Trading Tuesday

Ranora Daily - Your daily source for reliable market analysis and news.

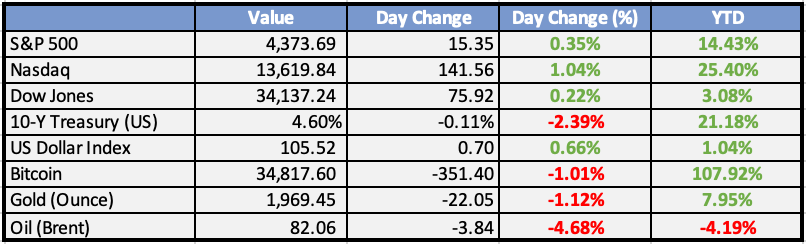

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Naira loses 4.24% on declining dollar supply - BusinessDay

Naira lost 4.24 percent of its value against the dollar at the official market, following a decline in dollar supply on Monday.After trading at the Nigerian Autonomous Foreign Exchange Market (NAFEM), on Monday, dollar was quoted at N809.02 as against N776.14 quoted on Friday, data from the FMDQ indicated.

Nigeria suffers $105bn hidden costs of food system – FAO - BusinessDay

The environmental, health and social hidden costs of Nigeria's agrifood system were at least $105.13 billion in 2020, a new report by the Food and Agriculture Organisation (FAO) has revealed.

Global

WeWork, once valued at $47 billion, files for bankruptcy - CNBC

WeWork filed for Chapter 11 bankruptcy protection, with the filing limited to its U.S. and Canada locations. The office-sharing company reported liabilities ranging from $10 billion to $50 billion. WeWork had previously struggled with the economic fallout of the pandemic, corporate collapses, and its inability to go public, losing significant value.

IMF Raises China 2023 Growth Forecast To 5.4% - Barrons

The International Monetary Fund (IMF) raised its 2023 growth forecast for China to 5.4% from the previous 5.0%, citing stronger domestic demand and recent policy measures by Beijing. After a challenging year, China's economy has shown signs of life, with a 4.9% GDP growth rate in the third quarter. The IMF also lifted its 2024 outlook to 4.6% from 4.2%.

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian equities traded mostly weaker on Tuesday. The greatest losses were in Seoul, which reversed much of its advance from the previous day. The Hang Seng also lost much of its Monday gains. Mainland China benchmarks ended a few points lower by the close. Losses were also seen in Australia, Southeast Asia, and India, although Taiwan saw a modest advance. Japan performed notably poorly, closing at its trough.

The Reserve Bank of Australia hiked their cash rate by 25 basis points to 4.35%, as was expected. They kept the door open for further hikes on inflation concerns. The bank also tweaked their inflation expectations higher to around 3.5% by the end of 2024 (compared to a prior forecast of 3.25%) and at the top end of the 2-3% target band by the end of 2025 (versus a prior forecast of 2.75%). The Australian Dollar gave up half of its gains from the previous week, while equities pulled back marginally.

Surprising numbers emerged from China, with a trade surplus of $56.53 billion, which was sharply lower than September’s surplus of $77.71 billion. Exports fell 6.4% year-on-year in October, which was much worse than the estimated 3.3% drop and the 6.2% decline in the previous month. However, imports unexpectedly rose by 3% year-on-year in the last month, compared to an estimate of a 4.8% drop and the 6.3% fall in September. This marked the first on-year growth since September 2022.

Japan also reported discouraging data on household consumption and wages, which are important data points for the Bank of Japan. Household spending dropped 2.8% year-on-year in September, slightly worse than August’s 2.5% drop. The biggest declines occurred in discretionary goods categories. Real wages contracted for an 18th month, falling 2.4% year-on-year in September, which was slightly shallower than August’s 2.8% contraction. While nominal wages rose by 1.2%, inflation is eroding purchasing power.

Europe, Middle East, Africa:

European equity markets were mostly lower on Tuesday. Markets experienced declines due to a backup in bond yields alongside poor China trade data. The worst-performing sectors included consumer services, energy minerals, and consumer durables.

Industrial production in Germany sank 1.4% MoM in September 2023, following a downwardly revised 0.1% fall in August. This was much worse than forecasts of a 0.1% decrease. It also marked the fourth consecutive month of falling industrial production, adding to further evidence of Germany’s economic weakness. The biggest downward impact came from the auto sector (-5%), electrical equipment (-4.4%), and pharmaceutical (-9.2%).

Saudi Aramco reported 3Q23 results, with operating income coming in at approximately US$62.5 billion (+10% QoQ and -22% YoY), and net income amounting to approximately US$32.9 billion (+13% QoQ and -21% YoY). The year-on-year decline in net income was largely driven by lower crude oil prices and volumes sold, partially offset by lower production royalties and taxes. The company generated free cash flows of approximately US$20.3 billion for 3Q23, including capex expenditures of the quarter at approximately US$11 billion (+22% YoY).

BoE’s chief economist Pill said that investors are not “unreasonable” to predict a rate cut next summer. Pill added that inflation should decline rapidly over the coming months, and this was seen as the clearest signal yet that the BoE is near or at the peak of its rate-hike cycle.

The Americas:

Minneapolis Fed President Neel Kashkari said that overtightening monetary policy is preferable to doing too little, and he’s concerned that inflation could tick up again. Fed speakers had expressed satisfaction with financial conditions tightening prior to the Fed meeting last week. However, last week saw a reversal of much of this, with yields moving lower, and the market gaining approximately 6% in a week.

Canada’s Ivey PMI came in at 53.4, a slight improvement from September. It revealed that employment, supplier deliveries, and price indices declined, while inventories gained. The Bank of Canada’s Q3 market participants survey showed median forecasts for modest GDP growth this year and next, with inflation easing to 2.2% by the end of 2024, and BoC rate cuts expected to begin in April.

There is a busy day of Fedspeak, with Barr, Schmid, Waller, Williams, and Logan all on the schedule.

The Week Ahead:

Monday:

Tuesday:

Wednesday:

Thursday:

Unemployment Claims (US)

Friday:

GDP m/m (UK)

Prelim UoM Consumer Sentiment (US)

Investment Tip of The Day

Stay Aligned With Financial Objectives: Continuously assess your investment choices to ensure they align with your evolving financial goals and life circumstances. Adjust your portfolio as needed to stay on track.

Meme of the Day