Trading Thursday

Ranora Daily - Your daily source for reliable market analysis and news.

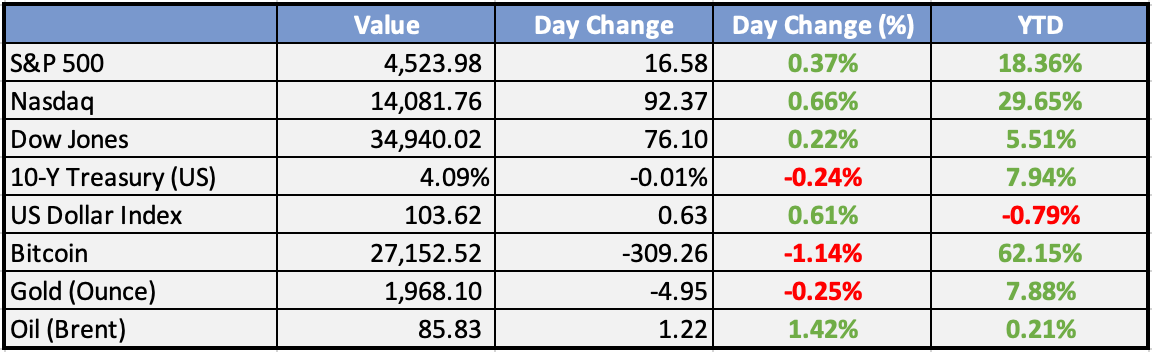

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Egypt approves issuing new batch of $500 mln yen-denominated samurai bonds - Ahram

Egypt has approved the issuance of a new batch of yen-denominated bonds worth $513 million, aimed at boosting its foreign reserves and securing additional funding for development projects.

Naira continues free fall as NNPC, AFREXIM $3bn Loan deal drags - Daily Trust

The Naira continued to fall against the dollar on Monday, trading at N774/$1, as the much-celebrated $3 billion emergency loan from the African Export-Import Bank (Afrexim) to stabilize the country's volatile foreign exchange market drags. The currency has lost more than 10% of its value against the dollar this year.

Global

US companies add 177k jobs, smallest gain in five months - Bloomberg

According to the ADP Research Institute, a recent report on Wednesday revealed that companies hired 177,000 employees this month, marking the lowest increase since March. The leisure and hospitality sector, which has significantly contributed to employment growth, experienced its weakest performance in over a year.

Under new Biden proposal, salaried workers earning up to $55k per year could get overtime pay - CNBC

Biden administration proposes extending overtime pay eligibility to around 3.6 million salaried workers. The new rule raises the threshold for non-hourly professionals to qualify for overtime from $35,568 to $55,068 annually. Automatic increases included. Public comments invited before finalization.

Visa, Mastercard prepare to raise credit-card fees - WSJ

Visa and Mastercard plan to raise fees for merchants accepting credit card payments, beginning in October and April. The fee hikes, including those for online purchases, may impact consumers as well. Both companies have not responded to requests for comment.

Weekly Investment Watchlist

Market Commentary

Asia and Australia:

Asian stock markets concluded on a mixed note on Thursday. Greater China markets opened with optimism but ended in the red once again, marking a challenging month for the country’s equity markets. Losses were observed in Seoul and Taipei, and India faced declines due to a drop in Adani stocks following a negative promoter investor report.

Several Chinese lenders are poised to reduce deposit rates starting from September 1st, marking the second round of rate cuts in less than three months.

PBOC hosted a symposium in collaboration with other regulators, financial institutions, and private enterprises on Wednesday, pledging to enhance access to funding within the financial sector.

China took steps to stabilize the finances of a troubled shadow bank, possibly setting the stage for a state-led rescue of Zhongrong, as reported by Bloomberg.

Japan’s industrial production fell softer than expected, registering a decline of -2% in July. In contrast, retail sales exceeded expectations with a 2.1% rebound. The positive retail sales figure could signify a path toward sustainable consumption, aligning with the BoJ’s objectives.

South Korea’s industrial production experienced a -8.0% year-on-year contraction in July, missing the consensus forecast of -6.0% and continuing its ten-month streak of decline. This marks the longest stretch of industrial output contraction since records began in 1976.

Europe, Middle East, Africa:

European equity markets displayed mixed performance with a predominantly firmer trend. Real Estate, Financial Services, and Travel/Leisure sectors led the gains, while Food/Beverage/Tobacco, Consumer Products/Services, and Healthcare sectors lagged.

Money market traders adjusted expectations for an ECB rate hike next month from 50% to 30% following a speech by ECB’s Schnabel and Eurozone inflation data.

German retail sales for July demonstrated a decline of 0.8% month-on-month, falling short of the expected 0.3% increase. This translated to a year-on-year decline of (2.2%), deviating from the expected (1.4%). Despite a gradual improvement since March 2023, the current print stalled this trend.

The Lloyds Bank business barometer for the UK surged by 10 points to reach an 18-month high of 41% in August.

Riksbank’s Thirteen expressed that the weakness of the SEK currency is not warranted.

Zambia’s inflation accelerated to a 16-month high in August, with prices rising by 10.8% compared to the previous year.

The Americas:

Dollar General witnessed a pre-market decline of -16.5% after posting results that missed expectations on multiple fronts. The company highlighted increased theft and lowered its FY EPS guidance from $8.10 to $7.30, against an estimated $10.

Visa released its payment volume update after Wednesday’s close. Street assessments leaned slightly positive, emphasizing a rise in US volume growth from 5% in July to 7% in August.

Salesforce reported positive Q2 results, particularly highlighting 11% year-on-year cc cRPO growth, surpassing guidance. The company’s Q3 guidance for 10% growth was also well-received.

Crowdstrike’s Q2 FY2024 results aligned with analyst expectations, with revenue increasing by 36.7% year-on-year to $731.6 million. The company anticipated next quarter’s revenue to be around $776.7 million, in line with analyst estimates. On the earnings front, Crowdstrike reported a non-GAAP profit of $0.74 per share, an improvement from the $0.36 per share profit in the same quarter last year.

Goldman Sachs noted that CTA equity demand has shifted to a buying position, with substantial demand anticipated in the next five days, regardless of whether the market is flat, up, or even down. The firm projected a daily demand of $11 billion over the next five days and $107 billion over the next month, assuming a flat market.

Shopify and Amazon reached an agreement for merchants to offer “Buy with Prime” on Shopify stores.

The Week Ahead:

Monday:

China PBOC Interest Rate Decision

Tuesday:

US Existing Home Sales Change (MoM)(Jul)

Wednesday:

S&P Global/CIPS Composite PMI (Aug) PREL (UK)

Retail Sales (MoM)(Jun) (Canada)

S&P Global Manufacturing PMI (Aug) PREL(US)

Consumer Confidence (Aug) PREL (EU)

Thursday:

US Q2 GDP second print comes in at 2.1%; lower than the previous estimate.

US ADP jobs report shows we added 177k jobs; the previous 371k. Smallest gain in five months.

US pending home sales rose 0.9% for the month of July.

Friday:

GFK Consumer Confidence (Aug) (UK)

Investment Tip of The Day

Regular Portfolio Rebalancing: Rebalance your portfolio periodically to maintain your desired risk level and alignment with your financial goals.

Meme of the Day