Think Thursday

Ranora Daily - Your daily source for reliable market analysis and news.

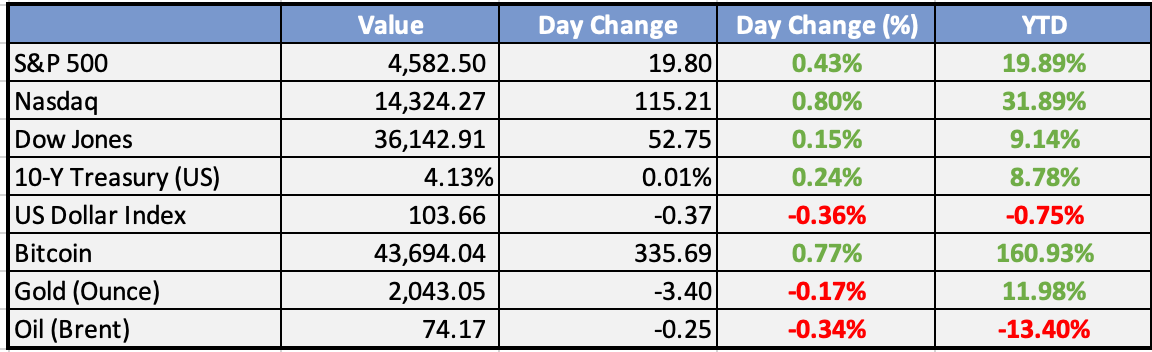

Market Data

Local

Global

x*Data as of 4pm WAT

Market News

Local

TCN, Discos to complete 53 CBN-funded projects in May - Punch

The Central Bank of Nigeria, Transmission Company of Nigeria, and power distribution companies will in May next year complete a total of 53 power projects worth N122bn currently under construction across the country.

FG to spend N100bn on auto-gas, CNG buses, EVs - Punch

The Presidential Compressed Natural Gas Initiative says N100bn has been earmarked to facilitate the deployment of CNG buses across the nation.

Five multinationals dump Nigeria in 10 months - Punch

At least five multinationals have winded down operations in Nigeria in the last 10 months, an analysis of separate notices filed by the firms has shown.

Stop Tax Waivers, Senate Tells Executive - Leadership

The Senate has asked the Executive arm of government to stop tax waivers granted to companies in Nigeria.

NNPC Seals Deals to Deliver LNG to Domestic, Int’l Gas Markets - ThisDay

The Nigerian National Petroleum Company Limited (NNPC) yesterday announced that it had signed two major agreements to deliver Liquefied Natural Gas (LNG) to the domestic and international gas markets.

Oando Plc Announces Federal High Court’s Adjurnment of Hearing on its Scheme of Arrangement - Oando

Global

Traders eye ECB key rate at 2.5% as they ramp up bets on cuts - Bloomberg

European markets are betting on an aggressive rate cut cycle by the ECB, with six quarter-point cuts expected in 2024 and a possible start in Q1. This optimism follows a slowdown in inflation and comments from Isabel Schnabel, an ECB hawk, suggesting further tightening is unlikely. However, some analysts warn that expectations for cuts might be too optimistic.

Russia and Saudi Arabia urge all OPEC+ powers to join oil cuts - Reuters

Russia and Saudi Arabia, the two largest oil exporters, are calling for all OPEC+ members to join the agreement on output cuts for global economic stability. This follows Putin's visit to Riyadh and meetings with the Saudi crown prince, emphasizing the importance of commitment to the agreement and hinting at specific oil powers who haven't yet joined.

Global Market Commentary

Overview

European equities continued the positive momentum initiated in Asia, benefiting from a decline in long-term bond yields influenced by a softer US ADP private payrolls report and lower US Q3 labor costs. Notable events on the horizon include China’s November trade data and US weekly jobless claims.

Currencies/Macro:

The US dollar was mostly flat or stronger against major FX currencies.

EUR/USD slipped -0.3% to 1.0765, reaching fresh lows since US October CPI on November 14.

GBP dropped -0.3% to 1.2555, while USD/JPY ticked up to 147.35.

US November ADP private payrolls rose 103k, softer than the estimated 130k, and October was revised to 106k from 113k.

US final Q3 unit labor costs pulled back -1.2%q/q, and productivity rose to 5.2%.

US October trade deficit was close to consensus at -USD64.3bn.

The Bank of Canada left policy unchanged at 5.0%, acknowledging a shift in the economy’s status from “excess demand” and emphasizing the current policy’s role in restraining spending as the labor market eases.

Interest Rates:

The US 2yr treasury yield held firm, lifting 1-2bps to 4.595%, while 10yr yields declined -5bps to 4.11%.

Pricing for the Fed funds rate for December 14 remained unchanged, but March 2024 pricing for a cut approached 75%.

December 2024 Fed pricing pared back to -125bps or 4.08%.

