Weekly Roundup: Growth Improves, But Liquidity, Power and Oil Still Set the Market Tone

Ranora Market Outlook -Nigeria’s Q1 growth print strengthened the macro story, but investors still need to watch inflation, power-sector stress, oil-price volatility and global risk appetite.

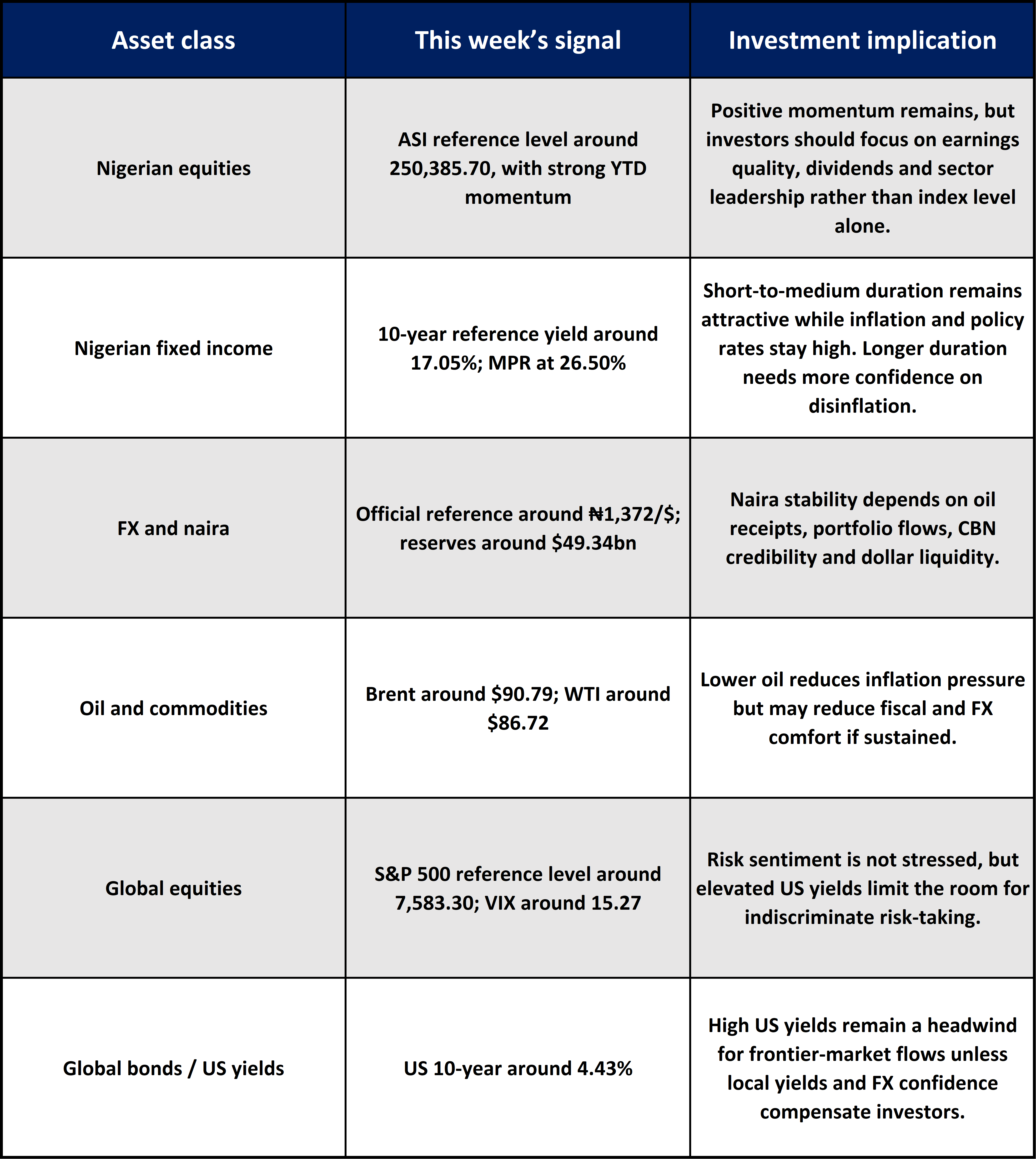

The Week in One Paragraph

Nigeria ended the week with a stronger growth signal but not a simpler investment environment. The Q1 2026 GDP print of 3.89% year-on-year confirms that the economy is expanding faster than it did a year earlier, with services, agriculture and the non-oil economy doing most of the work. That matters because Nigeria’s growth story is becoming less dependent on crude output volumes and more dependent on domestic activity, telecoms, trade, construction, financial services and real estate.But the quality of the growth still matters. Inflation at 15.69%, an MPR of 26.50%, a 10-year fixed income reference yield around 17.05%, and official FX around ₦1,372/$ all point to a market where nominal returns remain attractive but financing conditions are still tight. Equities have benefited from liquidity, earnings repricing and sector rotation, while fixed income remains relevant for investors seeking yield and capital preservation.Globally, the key story is not just weaker crude prices. It is the fall in the oil risk premium, slower foreign appetite for China, and still-elevated US yields. For Nigeria, lower oil prices can reduce inflation pressure at the margin, but they also reduce the comfort around fiscal revenues, external reserves and naira stability if sustained.

Nigeria Market Intelligence:

1. Nigeria’s Q1 GDP growth strengthens the domestic demand story

Nigeria’s economy grew by 3.89% year-on-year in real terms in Q1 2026, compared with 3.13% in Q1 2025. Nominal GDP rose to about ₦110.79 trillion from ₦94.05 trillion, reflecting 17.79% nominal growth.

Why it mattered:

The growth mix is more important than the headline number. The non-oil sector contributed 96.08% of GDP, while services remained the largest part of the economy. This supports the case for selective exposure to sectors tied to domestic activity, including banks, telecoms, trade-linked businesses, construction-related names and real estate-linked activity.

What comes next:

Investors should watch whether Q2 growth confirms the same pattern or whether inflation, high rates and energy costs begin to weaken household demand and corporate margins.

2. Non-oil growth remains the main investment signal

The non-oil sector grew by 3.94% and contributed 96.08% of GDP. Services grew by 4.31% and accounted for 57.73% of GDP, while agriculture rebounded to 3.15%.

Why it mattered:

This supports the argument that Nigeria’s listed market cannot be read only through oil. Banks, telecoms, consumer names, construction-linked companies and services-related businesses are now more central to the earnings story. The agriculture rebound is also important because food supply remains one of the most direct channels into inflation and consumer purchasing power.

