Wealth Wednesday

Ranora Daily - Your daily source for reliable market analysis and news.

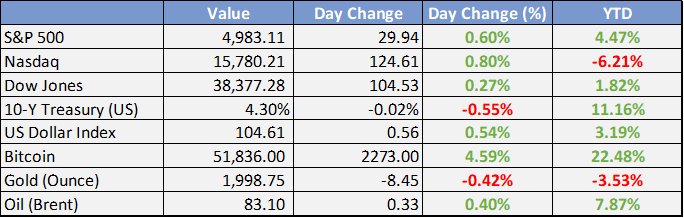

Market Data

Local

Global

*Data as of 4pm WAT

Market News

Local

Banking Credit To Economy Rises By 44% To N96.2trn - Leadership

Total credit to the Nigerian economy as at Dec’23 by the banking industry rose by 44.8% yoy to N96.2 trillion according to latest credit data made available by the Central Bank of Nigeria(CBN). According to the Money and Credit Statistics of the CBN, lending to both the government and the private sector rose from N66.398 trillion in Dec’22 to N92.188 trillion at the end of Dec’23.

FG, W’Bank plan $3bn broadband infrastructure fund - Punch

The Federal Government and the World Bank are planning to invest $3bn on an additional 120,000km of fibre optic cables to improve broadband infrastructure and connectivity in the country. The Minister of Communications, Innovations and Digital Economy, Bosun Tijani disclosed during a stakeholders’ engagement themed ‘broadband for all’.

Access Holding appoints Ms Bolaji Agreed as acting Group CEO - BNR

The Board of Directors of Access Holdings Plc (‘the Company’) has announced the appointment of Ms. Bolaji Agbede as the Acting Group Chief Executive Officer of the Company following the unfortunate demise of its former Group Chief Executive Officer, Dr. Herbert Wigwe, on February 9, 2024. The appointment is subject to the approval of the Central Bank of Nigeria.

Nigeria, UK sign new Trade Agreement - Premium Times

Nigeria and the UK on Tuesday signed a new trade agreement to boost trade and investment between both countries. Called the Enhanced Trade and Investment Partnership (ETIP), the agreement is also expected to also unlock new opportunities for UK and Nigerian businesses.

Crude rises to $83 as Nigeria’s output crosses 1.4mbpd - Punch

Brent, the global benchmark for crude, rose to $83.19/barrel on Tuesday evening, moving up by $1.19 when compared to its cost the preceding day, as latest data from the Federal Government indicated that Nigeria’s oil output increased to 1,426,574 barrels/day in January 2024.

Global

US Senate Passes $95.3 Billion Ukraine, Israel Aid Package - WSJ

The Senate passed a $95.3 billion package backed by President Biden that contains a fresh round of aid for Ukraine and funds for Israel and Taiwan, overcoming Republican objections but facing an uncertain future in the GOP-run House.

Market Commentary:

Currencies/Macro:

Following the release of CPI data, the US dollar strengthened significantly against all G10 currencies. The EUR/USD pair dropped from 1.0795 to 1.0710, hitting a three-month low. The GBP/USD decreased by 0.3% for the day to 1.2590, with the sterling showing relative strength. The USD/JPY surged from 149.30 before the CPI announcement to 150.80, marking its first time above 150 since November 17.

The US CPI for January indicated a month-over-month increase of 0.3% and a year-over-year rise of 3.1%, surpassing estimates which predicted a 0.2% monthly and 2.9% yearly increase. The core CPI, excluding food and energy, climbed by 0.4% month-over-month and 3.9% year-over-year, slightly above the expected increases. Significant movements were noted in the shelter component, with a monthly increase of 0.6%, and in vehicle insurance, which rose by 1.4% month-over-month.

The January NFIB small business sentiment index declined to 89.9, below both the expected 92.3 and the previous 91.9, with most components showing a downturn.

In the UK, labor data for December was unexpectedly strong. The unemployment rate decreased to 3.8%, better than the anticipated 4.0%. Employment increased by 72k, surpassing the forecast of 50k, and average weekly earnings grew by 5.8% year-over-year, higher than the expected 5.6%. Additionally, January payrolls saw an increase of 48k, defying expectations of a decrease and revising the previous figure to a more positive outcome.

Interest Rates:

After the release of US CPI data, the yield on the US 2-year treasury surged from 4.45% to 4.66%, and the yield on the 10-year treasury increased from 4.15% to 4.31%. Market expectations for the Federal Reserve's funds rate, which is currently at 5.375%, anticipate no change at the upcoming March meeting, but there's now a unanimous expectation of a rate cut by June.

This uncertainty also affected the credit markets, leading to a slight widening, with the Main index moving out by a basis point to 58 and the CDX index widening by 2 basis points to 55.5. The release of the CPI data also abruptly dampened the primary market's activity, with reports indicating that three potential issuers withdrew their plans immediately after the data was published.

Commodities:

Optimistic OPEC demand forecasts buoyed crude oil markets, with the March West Texas Intermediate (WTI) contract increasing by 1.5% to $78.07 and the April Brent contract rising by 1.1% to $82.94, despite higher-than-anticipated US CPI data and a rise in US yields and the dollar. OPEC predicts a global oil demand increase of 2.3 million barrels per day (mbpd) this year, following a 2.4 mbpd rise last year. The majority of this demand is expected to come from non-OECD countries, with significant contributions from China, India, other Asian regions, and the Middle East. These OPEC projections are more optimistic than those of the International Energy Agency (IEA), with IEA Director Fatih Birol forecasting a more moderate increase in world oil consumption of between 1.2 to 1.3 mbpd in 2024, citing a slowdown in global growth. Additionally, US sanctions have impacted Russian crude oil tanker operations, with a notable portion of the fleet sanctioned by the US treasury on October 10 showing a decrease in activity. Gasoline margins in northwest Europe reached a peak not seen since last September, with the premium for the Eurobob oxy gasoline contract over Brent at its strongest for this period since at least 2010.

In the metals market, a stronger US dollar and unexpected CPI data led to declines, with copper dropping 0.3% to $8,209 and zinc falling 0.5% to $2,308. However, nickel saw a 1.6% increase to $16,300 amid news of industry consolidation. Peru reported a 1.3% year-on-year increase in copper production for December, culminating in a 12.7% rise for 2023 compared to 2022.

Iron ore trading was muted due to the Chinese holiday, with the March Singapore Exchange (SGX) contract decreasing by 40 cents to $128.15. RBC anticipates iron ore prices to be supported in the first half of 2024, driven by increased blast furnace utilization after the Lunar New Year holidays, seasonally low shipment volumes, and reduced stockpile levels.

Investment Tip of The Day

Regularly reviewing and rebalancing your portfolio ensures your investment allocations remain aligned with your financial goals and risk tolerance. This process involves selling overperforming assets and buying underperforming ones to maintain a desired asset allocation. This discipline helps in managing risk and can contribute to better long-term investment outcomes.