Wealth Wednesday

Ranora Daily - Your daily source for reliable market analysis and news.

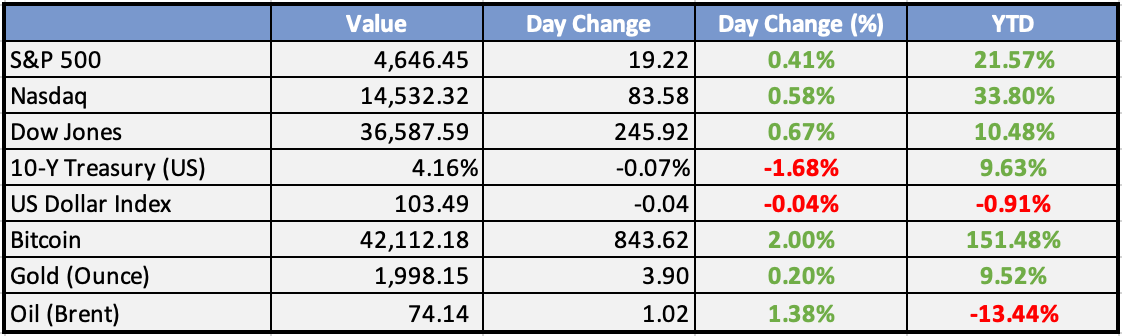

Market Data

Local

Global

x*Data as of 4pm WAT

Market News

Local

Nigerian govt to sell a 40% stake in Eleme petrochemicals, DisCos - BPE - Daily Post

The Bureau of Public Enterprises, BPE, is to raise money for the Federal Government to partially finance the 2024 budget by selling government’s stake in Eleme Petrochemicals Company Limited (EPCL), Electricity Distribution Companies, and two other public enterprises.

Global

Inflation slowed to a 3.1% annual rate in November - CNBC

US inflation ticked up slightly in November, but largely in line with expectations. The CPI increased 0.1% monthly and 3.1% annually, while core CPI rose 0.3% and 4% respectively. Energy prices fell, but food and shelter kept inflation elevated. The Fed is expected to hold rates steady but signal a pause in tightening.

Citadel is handling back about $7B in profits to clients - WSJ

Citadel's flagship fund returned nearly 15% in 2023 and plans to return $7 billion to investors, bringing its AUM to $58 billion. Their success is attributed to their multimanager platform, where teams independently trade within risk parameters. This model provides steady returns but can underperform in strong markets.

Global Market Commentary

Overview

Currencies and bond yields experienced fluctuations driven by a decline in UK wages growth, followed by a small upside surprise in US inflation. The AUD showed slight softening at 0.6560. Notable events on today’s agenda include Australia’s mid-year budget update, Japan’s Q4 Tankan business survey, and the global highlight, the FOMC decision, forecasts, and press conference.

Currencies/Macro:

The US dollar displayed mixed performance against G10 currencies amid market consolidation.

EUR/USD rose 0.3% to 1.0795, while GBP/USD gyrated before steadying little changed at 1.2565.

US November headline CPI edged up 0.1%m/m to an expected 3.1%y/y with core CPI +0.3%m/m to 4.0%.

UK labor data showed caution-worthy results as the survey underwent remodeling.

German and Eurozone ZEW surveys for December indicated an uptick in business expectations.

Interest Rates:

The US 2yr treasury yield remained little changed at 4.715%, and 10yr yields tested 4.14% but ended -3bps at 4.20%.

Markets showed no pricing for moves in the upcoming FOMC meetings.

Australian 3yr government bond yields remained +3bps, implying 3.93%, while 10yr yields were -2bps to 4.32%.

Credit spreads retained recent momentum, with Main half a bp better at 66.5, CDX heading to new YTD lows at 60.5.

Commodities:

Crude prices slumped to fresh lows due to increased EIA crude forecasts for 2023 and rising Russian exports.

Metals exhibited mixed performance, with copper unchanged at $8,342, nickel falling 0.8% to $16,475, and zinc rising 0.9% to $2,428.

Iron ore softened post Politburo and economic work meetings.

Day Ahead:

Eurozone:

October’s industrial production print is likely to reveal persistent weakness in demand.

US:

The FOMC is expected to maintain the funds rate at 5.25-5.50%, with a focus on quarterly forecasts and press conference guidance. Attention will be on inflation forecasts and the ‘dot plot’ of funds rate projections. Upstream price pressures measured by the US PPI are expected to moderate further in November ahead of the FOMC meeting.

The Week Ahead:

Monday:

Tuesday:

Core CPI m/m (US)

Wednesday:

UK GDP fell by 0.3% in October

Core PPI m/m (US)

Federal Funds Rate (US)

FOMC Economic Projections (US)

Thursday:

Official Bank Rate (UK)

Main Refinancing Rate (EU)

Core Retail Sales m/m (US)

Unemployment Claims (US)

Friday:

Flash Manufacturing PMI (UK)

Flash Services PMI (UK)

Empire State Manufacturing Index (US)

Flash Manufacturing PMI (US)

Flash Services PMI (US)

Investment Tip of The Day

Monitor Intellectual Property Protection: For technology and innovation-focused investments, assess how well companies protect their intellectual property. Legal disputes or breaches can pose risks to future earnings.

Service Spotlight of the week - Technology Solutions

Meme of the Day