Weekly Roundup: Higher Yields, Equity Rotation, and the Return of Rate Risk

Ranora Market Outlook - This week showed that Nigerian investors are still being paid to wait in fixed income, while global rate expectations are turning less friendly for risk assets.

Opening View

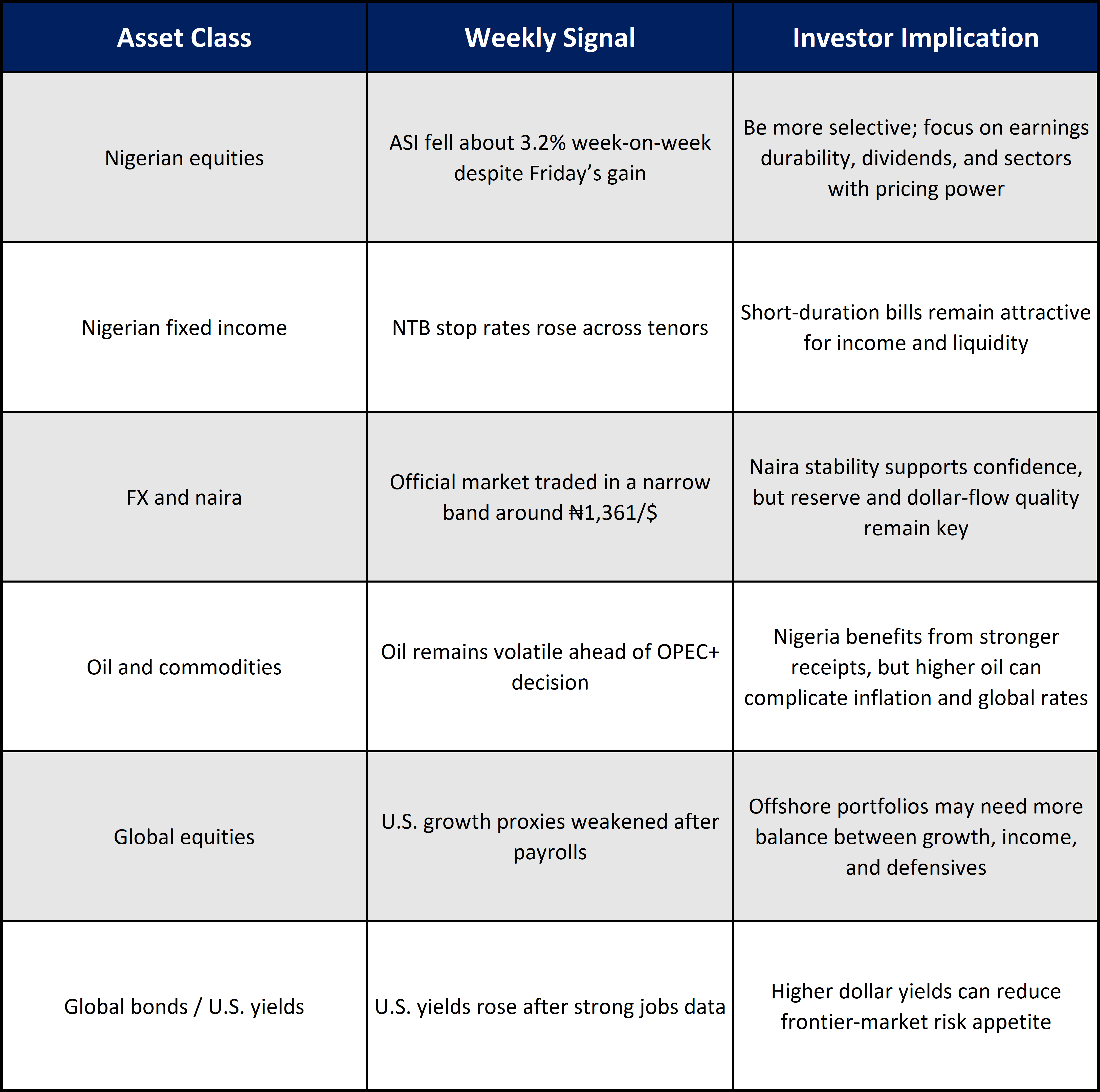

The week ended with two clear messages for investors. In Nigeria, liquidity is still large enough to support demand for government securities, but the CBN is not allowing that liquidity to fully suppress yields. The June 3 Treasury bills auction absorbed ₦1.457 trillion, above the ₦1 trillion offered, with stop rates rising across the 91-day, 182-day, and 364-day bills. That keeps short-duration naira fixed income relevant for investors who want income, liquidity, and lower equity volatility.

