Trading Tuesday

Ranora Daily - Your daily source for reliable market analysis and news.

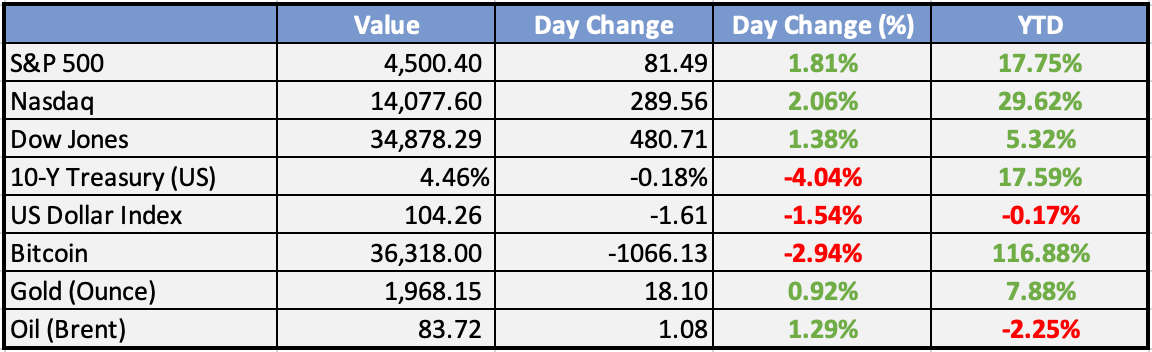

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Naira slump persists despite 46% rise in dollar turnover - Punch

The amount of dollars traded on the Investor & Exporter forex window rose by 46.69 per cent to $123.25m on Monday.

Nigeria’s non-oil income outpaces oil by N1.5trn in one year - Businessday

Nigeria’s non-oil revenue surpassed oil revenue in twelve months, marking the third time this has occurred since the oil boom in 1973.

Global

Oil climbs as IEA lifts demand growth forecast - Reuters

Oil prices rose as the International Energy Agency (IEA) increased its demand growth forecasts, with Brent crude gaining 0.2% to $82.72 a barrel, and U.S. WTI crude climbing 0.3% to $78.47. The IEA raised its 2023 growth forecast to 2.4 million barrels per day (bpd) from 2.3 million bpd and increased the 2024 forecast to 930,000 bpd from 880,000 bpd.

Futures Edge Up Ahead of Inflation Data - WSJ

The focus is on inflation as the U.S. consumer-price index for October is expected to show a rise of 3.3%, or 4.1% on a core basis. Investors will closely scrutinize the data for its implications on future interest-rate policy. Stock futures inched up ahead of the release. In Asia, Korea’s Kospi Composite rose over 1%, while moves were muted in Hong Kong and Tokyo

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian equities ended mostly higher, with Japan leading the gainers.

Mainland China markets also performed well, while Hong Kong closed slightly lower.

Corporate action boosted Kospi, and Taiex saw gains.

Southeast Asia experienced some losses, and India's market was closed for a holiday.

News of a 1 trillion Yuan (~$137B) stimulus for the housing market in China is making headlines.

PBOC plans to inject cheap funds through banks, with the money trickling down to households for home purchases, possibly this month.

Last month, China announced a 1 trillion Yuan package in additional sovereign debt, providing an early boost to markets.

Speculation of intervention briefly strengthened the Yen during US market hours.

Europe, Middle East, Africa:

European equity markets were higher, led by the DAX, while the UK’s FTSE lagged after mixed wage data.

UK Wage Data showed a decline in overall wages, but total wages exceeded consensus.

Average pay, including bonuses, was 7.9% YoY, higher than the consensus of 7.4%.

Basic pay came in at 7.7% vs. 7.9% last month. 54k jobs were created, and the unemployment rate remained stable at 4.2%.

Euro Area GDP growth's second reading was unchanged at -0.1%.

ZEW Sentiment data for the Euro Area and Germany surpassed expectations.

Euro Area Sentiment was 13.8 vs. 2.3 last month, and Germany’s reading was 9.8 vs. -1.1.

The Americas:

In Argentina, the Inflation Rate increased to 142.7% in October from 138.3% in September.

Bank of Mexico Gov Rodriguez suggested potential rate cuts due to an easing inflation outlook.

NFIB Small Business Optimism Index in the US edged down to 90.7 in October, the lowest since May.

22% of owners reported inflation as their top concern, and 43% reported hard-to-fill job openings.

Home Depot beat expectations, reporting in-line revenues; FY24 EPS guidance in-line, but revenues below consensus.

Same-store sales were down -3.1%, slightly better than expected, and customer transactions were down -2.4% YoY.

The Week Ahead:

Monday:

Tuesday:

Core CPI m/m (US)

Eurozone's GDP declines by 0.1% in Q3

Wednesday:

CPI y/y (UK)

Core PPI m/m (US)

Core Retail Sales m/m (US)

Empire State Manufacturing Index (US)

Thursday:

Unemployment Claims (US)

Friday:

Retail Sales m/m (UK)

Investment Tip of The Day

Watch for Currency Pegs: In international investments, be cautious of currency pegs, where a country's currency is tied to another currency or a fixed rate. Sudden changes in pegs can disrupt investments.

Meme of the Day