Trading Tuesday

Ranora Daily - Your daily source for reliable market analysis and news.

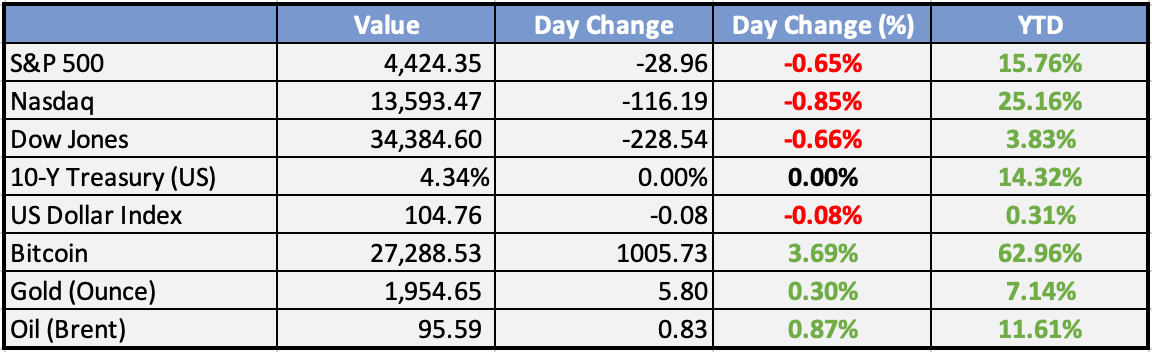

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Dangote Refinery to start refining petrol by November 30, 2023 – Report - Naira Metrics

Dangote Refinery is set to begin refining petrol by November 30, 2023. This development is expected to help Nigeria reduce its dependence on imported petroleum products, thereby improving the country's energy security and potentially reducing fuel prices. The refinery, once fully operational, is expected to have a significant impact on Nigeria's oil and gas industry.

Crude oil price hits $95 per barrel, the highest so far in 2023 - Naira Metrics

The price of crude oil has surged to $95 per barrel, driven by concerns over supply disruptions and geopolitical tensions in key oil-producing regions. This increase in oil prices could lead to higher fuel and energy costs, impacting consumers and businesses worldwide.

Management staff with less than 15 months to statutory retirement will exit company today – NNPCL - Naira Metrics

The Nigerian National Petroleum Corporation Limited (NNPCL) has announced that management staff with less than 15 months left until their statutory retirement will exit the company today. This move is part of the organization's restructuring efforts and is expected to affect several senior employees.

Global

Global Economy Poised to Slow as Rate Hikes Bite, OECD Says - Bloomberg

The global economy is set for a slowdown to 2.7% in 2024, with risks tilted to the downside, the OECD warned on Tuesday. The slowdown is due to a combination of factors, including interest-rate increases, China's pandemic rebound, and high inflation. The OECD urged central banks to remain restrictive until there are clear signs that inflation pressures have abated.

Euro zone Aug inflation revised slightly down - Reuters

Euro zone consumer inflation in August was slightly lower than initially estimated, at 5.2% year-on-year, but still more than twice the European Central Bank's target. The ECB raised its deposit rate to a record high 4% last week and hinted at a pause, raising expectations that its next move will be a cut, possibly as soon as late spring 2024.

Weekly Investment Watchlist

Market Commentary:

Asia and Australia:

Asian equities mostly closed lower in a quiet session. Hong Kong saw a rebound after a weak opening but still remained below recent support levels. Mainland markets were slightly lower. Australia, South Korea, and Taiwan all finished in the red, while Southeast Asian markets showed mixed results. Japan’s Topix remained flat, while the Nikkei closed lower. India’s market was closed for a holiday.

China announced its Loan Prime Rate, with market attention focused on whether they would take stronger action compared to the previous month when they cut rates by 10bps on the 1-year but not the 5-year. Rate cuts can put pressure on the currency, and China must balance this concern. The recent strength of the currency might allow for a larger cut.

Chinese developer Country Garden won bondholder approval for the last of a batch of eight onshore notes for repayment extensions. This development suggests that the Chinese property market has temporarily avoided a crisis.

RBA meeting minutes revealed that central bank members in Australia remain concerned about inflation both domestically and globally. However, they decided not to raise rates in September because inflation was still tracking their projections. Governor Lowe’s last meeting was also mentioned, although no specific details were provided.

Europe, Middle East, Africa:

European equity markets were firmer after rebounding from earlier lows. Financials advanced due to marginally higher yields, and the Energy Sector received a boost from a surge in Brent oil prices. However, the Retail sector continued to face pressure.

The OECD published its interim growth outlook, with Eurozone growth projections revised downward by 0.3% to 0.6% for this year and by 0.4% to 1.1% for 2024. Germany and Italy also saw reductions in growth projections for 2023 and 2024, respectively. The UK’s growth is expected to remain steady at 0.3% for this year but was revised down by 0.2% to 0.8% for 2024.

The ECB witnessed debate over whether it should pause or even cut rates going into 2024. Some members expressed concerns about the Eurozone economy’s sensitivity to rate increases and energy costs. With energy costs expected to remain high, inflation could rise, and economic growth might slow further. While there are hawks who advocate for one more rate hike, the ECB is at a point where a policy mistake could be made, given concerns about economic growth.

The Americas:

Data on the housing market showed signs of easing, with the NAHB/Wells Fargo Housing Market Index declining from 50 to 45. Higher mortgage rates appear to be weighing on the market, particularly for single-family homes.

Treasury Department data indicated that foreign holdings of US Treasuries increased for a second consecutive month in July, rising to $7.655 trillion from $7.562 trillion in the previous month. However, attention focused on China’s holdings, which fell to $821.8 billion, marking the lowest level since May 2009 and continuing a general downtrend over the past year.

There was no significant progress in government funding negotiations. House Speaker McCarthy faced opposition from within his own party for his proposal for a short-term spending patch, and a strike against Detroit automakers continued, with the UAW saying that targeted stoppages could expand if there is no “serious progress” by noon Friday.

The Week Ahead:

Monday:

Tuesday:

Harmonized Index of Consumer Prices (MoM) (EA)

Wednesday:

PBoC Interest Rate Decision (CN)

Consumer Price Index (YoY) (GB)

Fed Interest Rate Decision (US)

FOMC Press Conference (US)

Thursday:

Bank of England Minutes (GB)

Initial Jobless Claims (US)

Existing Home Sales Change (MoM) (US)

Friday:

GfK Consumer Confidence (GB)

Retail Sales (MoM) (GB)

HCOB Composite PMI (EA)

S&P Global Services PMI (US)

Investment Tip of The Day

Avoid Overconcentration: Diversification is a fundamental risk management principle. Avoid overconcentration in a single stock, sector, or asset class. Spreading your investments across a range of assets reduces the impact of a poor-performing investment on your overall portfolio and enhances risk mitigation.

Meme of the Day