Wealth Wednesday

Ranora Daily - Your daily source for reliable market analysis and news.

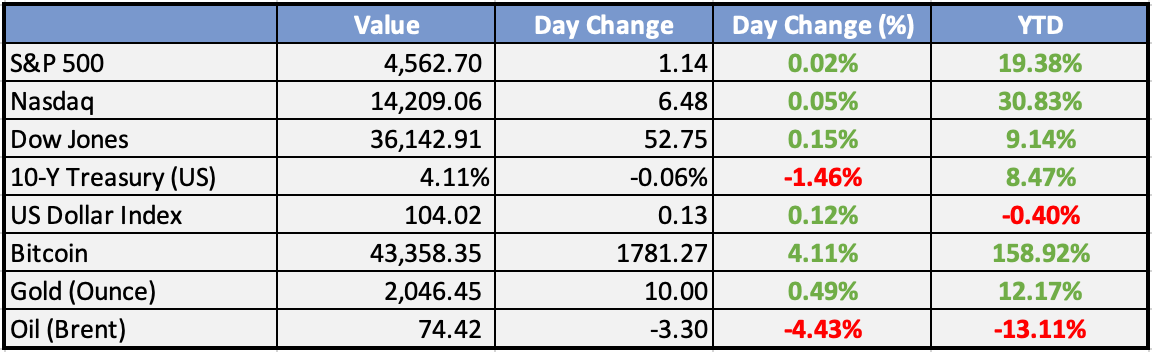

Market Data

Local

Global

x*Data as of 4pm WAT

Market News

Local

NCDMB Proposes 3 New Modular Refineries In 2024 - Leadership News

The Nigeria Content Development and Monitoring Board (NCDMB) has revealed that three more Modular refineries will start operation in the country by 2024.

Auction: Presidential aircraft bidders get December 24 deadline - Punch

Bidders for the Falcon 900B aircraft, a prominent member of the presidential air fleet, which has been put on sale by Nigeria Air Force, have until December 24 to submit their applications.

Power, finance ministries get N618bn multilateral loan, CSOs kick - Punch

CSOs and power consumer groups have expressed concern over the N618bn multilateral and bilateral loans allocated to the Ministries of Finance and Power in the 2024 budget.

Port Harcourt Refinery Ready This December, NNPC Insists - This day

The Nigerian National Petroleum Company Limited (NNPC), has maintained that the Port Harcourt Refining Company (PHRC) will start operations this December despite pessimism expressed by many Nigerians.

Global

Apple’s market cap closes above $3T - CNBC

Apple's stock price climbed 2% on Tuesday, pushing the company's market capitalization back above $3 trillion for the first time since August. The iPhone maker's stock price has risen over 48% so far this year, despite slowing growth and problems in markets such as China. Apple's fiscal 2023 revenue was down about 3% from the prior year.

US job openings hit more than 2-1/2-year low as labor market cools - Reuters

The number of job openings in the US fell to 8.733 million in October, the lowest level since March 2021. This is the strongest sign yet that higher interest rates are dampening demand for workers. The decline in vacancies was in all four regions, with steeper decreases in the South and Midwest. Hiring also slipped, but the quits rate was unchanged at 2.3%.

US Mortgage Rate Drops to Four-Month Low, Boosting Refinancing - Bloomberg

US mortgage rates fell to the lowest level in almost four months last week, spurring the biggest demand for refinancing since February. Mortgage rates have retreated on expectations that the Federal Reserve is not only done raising interest rates, but may start cutting them early next year. Refinancing activity jumped nearly 14%, the most since February.

Global Market Commentary

Overview

US bond yields saw a decline influenced by the softness in October job openings, despite the resilience of the November services ISM. Dovish comments from the ECB impacted Eurozone bond yields. Notable upcoming events include the Bank of Canada’s policy decision and the disclosure of US November ADP private payrolls.

Currencies/Macro:

The US dollar was flat against JPY but rose against other G10 currencies.

EUR/USD fell to 1.0780 (-0.4%), GBP slipped to 1.2590 (-0.3%), and USD/JPY reached 146.57.

Global Dairy Trade Auction saw a +2.1% rise in whole milk powder prices.

US November ISM Services Index rose to 52.7, with the employment component at 50.7.

US October JOLTS report showed a surprise slide in job openings to 8.733mn.

ECB’s Isabel Schnabel’s comments made a further rate increase unlikely.

Eurozone services PMI increased to 48.7, helping Composite PMI to 47.6.

ECB’s Consumer Expectations Survey showed unchanged inflation expectations.

UK final November Services PMI firmed to 50.9, allowing Composite PMI to tick up to 50.7.

Interest Rates:

US 2yr treasury yield slipped -5bps to 4.58%, 10yr yields declined -8.5bps to 4.17%.

Fed funds rate priced to remain unchanged; March 2024 cut probability approached 75%.

December 2024 Fed pricing at -130bps or 4.03%.

UK 10-year gilt yield fell -17bp to 4.02%, German bund -11bp to 2.24%.

Credit Spreads:

Main and CDX credit spreads are little changed; US IG cash is flat to a bp wider.

December is expected to be slower for supply; deals continue to be printed.

Commodities:

Crude markets weakened after Saudi Arabia cut prices; WTI at $72.32, and Brent at $77.18.

Gas prices in Europe fell due to congestion in the Panama Canal.

Metals under pressure; copper down 1.2% at $8,341, zinc down 1.4% at $2,418.

Iron ore prices unaffected by Moody’s; January SGX contract at $129.00.

Day Ahead:

Eurozone: October retail sales expected to reflect broad-based weakness.

US: November ADP private payrolls change likely to show a softening labor market.

The Week Ahead:

Monday:

Tuesday:

US ISM Services PMI is at a current level of 52.70, up from 51.80 last month

US JOLTS Job Openings fall to 8.7 million in October vs. 9.3 million forecast

Wednesday:

US ADP Non-Farm Employment increased by 103,000 jobs in November and annual pay was up 5.6 percent YoY

Thursday:

Unemployment Claims (US)

Friday:

Average Hourly Earnings m/m (US)

Non-Farm Employment Change (US)

Unemployment Rate (US)

Prelim UoM Consumer Sentiment (US)

Investment Tip of The Day

Monitor Short Interest Levels: High levels of short interest in a stock may indicate potential risks. Stay informed about short interest trends as they can impact stock prices and market sentiment.

Service Spotlight of the week - Wealth Management

Meme of the Day