What comes next:

Watch whether agriculture’s rebound is sustained. If food supply improves, inflation pressure could moderate further. If it does not, real consumer income may remain under pressure despite stronger GDP growth.

3. Power-sector financing stress is a warning for industrial productivity

Nigeria cancelled about $717.7 million in undisbursed World Bank financing under the Power Sector Recovery Operation after reform targets stalled. The programme’s closing date was reportedly moved to May 31, 2026. About $796 million had been disbursed out of roughly $1.51 billion committed..

Why it mattered:

This is not just a power-sector story. It affects the cost base of manufacturers, SMEs, industrial firms and consumer companies. If tariff deficits, FX-linked generation costs and weak sector finances persist, businesses may continue to rely heavily on self-generation, which keeps operating costs elevated and limits margin recovery.

What comes next:

Investors should watch whether the government introduces a credible replacement reform plan, addresses tariff shortfalls, or improves payment discipline across the electricity value chain.

4. Nigerian equities remain supported, but valuation discipline matters

Ranora’s market dashboard shows the NGX All Share Index reference level at 250,385.70 to close the week, while publicly available market trackers showed the ASI around 249,738.84 on May 28, 2026. The broad direction remains clear: Nigerian equities are still trading at elevated levels after a strong year-to-date rally.

Why it mattered:

At this stage of the rally, investors should be less focused on index direction alone and more focused on earnings quality, dividend capacity, balance-sheet strength and sector leadership. Banking, oil and gas, industrials and consumer names may not move together from here.

What comes next:

Watch market breadth. A rally led by fewer heavyweights is less durable than one supported by broader earnings upgrades.

5. Fixed income still offers a strong competing return

Nigeria’s 10-year fixed income yield is 17.05%, while recent public data show FGN bond yields still elevated across the curve. The MPR remains 26.50%, and inflation is 15.69%

Why it mattered:

High nominal yields keep fixed income attractive for conservative investors and institutions with liability-matching needs. The issue is duration. If inflation continues to ease and policy eventually turns more accommodative, longer-duration bonds could benefit. If inflation proves sticky, short duration remains cleaner.

What comes next:

Watch Treasury bill auction stop rates, bond auction demand and system liquidity. These will show whether investors are extending duration or still demanding compensation for inflation and FX risk.