Credit Spreads:

Credit spreads were little changed, with Main at 67 and CDX at 62.5.

Strong rally in US IG cash through November slowed, and primary volumes eased ahead of payrolls on Friday.

Commodities:

Crude hit five-month lows despite EIA reporting falling crude inventory, production, and exports last week.

January WTI contract down 4% at $69.40, and February Brent contract down 3.7% at $74.33.

Gasoline inventory surged, and distillate jumped; implied gasoline demand plunged.

Metals slumped as weak China data and deteriorating technical picture weighed on sentiment.

Copper fell 1.2% to $8,341, zinc fell 1.4% to $2,418, nickel fell 2.6% to $16,280.

Iron ore markets remained resilient; January SGX contract up $2.20 at $131.29, 62% Mysteel index up $2.15 at $133.40.

Day Ahead:

Eurozone: Minimal expectation for the final estimate of Q3 GDP to differ from the prior quarter’s print.

US: Initial jobless claims near lows; October consumer credit likely reflecting the impact of rate hikes.

The Week Ahead:

Monday:

Tuesday:

US ISM Services PMI is at a current level of 52.70, up from 51.80 last month

US JOLTS Job Openings fall to 8.7 million in October vs. 9.3 million forecast

Wednesday:

US ADP Non-Farm Employment increased by 103,000 jobs in November and annual pay was up 5.6 percent YoY

Thursday:

Unemployment Claims (US)

Friday:

Average Hourly Earnings m/m (US)

Non-Farm Employment Change (US)

Unemployment Rate (US)

Prelim UoM Consumer Sentiment (US)

Investment Tip of The Day

Consider Factor Rotation Strategies: Explore factor rotation strategies that adjust exposure to factors like value, momentum, or quality based on prevailing market conditions.

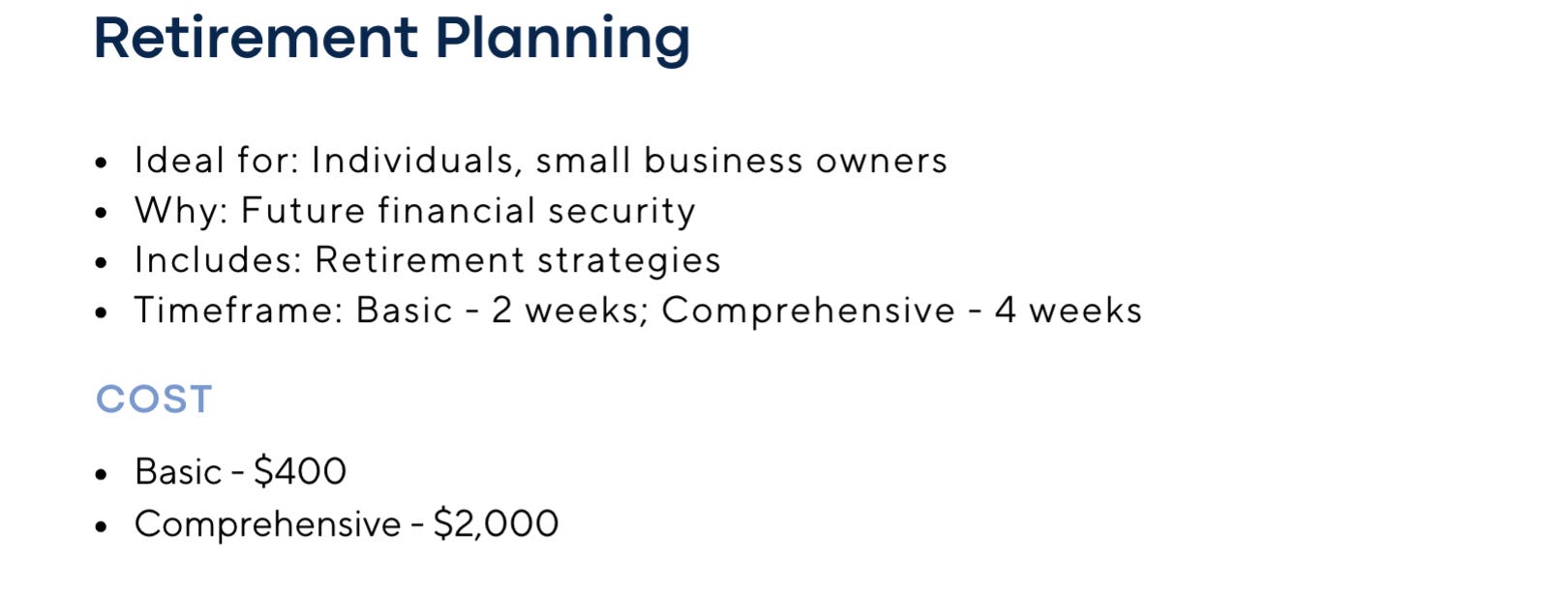

Service Spotlight of the week - Wealth Management

Meme of the Day