Trading Tuesday

Ranora Daily - Your daily source for reliable market analysis and news.

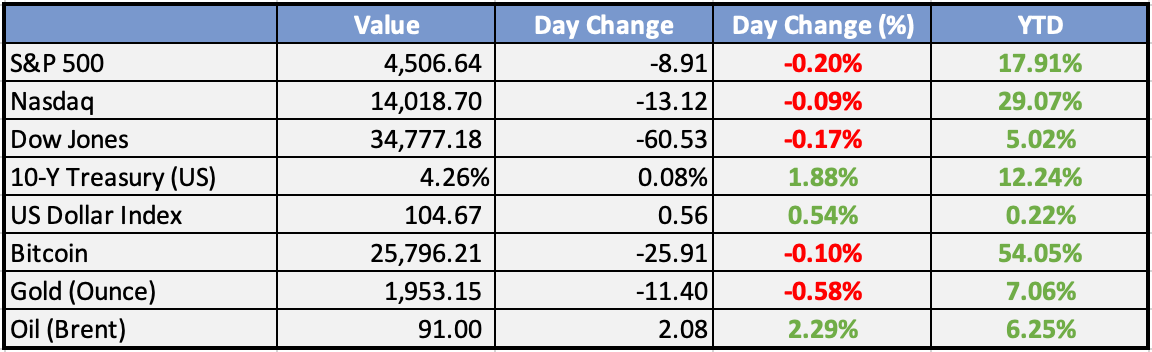

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

FG to engage terminal operators on $800m port rehabilitation - Punch

The Nigerian government plans to discuss a proposed N800 billion ($1.95 billion) rehabilitation of the nation's seaports with terminal operators. The project aims to enhance port efficiency and competitiveness, with government funding and terminal operators handling implementation.

Oando seals deal to acquire NAOC - Punch

Oando Plc has agreed with Eni to acquire 100% of the shares of its oil and gas unit, Nigerian Agip Oil Company Limited. The completion of the transaction is pending ministerial consent and regulatory approvals. This acquisition increases Oando's participating interests in several assets and infrastructure, including oil and gas fields, pipelines, gas processing plants, and power plants.

Global

Biden gets low marks on economy and major concerns about his age as he looks to rematch Trump - CNBC

A new poll highlights President Biden's weaknesses, with 60% of registered voters doubting his fitness for the job, and 73% believing he's too old to run for re-election. The poll also reveals majorities disapprove of Biden's handling of the economy, inflation, and middle-class growth. Voters are split between Biden and Trump for the 2024 election.

North Korea’s Kim Jong Un expected to meet Putin in Russia - WSJ

The US government has warned that negotiations between Russia and North Korea over arms deals are progressing, potentially involving a meeting between Kim Jong Un and Vladimir Putin in Russia. There are concerns that North Korea seeks technology in exchange for weaponry, which could advance its satellite and nuclear-powered submarine capabilities.

Weekly Investment Watchlist

Market Commentary

Asia and Australia:

Asian equities closed with mixed results on Tuesday. Hong Kong and mainland markets experienced significant losses, while Japan’s Nikkei saw a sharp late-session spike, ending in positive territory. Australia ended in the red, while Seoul, Taipei, and Southeast Asia had mixed performances. India posted modest gains.

China’s stock market surged previously due to stimulus measures in the property sector but retreated the next day due to weaker Caixin PMI services data. Caixin services PMI for August was reported at 51.8, falling short of consensus expectations of 53.5 and below July’s 54.1. Concerns regarding economic data may limit potential market rallies.

Country Garden made interest payments on two-dollar bonds just before the expiration of a 30-day grace period.

In the Philippines, inflation resurged due to rising rice prices, leading the government to impose price caps.

The Reserve Bank of Australia (RBA) maintained its policy rate at 4.1% during Governor Lowe’s final meeting. This marked the third consecutive meeting without a rate hike. Inflation has peaked but remains above the RBA’s policy rate at 4.9%. The RBA reiterated that further tightening may be necessary.

Several brokerages revised their yen outlook downward. Goldman Sachs reduced its year-end forecast to 150 yen per dollar from 140, followed by similar downgrades from JPMorgan (152 from 142) and Barclays (146 from 135). BofA also adjusted its year-end projection to 150 from the previous 145.

South Korea’s CPI edged higher to 3.4% year-on-year from July’s 2.3%, surpassing consensus expectations of 2.7%. This marks the first time in seven months that prices accelerated and the highest rate since April.

Europe, Middle East, Africa:

European equity markets mostly showed a softer performance. Financial services, basic resources, and energy sectors advanced, while China-exposed sectors, such as Construction and materials, Chemicals, and Luxury, lagged. Weaker data on China’s services activity contributed to the downturn in China-exposed sectors.

Retail was among the worst-performing sectors in European trade, as Barclays data indicated that UK consumer spending growth slowed down last month, indicating a weakening economy.

In August, the HCOB Eurozone Composite PMI revealed a faster contraction in the economy, with services activity declining. The HCOB Eurozone Composite PMI Output Index dropped to a 33-month low of 46.7, down from July’s 48.6. The HCOB Eurozone Services PMI Business Activity Index fell to a 30-month low of 47.9, below the preliminary reading of 48.3 and the prior month’s 50.9.

The Americas:

The US unemployment report released on Friday was seen as relatively benign. Despite an increase in the unemployment rate from 3.5% to 3.8%, the market suggests that the Federal Reserve might be done with rate hikes. The report also showed an addition of 187,000 payrolls, but prior revisions indicated a reduction of 110,000 jobs. This leaves the job market showing signs of weakening.

Chevron LNG workers plan to strike for two weeks starting on September 14 unless substantial progress is made in negotiations.

The upcoming week in the US is relatively quiet, with some scattered Fed speakers and the major economic data point being the Service PMI data.

The Week Ahead:

Monday:

Tuesday:

Wednesday:

ISM Services PMI (US)

Thursday:

Unemployment Claims (US)

Friday:

Investment Tip of The Day

Stay Disciplined: Adhere to your investment plan, avoiding knee-jerk reactions driven by short-term market noise.

Meme of the Day