Weekly Roundup: Bills, Banks, and the Return of Foreign-Flow Optionality

Ranora Market Outlook - This week showed that Nigerian assets are still being priced around yield, liquidity, and credibility, while global markets remain sensitive to oil and Fed risk.

Opening View

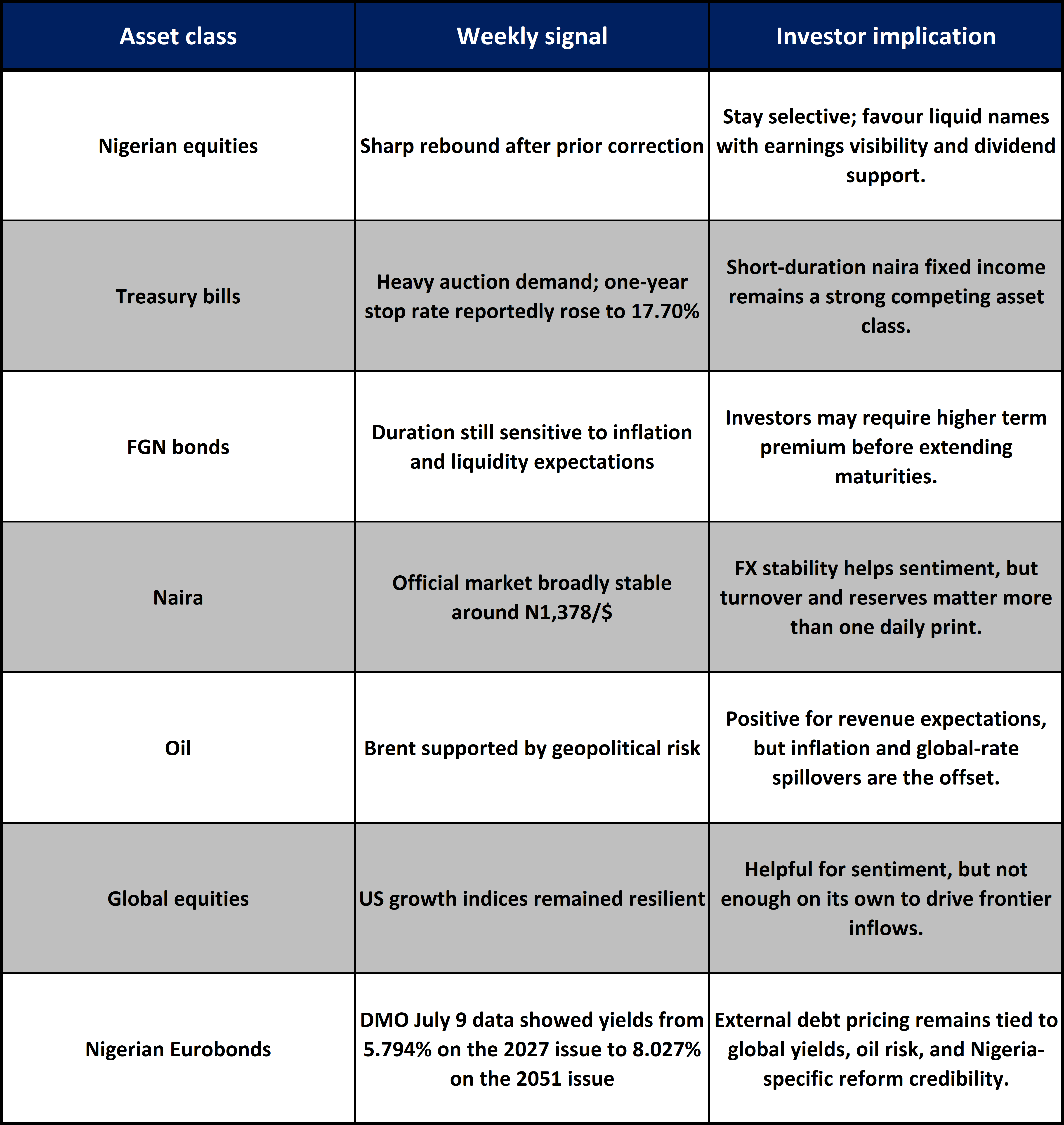

Nigerian markets ended the week with a more constructive tone than the prior selloff suggested. The NGX All-Share Index recovered strongly from the previous week’s close, while the July 8 Treasury bills auction confirmed that domestic liquidity is still looking for a home in high-yield, short-duration instruments. That matters because the equity rebound and the fixed-income bid are not separate stories. They both point to the same market condition: cash is available, but investors are still demanding either visible earnings momentum or attractive risk-free yield.

The bigger strategic signal came from S&P Dow Jones Indices placing Nigeria on its 2027 watchlist for possible reclassification from Standalone to Frontier Market. This is not an immediate upgrade, but it gives investors a fresh reason to track reforms, market access, FX liquidity, and settlement infrastructure more closely.

