Weekly Roundup: Liquidity, Rates and Oil Set the Market Tone

Ranora Market Outlook - This week’s market signal was clear: Nigerian assets are still being priced around liquidity, FX confidence, and the level of real returns available in fixed income.

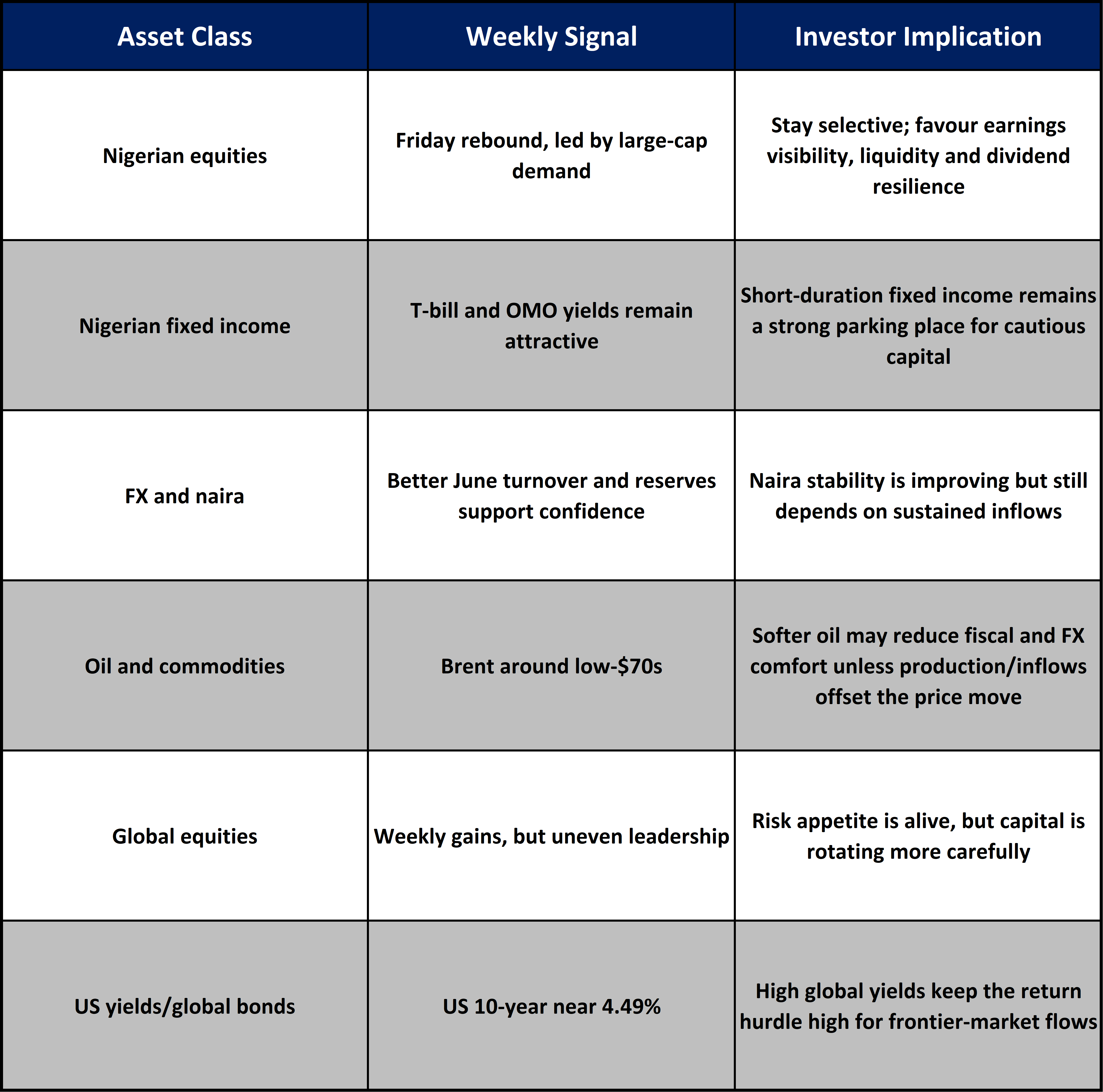

Opening View

The week ended with a useful reminder for Nigerian investors: liquidity is still the dominant market variable. Equities recovered sharply on Friday, but the broader message was not simply that risk appetite returned. It was that investors are still rotating quickly between cash, fixed income and selective equities depending on where yield, FX comfort and earnings visibility look strongest.