Global Market Intelligence:

1. China’s FDI decline signals weaker global capital conviction

Foreign direct investment into China fell 10.3% year-on-year to CNY 287.7 billion in January to April 2026. High-tech industries attracted CNY 166.3 billion, up 20.3%, and accounted for 40.4% of total FDI.

Why it mattered:

This shows that capital is not leaving China uniformly. Investors are reducing broad exposure while still allocating to high-tech and strategic sectors. For emerging and frontier markets, the implication is that foreign capital is becoming more selective, not simply more abundant.

What comes next:

Watch whether China’s weaker broad FDI trend affects commodity demand expectations, emerging market flows and global manufacturing sentiment

2. Oil’s pullback changes the Nigeria market equation

Brent at $90.79 and WTI at $86.72. The supplied market note also states that Brent fell sharply month-on-month to about $92.45 per barrel, its largest monthly decline since 2020.

Why it mattered:

For Nigeria, lower oil can help reduce imported inflation and energy-cost pressure if sustained. But it can also weaken fiscal revenue assumptions, FX supply expectations and external reserve comfort. That makes oil a two-sided signal for Nigerian assets.

What comes next:

Watch whether Brent stabilises above the fiscal comfort zone or continues lower. A sustained decline would matter more for the naira, reserves and government revenue than a short-term correction.

3.US growth remains positive, but rates are still the real market driver

US GDP growth at 2.70%. Publicly available BEA data show Q1 2026 annualized GDP growth was first estimated at 2.0%, with later reporting indicating a second estimate of 1.6%. US unemployment was 4.30%, and April CPI was 3.80% year-on-year.

Why it mattered:

For global investors, the key issue is that inflation is not yet comfortably back to target. That keeps US yields elevated and limits the case for aggressive rate cuts. For Nigeria, higher US yields can reduce foreign appetite for frontier-market risk unless local yields and FX confidence remain compelling..

What comes next:

Watch US inflation and jobs data. A softer inflation path would support risk assets and emerging market flows. Sticky inflation would keep pressure on global bonds and frontier-market currencies.

4. US yields and dollar levels remain important for Nigeria

US 10-year yield at 4.43%, the S&P 500 at 7,583.30, the trade-weighted dollar major index at 98.79, and the VIX at 15.27%.

Why it mattered:

A US 10-year yield above 4% keeps global capital selective. For Nigeria, this means local assets must offer enough yield, liquidity and FX credibility to compete for foreign capital. A calmer VIX helps risk appetite, but elevated US yields still raise the bar for frontier-market inflows.

What comes next:

Watch the next US inflation print, Fed communication and dollar direction. Nigeria benefits most from a combination of lower US yields, stable oil prices and credible naira liquidity.

Asset Class Implications:

Ranora View:

Ranora’s view is that Nigeria’s macro story improved this week, but the investable story remains selective.

The GDP print supports confidence in domestic activity, especially services, agriculture, telecoms, trade, construction and financial services. That is constructive for equities, particularly companies with pricing power, strong balance sheets and exposure to resilient demand. However, the same economy is still operating with high policy rates, elevated yields and unresolved infrastructure constraints. This means investors should not treat growth as a blanket buy signal.

In fixed income, high nominal yields continue to offer a credible alternative to equities. For investors managing risk, short-to-medium duration still looks attractive while inflation is above target and monetary policy remains tight. If inflation continues to moderate, duration extension may become more compelling, but that trade requires stronger evidence.

The biggest external risk is oil. Brent near the low $90s is still supportive compared with historical stress levels, but the sharp monthly decline matters. Nigeria benefits from lower imported inflation, but the country also needs oil receipts for fiscal and FX stability. If oil falls further while US yields remain elevated, the naira and foreign portfolio appetite could face renewed pressure.

The core positioning message is this: stay invested, but be selective. Favour quality equities, income-generating fixed income, and sectors that can defend margins in a high-rate, infrastructure-constrained economy..

What to Expect Next Week:

Nigeria’s next inflation print: whether April’s 15.69% becomes a temporary rise or the start of renewed price pressure.

Treasury bill and bond auction pricing: whether investors continue demanding high yields or begin extending duration.

Oil price direction: whether Brent stabilises near current levels or continues to unwind its geopolitical premium.

Naira liquidity and official FX turnover: whether reserve strength translates into more reliable dollar supply.

Power-sector reform response: whether the cancelled World Bank loan is followed by a credible domestic reform plan.

Question of the week:

With Nigerian GDP improving but interest rates still high, should investors lean more toward equities for growth or fixed income for yield over the next quarter?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.