Trading Tuesday

Ranora Daily - Your daily source for reliable market analysis and news.

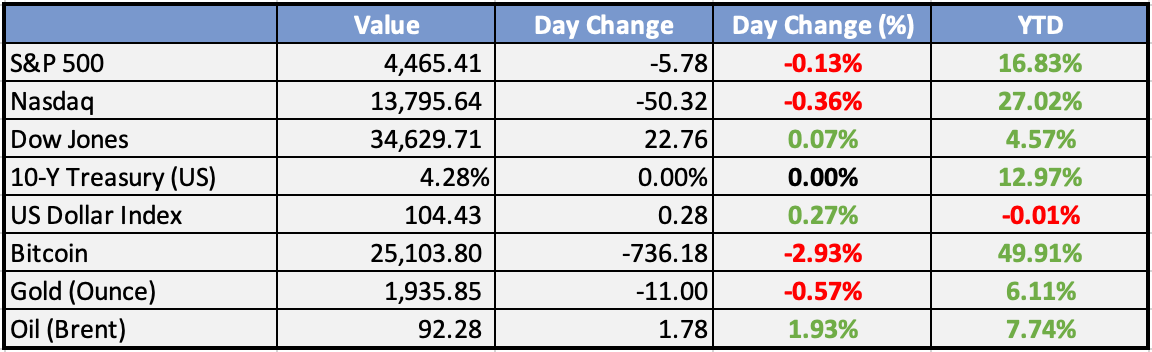

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

CBN directs banks to stop spending FX revaluation gains - Punch

The Central Bank of Nigeria (CBN) has instructed banks to refrain from utilizing foreign exchange (FX) revaluation gains, seeking to tighten control over FX transactions and manage its dwindling reserves more effectively. This directive comes amid Nigeria's ongoing foreign exchange challenges and efforts to stabilize its currency.

Operators excited as UAE lifts visa ban on Nigerians - Punch

The United Arab Emirates (UAE) has lifted its visa ban on Nigerian travelers, leading to excitement among operators in the aviation and tourism sectors. This decision, effective immediately, is expected to boost flight operations between the two countries and encourage tourism and business travel.

NERC inaugurates mobile app to address complaints - Nigeria Business News

The Nigerian Electricity Regulatory Commission (NERC) has introduced the Power Outage Reporting System (PORS) app to simplify and expedite the process of reporting power outages to Electricity Distribution Companies (DisCos). The app allows consumers to report complaints online and aims to improve electricity supply in Nigeria.

Olam Group denies reports of multi-billion dollar forex fraud in Nigeria, shares slump - Nigeria Business News

Olam Group has refuted allegations of a multi-billion-dollar forex fraud in Nigeria, causing a decline in its shares. The company denies involvement in any fraudulent activities and reaffirms its commitment to compliance and ethics in its business operations.

Global

2023 severe weather: $57B in damage and 253 people dead so far - CNBC

The United States has experienced a record number of billion-dollar weather disasters in 2023, with 23 such events causing over $57.6 billion in damages and claiming at least 253 lives. These disasters include wildfires and severe storms, such as the devastating wildfire in West Maui, Hawaii, and Hurricane Idalia hitting Florida.

Dollar drops most in two months as yuan, yen rally on pushback - Bloomberg

The US dollar experienced its most significant drop in two months due to indications from China and Japan that they might take measures to strengthen their currencies, leading to a notable surge in the yen and the yuan. This shift interrupted one of the longest-running dollar rallies in years, driven by the strong US economy and expectations of higher interest rates.

Oil holds near-yearly high ahead of OPEC, US market outlooks - Bloomberg

Oil traded near $91 a barrel as global fuel markets continued to tighten due to robust demand and supply curbs by top OPEC+ members. Brent crude edged higher, supported by diesel's rally after Russia planned to limit exports, pushing European futures past $1,000 a ton. Oil futures have risen approximately 25% since late June as global fuel demand reaches new highs.

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian equities exhibited mixed performance on Tuesday. The Australian ASX reversed an initially weak opening to post gains for the second consecutive day, while Japan’s primary indices were set to close higher. The Hang Seng also rebounded after a poor start, while mainland China stocks remained flat.