Equities told a different story. The NGX All-Share Index closed at 242,323.52 on Friday, down from 250,385.47 the previous Friday, implying a weekly decline of about 3.2%. Friday’s rebound was useful, but it did not erase the midweek selloff.

Globally, the U.S. jobs report changed the tone. Payrolls rose by 172,000 in May and unemployment held at 4.3%, giving the Federal Reserve less reason to ease policy quickly. That matters for Nigeria because higher U.S. yields can reduce foreign appetite for frontier-market duration and equities, even when local yields look attractive

The Big Picture:

This was a week of yield discipline. Nigerian fixed income remained the cleanest expression of the domestic macro setup: inflation is still above comfort levels, policy remains tight, and liquidity needs to be sterilised. The CBN’s auction result suggests that investors are willing to lock in one-year naira rates, but only at slightly better pricing.

For equities, the issue is not that Nigeria’s corporate story has disappeared. It is that valuations, profit-taking, and alternative yields are now competing more aggressively for investor attention. When Treasury bills offer mid-teen returns with lower volatility, equity investors become more selective.

The global layer makes that selection harder. A stronger U.S. labour market, higher Treasury yields, and a firmer dollar can tighten the external backdrop for emerging and frontier markets. Nigeria’s reserve position and steadier official FX market help, but they do not fully remove the risk that global capital becomes more expensive..

Nigeria Market Intelligence

NGX gave background despite Friday’s rebound

What happened:

The NGX All-Share Index closed at 242,323.52 on Friday, June 5, after gaining 0.33% on the day. But that was still below the 250,385.47 close recorded on Friday, May 29, implying a weekly decline of about 3.2%. Market capitalisation also fell from ₦160.51 trillion to ₦155.42 trillion over the same period.

Why it mattered:

The market’s Friday bounce showed that buyers are still present, but the weekly move points to profit-taking and a more selective equity market. This is important because Nigerian equities have had a strong run, and investors now need earnings visibility, dividend strength, or sector-specific catalysts to justify fresh risk.

What to watch next:

Watch whether banks, energy names, and large-cap consumer stocks stabilise next week. If market breadth weakens again, the rebound may remain tactical rather than the start of a stronger rotation.

Treasury bill yields moved higher despite heavy demand

What happened:

The CBN raised ₦1.457 trillion at the June 3 NTB auction against a ₦1 trillion offer. Total subscriptions reached ₦2.160 trillion, with the 364-day bill attracting ₦1.946 trillion in bids. Stop rates rose to 16.05% for 91-day, 16.19% for 182-day, and 16.35% for 364-day bills.

Why it mattered:

This tells investors two things at once: liquidity is still strong, and the market is demanding better compensation for duration. For portfolios, the implication is that one-year Treasury bills remain attractive relative to cash, especially for investors who want predictable income without taking equity drawdown risk.

What to watch next:

The next test is whether the CBN uses more OMO issuance to absorb June liquidity. If liquidity remains heavy, secondary-market yields may compress; if the CBN drains aggressively, yields could stay elevated.

Inflation remains the constraint on policy easing

What happened:

Nigeria’s headline inflation rose to 15.69% in April 2026 from 15.38% in March. Food inflation stood at 16.06% year-on-year. The CBN’s policy rate remains at 26.50%.

Why it mattered:

Even with inflation far below last year’s levels, the month-on-month pressure means the CBN has limited room to move quickly toward easier policy. For investors, that supports a continued income opportunity in naira fixed income, but it also keeps borrowing costs high for corporates and households.

What to watch next:

May inflation will matter for the July policy setup. A renewed acceleration would strengthen the case for continued tight liquidity management.

Naira stability is being helped by reserves and tighter FX conditions

What happened:

The official NFEM rate was reported around ₦1,361/$ on June 5, with the week’s official trading band around ₦1,359 to ₦1,365. Nigeria’s gross external reserves were also reported near $49.58 billion as of May 29.