Globally, the week was shaped by oil risk and the Federal Reserve. Brent remained supported by Middle East supply concerns, while Fed minutes showed policymakers still worried about inflation. For Nigeria, that mix is double-edged: stronger oil can help external balances, but higher global yields can reduce foreign appetite for frontier risk.

The Big Picture:

The week’s main lesson is that liquidity is back, but selectivity is still doing the work.

In equities, the NGX rebound suggests investors are willing to re-enter after the correction, especially where earnings, dividends, or index weight justify positioning. The All-Share Index moved from 229,240.34 at the July 3 weekly close to about 243,954.45 on July 10, a roughly 6.4% weekly recovery.

In fixed income, demand for Treasury bills remained deep. CBN allotted about N1.06 trillion at the July 8 auction against an offer of N700 billion, while the one-year stop rate reportedly rose to 17.70% from 17.34% at the June 17 auction. That keeps short-duration naira assets attractive for investors who want yield without taking long bond duration risk.

The global backdrop is not risk-free. Fed minutes released July 8 showed all participants supported holding rates at the June meeting, but a few saw a case for a hike, and participants still judged inflation risks as tilted upward.

Nigeria Market Intelligence

NGX recovered, but the rebound still needs earnings confirmation.

What happened: Nigerian equities rebounded sharply after the previous week’s 1.21% decline.

Why it mattered: A strong bounce after a selloff shows liquidity has not left the market, but it also raises the bar for earnings delivery.

What to watch next:ank earnings, dividend expectations, and whether the rebound broadens beyond large liquid names.

Treasury bills remain the anchor for naira portfolios.

What happened: The July 8 auction drew heavy demand, with reported subscriptions of about N2.03 trillion versus N700 billion offered.

Why it mattered: Strong demand at high yields keeps short-duration fixed income competitive against equities.

What to watch next: Whether CBN continues to absorb liquidity without pushing stop rates too sharply higher.

Nigeria’s S&P DJI watchlist placement is a credibility signal, not a capital-flow event yet.

What happened: S&P Dow Jones Indices placed Nigeria on its 2027 Country Classification Watchlist for possible reclassification from Standalone to Frontier Market.

Why it mattered: If reforms hold, Nigeria could regain visibility for benchmark-sensitive frontier investors.

What to watch next: FX access, market liquidity, settlement resilience, policy consistency, and foreign investor repatriation experience.

The naira was broadly stable in the official market, but not yet a settled story.

What happened: CBN’s NFEM data for July 9 showed an official rate around N1,378 per US dollar, with the closing rate at N1,379.25.

Why it mattered: Stability supports investor confidence, but the test is whether dollar liquidity remains adequate as import and portfolio-flow demand changes.

What to watch next: NFEM turnover, external reserves, and the parallel-market spread.

Global Market Intelligence:

The Fed is still a source of yield pressure.

What happened: Fed minutes showed inflation remained elevated and upside risks were still prominent.

Why it mattered: Higher-for-longer US yields can reduce the relative appeal of frontier-market risk unless local yields and FX stability compensate investors.

What to watch next: US June CPI, scheduled for July 14.

Oil risk stayed central to the global macro story.

What happened: Brent was heading for a weekly gain, with Middle East supply risk still influencing prices.

Why it mattered: For Nigeria, higher Brent can support oil revenue and reserves, but persistent geopolitical risk can also keep global inflation and yields elevated.

What to watch next: Strait of Hormuz flows, OPEC/IEA updates, and Nigeria’s production levels.

US equities held up, led by growth sentiment.

What happened: As of Thursday’s close, the S and P 500 was up 0.8% for the week and the Nasdaq was up 1.4%, while the Dow was down 0.8%.

Why it mattered: Strong US risk appetite can help global sentiment, but if it is driven by AI optimism while yields rise, frontier markets may not receive the same benefit.

What to watch next: Whether earnings justify valuations as inflation data arrives.

Asset Class Implications:

Ranora View:

This week strengthened the case for a barbell approach in Nigerian portfolios: maintain exposure to short-duration fixed income for yield and liquidity, while keeping selective equity exposure in sectors where earnings can defend valuations. The Treasury-bill auction confirms that naira liquidity is still being pulled toward high nominal yield. That makes broad, indiscriminate equity buying harder to justify.

The more interesting medium-term story is Nigeria’s possible path back into frontier-market visibility. The S&P DJI watchlist decision will not bring passive flows immediately, but it raises the value of policy consistency. If FX access improves, market infrastructure remains reliable, and corporate earnings hold up, Nigeria could become easier for foreign allocators to re-underwrite. Until then, investors should treat the watchlist as an option on future flows, not as current liquidity.

What to Watch Next:

US June CPI on July 14 and the impact on Treasury yields.

Nigeria’s next inflation print and whether food inflation continues to pressure real returns.

CBN liquidity operations after the large Treasury-bill allotment.

NGX breadth: whether the rebound expands beyond large-cap and financial names.

Official FX turnover and any widening between official and parallel-market rates.

Question of the day:

Is the stronger opportunity in Nigerian markets now in locking in short duration yield, or in selectively buying equities after the correction?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.