Country Garden, a Chinese property developer, has been granted additional debt repayment extensions for six out of eight onshore bonds, each extended by three years. The notional value of these bonds amounts to a total of CNY 10.8 billion ($1.48 billion).

The People’s Bank of China (PBOC) is expected to cut the Required Reserve Ratio (RRR) for the second time this year. This move comes after August credit data exceeded expectations, signaling signs of stability in the Chinese economy.

The recent 5-year Japanese Government Bond (JGB) auction showed relatively good demand, providing support for JGBs. The Ministry of Finance sold ¥2.5 trillion ($17 billion) of debt maturing in June 2028. Following Governor Ueda’s recent comments, the market appears to be more confident about the possibility of higher interest rates.

Australian consumer confidence continued to decline in September, despite the Reserve Bank of Australia (RBA) keeping the cash rate unchanged for a third consecutive month.

IPO underwriters for Arm are closing orders a day earlier than originally planned. The IPO is expected to be priced on Wednesday, likely at or above the initial range of $47 to $51 per share. Reports suggest that the offering has been oversubscribed by as much as 10 times, possibly reaching 15 times by Wednesday.

Alibaba’s CEO has stated that artificial intelligence (AI) is now a key priority in the group’s revamp plan, emphasizing the growing importance of AI in the company’s strategy.

Europe, Middle East, Africa:

European equity markets exhibited mixed results. The FTSE 100 outperformed other indices. Sectors such as retail, telecom, and insurance showed strength, while chemicals, technology, and real estate lagged.

In the UK, although unemployment increased, wage growth accelerated due to bonuses. Total average earnings, including bonuses, reached 8.5%, exceeding the consensus forecast of 8.2%. This has raised concerns for the Bank of England (BoE) as persistent wage growth contributes to inflation.

UK grocery inflation has decreased to its lowest level in a year as it entered September. Annual grocery inflation for the four weeks ending September 3rd was 12.2%, down from 12.7% in August.

Germany’s ZEW investor sentiment unexpectedly improved in September to -11.4, compared to -12.3 in the previous period. However, the current conditions index continued to weaken, reaching its lowest level in three years at -79.4, down from -71.3.

Eurozone ZEW investor sentiment came in worse than expected at -8.9, down from -5.5 in the previous month. The figure fell short of the expected level of -6.2.

The Americas:

Oracle reported fiscal Q1 revenue largely in line with expectations, but profitability and free cash flow (FCF) surpassed estimates. However, fiscal Q2 guidance for 5-7% revenue growth lagged behind the consensus of +8%, and EPS only met the higher end of the outlook range. The stock price dropped by nearly -10%, reflecting market sentiment.

Apple launched its new iPhone 15 models today, along with the Apple Watch Series 9. The company expects to introduce the first phones manufactured at its plant in India. Initial previews seemed positive regarding hardware upgrades, although there is debate about whether these upgrades are sufficient to drive sales at a time when consumer spending is slowing.

In negotiations with the Big Three US automakers (General Motors, Ford, and Stellantis), the United Auto Workers (UAW) has reduced its pay-increase demand. Recent proposals include a mid-30% wage increase, down from the initial demand of 40%+.

Bank of America’s latest Global Fund Manager Survey indicates that investor sentiment is no longer extremely bearish, with global equity allocations at a 17-month high.

The NFIB Small Business Optimism Index slipped to 91.3 in August from 91.9 in July, marking the 20th consecutive month below the 49-year average of 98.

Tesla received an upgrade from “equal-weight” to “overweight” at Morgan Stanley, with the move attributed to the opportunity presented by Tesla’s Dojo supercomputer initiative.

The Week Ahead:

Monday:

Tuesday:

Wednesday:

Manufacturing Production (YoY) (GB)

Industrial Production (MoM) (EA)

Consumer Price Index (MoM) (US)

Thursday:

Employment Change s.a (AU)

Retail Sales (MoM) (US)

Friday:

Industrial Production (YoY) (CN)

NY Empire State Manufacturing Index (US)

Industrial Production (MoM) (US)

Michigan Consumer Sentiment Index (US)

Investment Tip of The Day

Asset Allocation Reassessment for Optimal Portfolios: Periodically reassessing your portfolio's asset allocation is crucial to align it with your financial goals and risk tolerance.

Meme of the Day