Why it mattered:

A steadier naira reduces the immediate pressure on imported inflation and gives foreign investors more confidence in naira assets. But the stability still depends on oil earnings, reserve quality, portfolio inflows, and CBN market management.

What to watch next:

The key risk is not one day’s FX print. It is whether dollar liquidity remains sufficient if global yields rise and foreign investors demand more compensation for frontier-market risk.

Global Market Intelligence:

U.S. payrolls pushed rate risk back into the market

What happened:

U.S. nonfarm payrolls rose by 172,000 in May, while unemployment held at 4.3%. March and April payrolls were revised higher by a combined 93,000 jobs.

Why it mattered:

The report reduces the urgency for Fed easing and raises the hurdle for a dovish pivot. For Nigerian markets, this matters because higher U.S. yields can pull capital toward dollar assets and make foreign participation in naira bonds and equities more selective.

What to watch next:

The June 16-17 Fed meeting is now more important for guidance than for the rate decision itself. Investors should watch whether the Fed validates the market’s higher-for-longer repricing.

U.S. yields rose after the jobs report

What happened:

Reuters reported that the U.S. 2-year yield rose to about 4.15% and the 10-year yield to about 4.54% after the jobs data.

Why it mattered:

The front end of the curve is particularly important because it tracks Fed expectations. Higher short-term U.S. yields reduce the relative appeal of riskier carry trades and can pressure emerging-market assets if investors demand wider spreads.

What to watch next:

If the 10-year yield keeps moving higher, global equity valuations may face renewed pressure, especially in long-duration growth and AI-related stocks.

U.S. equities were pressured by rate repricing

What happened:

At the time of writing, SPY, a proxy for the S&P 500, was down about 1.7% on the day, while QQQ, a Nasdaq-heavy proxy, was down about 3.3%.

Why it mattered:

This is the market applying a higher discount rate to growth assets. For Nigerian investors with offshore exposure, it argues for checking whether portfolios are too concentrated in expensive U.S. growth stocks without enough income or defensive balance.

What to watch next:

Watch whether Friday’s weakness remains contained or becomes a broader de-risking move across global equities..

Oil remains a two-sided issue for Nigeria

What happened:

Oil-linked assets were lower at the time of writing, with USO down about 3.0% intraday. Separately, OPEC+ members were expected to consider a modest July output increase at their June 7 meeting.

Why it mattered:

For Nigeria, oil is both a fiscal support and an inflation risk. Higher oil prices can support external receipts and reserves, but they can also raise global inflation pressure, keep U.S. rates higher, and increase domestic energy-linked costs.

What to watch next:

The June 7 OPEC+ decision and the next IEA oil market update on June 17 will matter for Nigeria’s fiscal and FX assumptions.

Asset Class Implications:

Ranora View:

The main lesson from this week is that yield is back in charge. Nigerian investors do not need to force risk when Treasury bills are still offering mid-teen returns and the equity market is showing signs of valuation digestion. That does not mean equities should be abandoned. It means equity exposure should be earned through earnings quality, dividend capacity, balance-sheet strength, and sector catalysts.

For institutions, the near-term opportunity remains in disciplined duration management. One-year bills are attractive, but investors should avoid assuming that yields will fall in a straight line. The CBN still has to manage liquidity carefully, inflation has not fully settled, and global rates have become less supportive.

For businesses, the message is also clear: funding costs are unlikely to fall quickly. Companies with strong cash generation and lower refinancing needs should continue to command a premium.

What to Watch Next:

Nigeria’s May inflation print and whether food inflation keeps pressure on the disinflation story.

CBN liquidity management through OMO auctions after the large June NTB allotment.

NGX breadth next week, especially whether large-cap banking and energy names stabilise.

The June 16-17 Federal Reserve meeting and its guidance after the strong U.S. jobs report.

OPEC+ output signals and their impact on Brent, Nigeria’s oil revenue expectations, and imported inflation risk.

Question of the day:

If Nigerian Treasury bills continue to offer mid-teen yields, what would make you increase equity exposure from here: cheaper valuations, stronger earnings, higher dividends, or clearer FX stability?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.