have to return to the House for another vote before it can be signed into law.

Meanwhile, the Treasury’s cash balance dropped to $37.4 billion on Tuesday, the lowest level since 2017.

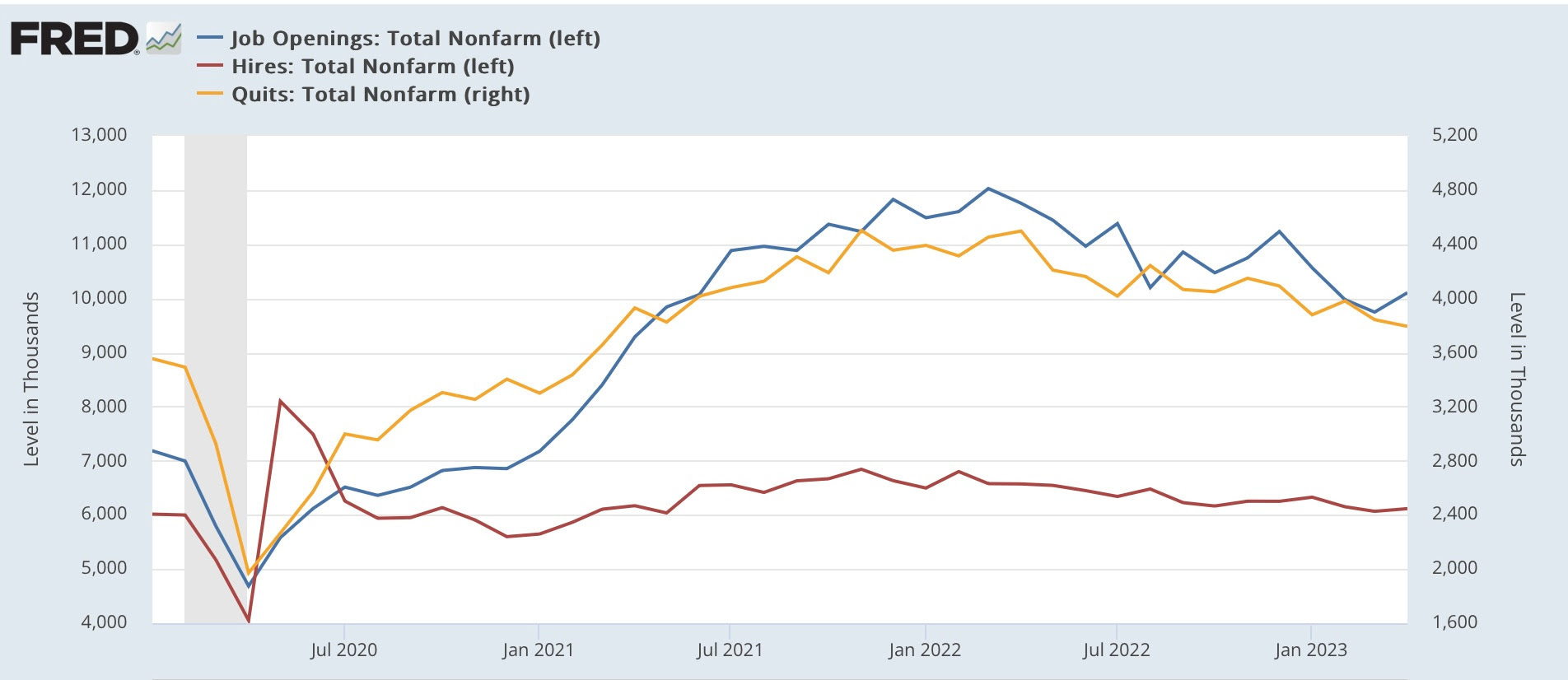

Job openings in the US rose unexpectedly in April, increasing to 10.1 million (from 9.7 million) and topping estimates of 9.375 million.

The surge reverses a 3-month streak of declines in vacancies.

The quits rate ticked down to 2.4%, the lowest in more than 2 years, and—in contrast to openings—suggests easing in the labor market.

The ratio of openings to unemployed people, however, rose to its highest in 3 months at 1.8 which is not what the Fed wants to see.

Cause for concern: at 31%, the survey’s response rate remains at record lows.

A few prominent media groups will be inexplicably absent from OPEC’s next meeting in Vienna on June 4.

In an unusual move, the group has refused to extend invitations to Bloomberg, Reuters, and the Wall Street Journal to cover the event.

While no reason was offered, many suspect the decision came down from Saudi Arabia’s energy minister, Prince Abdulaziz bin Salman, who has made a concerted effort recently to raise prices.

Weekly Investment Watchlist

Market Commentary

Asia and Australia

Japan's manufacturing activity expands for the first time in seven months.

South Korea S&P Global PMI reflected a continued slowdown in the country's manufacturing output but hinted at the slowing pace of decline.

Repricing of the RBA rate path continues with futures now pricing in a 100% chance of a rate increase by August (vs zero probability in mid-May).

India's GDP growth accelerated to 6.1% in Q4 y/y (ending 31 Mar-23) from 4.5% y/y growth in Q3, boosted by government and private spending, and manufacturing.

Europe, Middle East, Africa

The details of the ECB May meeting showed most members backed the decision to raise rates by the more moderate 25 bps, though some members initially expressed a preference for a larger move.

Eurozone inflation cools in May but will not stop the ECB hiking cycle. Flash CPI is at 6.1% y/y versus consensus 6.3% and prior 7.0% gain, while core is at 5.3% versus 5.5% forecast and prior 5.6%.

UK manufacturing activity declines for the third straight month in May

Eurozone manufacturing downturn deepens in May. Manufacturing PMI falls to a 36-month low of 44.8 vs the preliminary reading of 44.6 and April's outcome of 45.8.

The Americas

Fed officials signal support for leaving rates unchanged in June while retaining the option to hike again in coming months

Deutsche Bank warns of an imminent wave of corporate debt defaults. They forecast peak default rates to reach 9% for U.S. high-yield debt, 11.3% for U.S. loans, 4.4% for European high-yield bonds, and 7.3% for European loans.

BofA noted that its Global Earnings Revision Ratio improved significantly last week from 0.77 to 0.90 to reach the highest level in over a year. It would seem that Earnings revisions are being improved to cater to the better-than-expected results delivered in Q1, 2023.

The Week Ahead:

Monday: Fed talk - Bullard, Barkin, Bostic, Daly

Tuesday: US Manufacturing PMI comes in at 48.5; est: 50.2, US new homes sales come in at 683k; est: 663k.

Wednesday: FOMC minutes

Thursday: Initial jobless claims, GDP growth, pending home sales

Friday: Core PCE, personal income & spending, durable goods orders, Michigan consumer sentiment

Investment Tip of The Day

Emotions can cloud judgment when it comes to investing. Avoid making impulsive decisions based on fear or greed and rely on your research, analysis, and long-term strategy.

Meme of the Day

Disclaimer: The information contained in this report is intended for informational purposes only and should not be considered as investment advice. The information is obtained from sources believed to be reliable, but accuracy and completeness cannot be guaranteed.

Thanks for reading Ranora Daily! Subscribe for free to receive new posts and support our work.