Trading Tuesday

Ranora Daily - Your daily source for reliable market analysis and news.

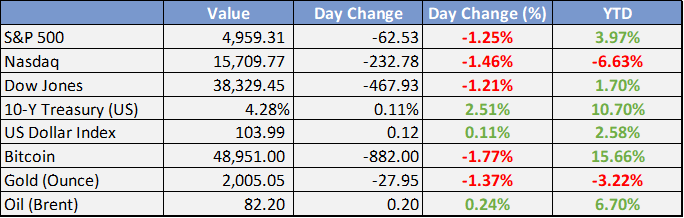

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

IMF forecasts $8bn fall in Nigeria’s 2024 foreign reserves - Punch

The International Monetary Fund has said Nigeria’s foreign reserves may fall to $24bn in 2024. The fund revealed this in its latest country report for Nigeria, indicating a significant drop and potential forex challenges for Africa’s largest economy. The country’s external reserves stood at $33.12bn as of February 8.

Outages: FG plans sanctions for non-performing Discos - Punch

Power distribution companies that are performing below stipulated standards in the Nigeria Electricity Supply Industry are going to lose 50 per cent of their operating expenditures, the Federal Government declared on Monday.

Shell supplies 475,000 barrels of crude oil to P’Harcourt refinery - Punch

he Shell Petroleum Development Company of Nigeria Limited said it has completed the supply of 475,000 barrels of crude oil to the Port Harcourt Refining Company Limited. The SPDC said this was in furtherance of the Federal Government’s commitment to increase domestic refining capacity and make petroleum products more readily available in the country.

Port workers threaten shutdown over FG planned 50% revenue slash - Punch

The Maritime Workers Union of Nigeria and Senior Staff Association of Statutory Corporations and Government Owned Companies maritime branch have issued a warning that they will close down the country’s seaports if the Federal Government proceeds with its plan to cut by 50 per cent the internally generated revenues from the Federal Government-owned enterprises especially Nigerian Ports Authority.

Global

UK to explore investment opportunities in Nigeria - Punch

The UK Minister for Business and Trade, Kemi Badenoch and the Prime Minister’s Trade Envoy to Nigeria, Helen Grant, will be meeting with British and Nigerian business leaders and investors to explore potential investment in the country.

CPI comes in at 3.1% YoY - CNBC

The consumer price index increased 0.3% in January, the Bureau of Labor Statistics reported. On a 12-month basis, that came out to 3.1%, down from 3.4% in December.

Shelter prices accounted for much of the rise, climbing 0.6% on the month, contributing more than two-thirds of the headline increase. On a 12-month basis, shelter rose 6%.

Stocks slid sharply following the release and Treasury yields surged higher.

Market Commentary:

Currencies/Macro:

The US dollar remained relatively stable against the major currencies, with slight variations noted against the Scandinavian currencies. The EUR/USD was consistent at around 1.0775, while the GBP/USD was unchanged at 1.2630. The USD/JPY decreased to 148.93 before returning to 149.30. The AUD/USD climbed to 0.6543 but later pared back to a 0.1% increase at 0.6530.

Inflation expectations in the US, as per the New York Fed's January survey, showed a slight decrease in the one-year ahead forecast to 3.00% from 3.01%, with the five-year outlook remaining steady at 2.5% and the three-year dropping to 2.4% from 2.6%, marking the lowest point in the survey's 11-year history. The survey also indicated a rise in earnings expectations to 2.8% for the coming year, though the prospect of finding a job dipped from 55.9 to 54.2.

Fed Governor Bowman emphasized the adequacy of the current policy rate given the existing economic conditions, indicating it's too premature for discussions on rate reductions, which aren't expected in the near term.

Interest Rates:

The yield on the US 2-year treasury edged down slightly from 4.48% to 4.47%, while the 10-year yield experienced some fluctuations but closed unchanged at 4.17%. Market expectations for the Federal Reserve's funds rate, presently at 5.375%, are to remain steady in the upcoming March meeting, with a 55% probability of a rate cut by May being priced in.

Credit markets saw an improvement, with the Main index tightening by 1.5 basis points to 57.5 and the CDX index improving by half a basis point, despite some retracement in gains as US stocks showed weakness. In the US investment grade (IG) cash market, there was little change, but the primary markets were notably active in anticipation of the Consumer Price Index (CPI) data and an expected decrease in supply activity tonight.

Commodities:

Crude oil markets experienced narrow trading fluctuations, with geopolitical tensions providing support but gains being limited by supply factors. The March West Texas Intermediate (WTI) contract saw a modest increase of 12 cents to $76.96, while the April Brent contract decreased by 17 cents to $82.02. Geopolitical developments included Israeli military actions in Rafah and a Houthi rebel attack on a US-listed bulk carrier, which sustained minor damage as reported by the UK navy, as it navigated the Bab el-Mandeb Strait. According to Bloomberg's ship tracking data, 27 tankers carrying approximately 27 million barrels of oil have reached Europe from the US Gulf this February, with an additional 40 tankers expected to bring the monthly total to a record 64.3 million barrels since the lifting of the US crude export ban in 2016. Goldman Sachs noted potential downward risks to Chinese oil demand projections due to a surge in electric vehicle sales but maintained a balanced outlook for Brent prices within the $70-90 range. Morgan Stanley updated its Brent price forecasts for 2024 and 2025 upwards by $2.50 to $5, citing tighter than expected market conditions. The European diesel premium over Brent has surged to a seasonal high, influenced by a combination of sanctions, plant closures, and regional disruptions.

Copper prices increased by 1% to $8,257, and zinc by 1.3%, even as zinc stockpiles at the London Metal Exchange grew significantly, driven by inflows into Singapore.

Iron ore trading was muted due to the Lunar New Year holidays in China, yet prices in Singapore received support from news of a BHP strike. The March SGX iron ore contract rose by $1.45 to $128.55, influenced by BHP train drivers announcing a 24-hour strike.

Investment Tip of The Day

Maximizing contributions to tax-advantaged accounts like retirement funds can significantly reduce your taxable income and allow investments to grow with tax benefits. This strategy enhances long-term wealth growth by minimizing tax impacts on investment returns. It's a foundational tip for efficient wealth management and tax optimization.