Wealth Wednesday

Ranora Daily - Your daily source for reliable market analysis and news.

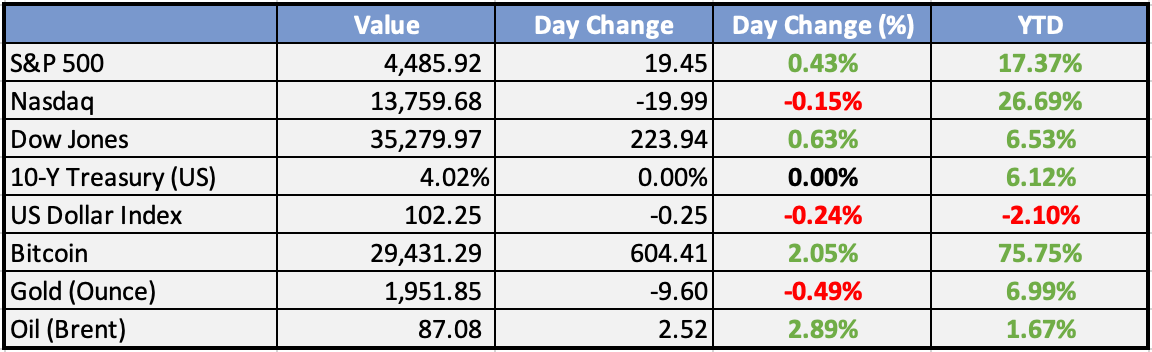

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Tinubu Vows to End Nigeria’s Overreliance on Borrowing for Public Expenditure - This Day

President Tinubu launches the Fiscal Policy and Tax Reforms Committee to reduce borrowing reliance, improve revenue, and achieve an 18% tax-to-GDP ratio in three years. The committee, led by Taiwo Oyedele, aims to enhance fiscal governance, tax reforms, and growth facilitation.

Global

US bank shares drop as Moody’s cuts ratings, warns on risks - Bloomberg

Moody's Investors Service downgraded the credit ratings of 10 US banks on Tuesday, citing rising risks in the industry. The downgrades affected banks of all sizes, including Bank of America, Citigroup, and Wells Fargo. Moody's said that the banks are facing increasing pressure from rising inflation, a potential recession, and the war in Ukraine.

Chinese economy falls into deflation for first time since February 2021 - Financial Times

China's economy enters deflation as consumer prices fall by 0.3% YoY in July, the first decline since February 2021. Producer prices also drop by 4.4%. Stagnating growth, weak trade, and a struggling real estate sector contribute to the deflationary trend, prompting potential fiscal stimulus considerations.

Rates on savings accounts are higher than millions of mortgages - Bloomberg

Millions of Americans experience higher interest on their savings accounts (4.3%) than their mortgage rates (below 4.375%). After Fed rate hikes, borrowing costs for homes surged, causing a shortage due to reluctance to move. High-yield accounts, including Marcus, Barclays, and Capital One, benefit from higher rates. Fed's future hikes are tied to economic data.

Goldman Sachs’ John Rogers steps down as chief of staff - Financial Times

Goldman Sachs' John Rogers steps down as chief of staff, staying as EVP and board secretary. Russell Horwitz, returning after 2020 departure, takes over. Amid challenges and departures, CEO David Solomon faces maintaining momentum.

Weekly Investment Watchlist

Market Commentary

Asia and Australia:

Asian equities had a mixed performance on Wednesday. The Nikkei underperformed due to negative market reactions to post-close earnings from the previous day. Hong Kong traded higher, while Mainland China markets posted losses for the third consecutive day.

The offshore yuan rebounded from a three-week low against the dollar, attributed to a much stronger-than-expected fixing of the daily midpoint.

Country Garden faced mounting troubles as it missed an offshore bond interest payment.

TSMC announced plans to build an $11 billion chip manufacturing plant in Germany.

The US plan to restrict investment in China is likely to target Chinese firms earning at least half their revenue from cutting-edge sectors such as quantum computing and AI.

South Korea’s unemployment rate rose to a six-month high.

Europe, Middle East, Africa:

European equity markets traded higher and were near their best levels. Banks rallied as the Italian government eased market fears surrounding a surprise bank tax. Energy and mining sectors also advanced, while travel/leisure and healthcare lagged.

Economists warned that the Bank of England’s rate rises risk tipping Britain into a recession.

Germany’s property sector is in a slump due to various factors, including rising interest rates, soaring building costs, and the Ukraine war.

The primary gauge of long-term Eurozone price pressures climbed well above the ECB target, reaching 2.66%.

The Americas:

US banks suffered around $19 billion in loan losses as borrowers felt the pain of rate rises.

The Treasury auctions got off to a positive start, with the 3-year note sale producing a lower-than-expected yield.

KKR purchased prime auto loans as regional lenders sold assets to improve liquidity.

WeWork stated that there is “substantial doubt” about its ability to continue operating.

A US judge rejected Google’s proposal to dismiss a $5 billion privacy lawsuit filed against the company.

Hedge funds closed their underperformance after bailing on record short positions, resulting in positioning that is now the most bullish since December 2021.

The Week Ahead:

Monday:

Tuesday:

US consumer credit report rose: +$17.84b; est +$13.55b.

US July jobs report non-farm payrolls expanded 187k, unemployment is 3.5%; est: 3.6%.

Wednesday:

Consumer Price Index (China)

Thursday:

Consumer Price Index (US)

Economic Bulleting (EA)

Monthly Budget Statement (US)

Friday:

Gross Domestic Product (US)

Consumer Price Index (France)

Producer Price Index ex. Food & Energy (US)

Michigan Consumer Sentiment Index (US)

Investment Tip of The Day

Stay informed about macroeconomic indicators, including GDP growth, inflation rates, and unemployment figures, to understand the broader economic landscape. Analyze how these indicators can impact different sectors and make informed investment decisions.

Meme of the Day