Nigeria’s macro backdrop remains supportive in parts but not frictionless. External reserves have improved, the naira showed resilience in June, and Q1 GDP growth remained positive. But inflation is still above comfort levels, the CBN is keeping policy tight, and the planned scale of Q3 Treasury bill issuance suggests domestic rates may remain a major competitor to equities.

Globally, the week was shaped by softer US labour data, mixed equity performance, elevated US yields, and a weaker oil price environment. For Nigeria, Brent near the low-$70s is not just an oil-market story. It affects fiscal expectations, external inflows, reserves confidence and the naira narrative. The key investor question now is whether Nigeria’s improving reserves and market liquidity can continue to offset pressure from softer oil prices and heavy domestic borrowing.

The Big Picture:

The biggest implication from this week is that Nigerian markets are no longer being driven by a single story. Equities are still attractive where earnings and liquidity are strong, but fixed income remains difficult to ignore because yields are high and supply is rising. FX stability is improving, but it remains dependent on sustained inflows, reserves strength and credible policy execution.

Globally, investors moved away from a simple “AI-led risk-on” trade and into a more balanced rotation. US labour data reduced expectations of another near-term Fed hike, but US 10-year yields still hovered around 4.49%, which keeps global capital selective toward frontier and emerging markets. For Nigeria, that means foreign interest will likely remain concentrated in liquid, high-yielding instruments and equities with clear dollar-linked or inflation-resilient earnings.

Nigeria Market Intelligence

Nigerian equities rebounded, but selectivity still matters

What happened: The NGX All-Share Index closed Friday, July 3, at 229,240.34, up 2.19% on the day, with market capitalization at about ₦147.10 trillion. Market breadth was positive, with 41 gainers against 14 decliners. Airtel Africa led the gainers with a 10% move.

Why it mattered: The Friday rebound shows that liquidity can still move the market sharply when large-cap names attract demand. But the broader implication is more nuanced: after a strong year-to-date rally, investors are likely to become more valuation-sensitive. The best opportunities may be in names where earnings growth, dividend capacity or FX-linked revenue can justify higher prices.

What to watch next: Watch whether the rally broadens beyond a few large-cap counters. A narrow rebound led by index-heavy stocks is less durable than a broad recovery across banks, consumer names, industrials and telecoms.

Fixed income remains the main competitor to equities

What happened: CBN’s June 17 Treasury bill auction cleared at marginal rates of 16.28% for 91-day, 16.50% for 182-day and 17.34% for 364-day bills. FMDQ’s July 2 market data showed Nigerian Treasury bill true yields ranging from about 16.05% on the short end to above 20% around the longer bill maturities.

Why it mattered: At these levels, fixed income is not a passive allocation. It is an active competitor for capital. For pension funds, corporates and conservative investors, short-duration bills still offer a strong nominal return with lower volatility than equities.

What to watch next: The reported Q3 Treasury bill issuance plan of about ₦5.8 trillion needs close monitoring because heavy supply could keep yields elevated and preserve demand for short-duration fixed income.

FX stability improved, but the naira still needs consistent inflows

What happened: CBN data and FMDA, reported that the naira improved to ₦1,370.15/$ on Thursday from ₦1,372.41/$ on Wednesday, while June NFEM turnover rose by about 45% to more than $12.9 billion. Average external reserves reportedly increased by 4.09% to $51.04 billion during June.

Why it mattered: The improvement supports investor confidence, but the naira’s stability is still flow-dependent. Stronger turnover and reserves give the CBN more room to manage volatility, but higher domestic liquidity, import demand or softer oil receipts could test the market again.

What to watch next: Watch NFEM turnover, external reserves, oil receipts and whether the parallel-market gap continues to narrow.

Reserves are stronger, but the market will ask how durable the buffer is

What happened: Nigeria’s external reserves were reported at $51.04 billion as of June 18, 2026, up 35.35% year-on-year, according to CBN data.

Why it mattered: A stronger reserves position improves FX confidence and reduces immediate pressure on the naira. It may also improve foreign investor comfort around repatriation risk. But reserves strength is most valuable when it is supported by durable inflows, not only intervention capacity.

What to watch next: The key test is whether reserves remain firm if Brent stays near the low-$70s and domestic FX demand rises.

Global Market Intelligence:

US labour data softened, changing the Fed conversation

What happened: The US economy added 57,000 jobs in June, while unemployment stood at 4.2%, according to the US Bureau of Labor Statistics.

Why it mattered: Softer hiring reduces pressure for additional Fed tightening, but it does not automatically create a strong rate-cut story. For frontier markets like Nigeria, the practical implication is that global capital may remain selective rather than aggressively risk-seeking.

What to watch next: US inflation, wage growth and Fed commentary ahead of the next policy meeting.

The Fed is still on hold, but US yields remain high

What happened: The Federal Reserve held the federal funds target range at 3.50% to 3.75% at its June 17 meeting. US 10-year Treasury yields were around 4.49% on July 3 market data.

Why it mattered: High US yields keep the hurdle rate elevated for emerging and frontier market allocations. Nigeria can still attract flows, but investors will demand adequate compensation through yields, FX confidence and liquidity.

What to watch next: Whether US yields break lower after weak jobs data or remain sticky because inflation risks persist.

US equities rose for the week, but the leadership was uneven

What happened: For the week, the S&P 500 gained 1.8%, the Dow rose 2.0%, and the Nasdaq added 2.1%, although Thursday’s session showed rotation: the Dow rose to another record while the Nasdaq fell 0.8%.

Why it mattered: The market is not abandoning risk, but it is becoming more selective. That matters for Nigeria because global risk appetite affects foreign participation in frontier equities and local-currency debt.

What to watch next: Whether investors continue rotating out of expensive technology trades into broader cyclicals, defensives and value sectors.

Brent crude near $72 changes the fiscal conversation

What happened: Brent traded around $72.09 per barrel on July 3, down about 24% over the previous month, according to Trading Economics. Investing.com historical data showed Brent around $72.02 on July 3.

Why it mattered: Lower Brent reduces the oil-revenue tailwind for Nigeria, even if production improves. For investors, this matters because oil revenue influences fiscal expectations, reserves, FX confidence and sovereign risk pricing.

What to watch next: OPEC+ meets on July 5 after previously agreeing to a 188,000 barrels-per-day July production adjustment.

Asset Class Implications:

Ranora View:

Ranora’s view is that the Nigerian market is entering a phase where liquidity management matters more than headline optimism. Equities can still perform, especially where earnings are strong and foreign or institutional demand is present. But the high-yield fixed-income environment means equity investors need a clearer margin of safety.

Short-duration fixed income remains attractive for investors prioritising capital preservation and predictable returns. Equities should be approached through quality, liquidity and sector earnings power rather than broad index exposure alone. Banks, telecoms and select industrial names may continue to attract attention, but valuations need to be tested against yields available in Treasury bills and money-market instruments.

The naira story is better than it was, but not risk-free. Stronger reserves and improved FX turnover support confidence, yet lower oil prices and heavy domestic borrowing could reintroduce pressure. For businesses, this is a week to watch funding costs, FX planning and working-capital discipline. For investors, the central question is not whether Nigeria is attractive. It is whether each asset offers enough return for the liquidity, inflation and FX risks being taken.

What to Watch Next:

OPEC+ July 5 meeting and what it signals for Brent crude and Nigerian oil-revenue expectations.

CBN Treasury bill issuance and whether heavy Q3 supply keeps yields elevated.

NFEM turnover and whether the naira holds near recent levels.

NGX breadth next week: whether Friday’s rebound broadens or remains concentrated in large caps.

US inflation and Fed messaging after the softer June jobs report.

Question of the day:

If Nigerian Treasury bills continue to offer high yields while equities remain volatile, where should local investors take more risk next: duration, dividend equities, banks, telecoms, or dollar-linked assets?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.