Weekly Roundup: Policy Tightness Supported the Naira While Global Yields Did the Heavy Lifting

Ranora Market Outlook -Nigeria’s macro story improved at the margin this week, but higher U.S. yields still shaped the global investment backdrop.

The Week in One Paragraph

This week’s market story was not simply about prices moving. It was about which policy signals investors were prepared to trust. In Nigeria, the CBN’s decision to leave the benchmark interest rate unchanged at 26.5% reinforced the message that monetary authorities are still prioritising inflation control, FX stability, and policy credibility. That helped support demand for local fixed income and added to the naira’s improving tone against major currencies, including the euro. But the domestic story did not unfold in isolation. Globally, investors had to absorb a U.S. labour market that remains firm, a Federal Reserve still facing sticky inflation risks, and bond yields that continue to keep financial conditions tight. The practical implication is that Nigeria’s market is benefiting from better domestic policy discipline, but external liquidity is not turning supportive in a way that would justify complacency. This remains a market where carry, policy credibility, and selectivity matter more than broad optimism.

Top 5 Market Stories of the Week:

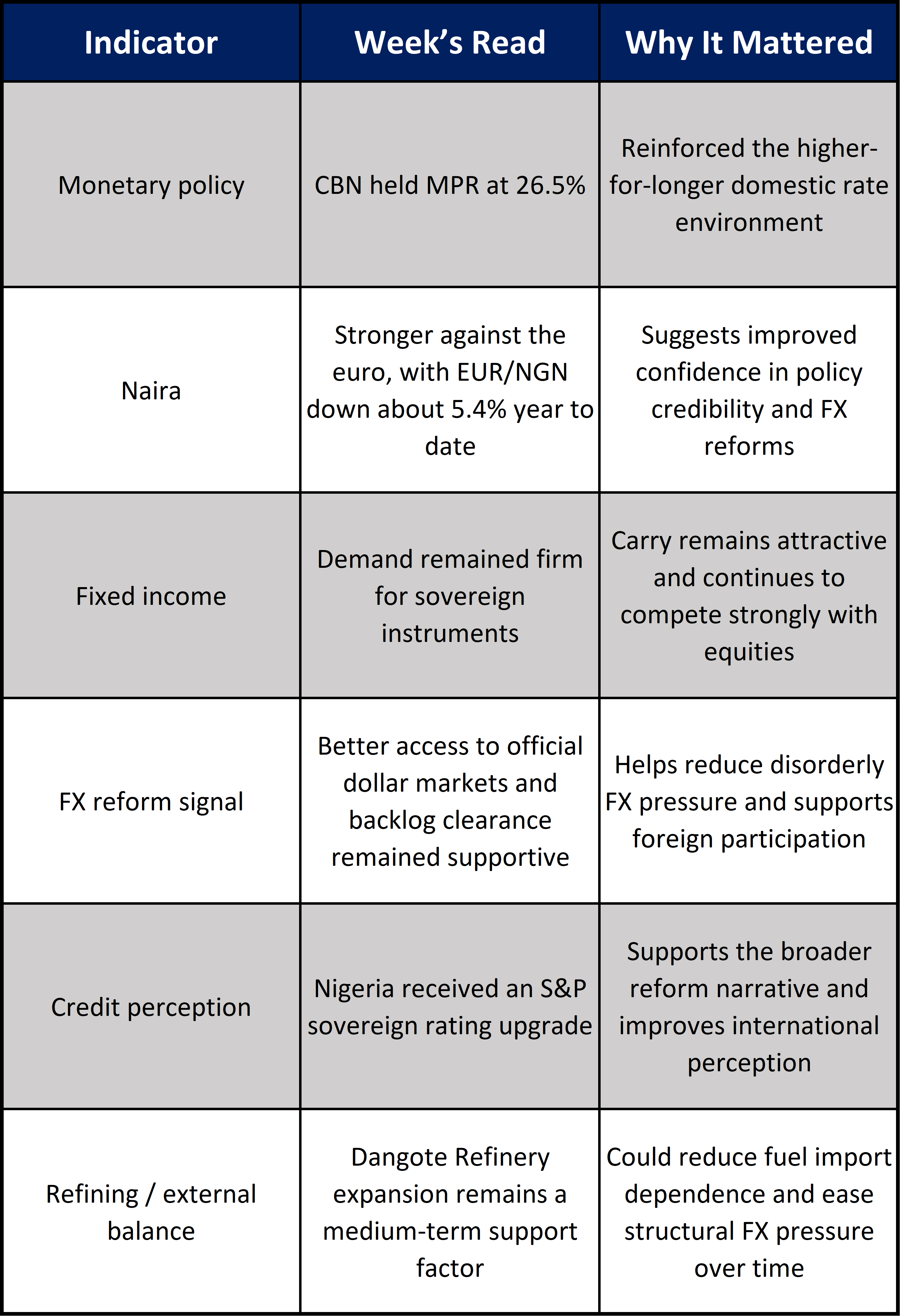

1. The CBN held rates at 26.5%, reinforcing the higher-for-longer domestic stance

The Monetary Policy Committee left the benchmark rate unchanged this week, signalling that the central bank is still focused on inflation control and macro stability.

Why it mattered:

This was a clear message to both local and foreign investors that policy easing is not imminent. That keeps Nigerian fixed income attractive and supports confidence in the broader reform direction.

What comes next:

The next inflation prints and FX conditions will determine whether this stance remains durable, but for now the policy bias still favours tight liquidity and elevated yields.

2. The naira strengthened against the euro as domestic reform credibility improved

The euro has weakened against the naira by roughly 5.4% this year, falling from around ₦1,684 to about ₦1,592.5, supported by tighter monetary policy, improved access to official FX markets, and broader reform credibility.

Why it mattered:

This is not just a currency story. It suggests that tighter rates, FX backlog clearance, the willing-buyer willing-seller framework, and better foreign participation in Nigerian debt markets are helping stabilise the currency complex. That can reduce imported cost pressure and improve confidence in local assets.

What comes next:

The key question is whether this improvement can hold if external dollar conditions become less friendly. Nigeria’s FX story is better than it was, but it still depends on sustained confidence and continued liquidity discipline.

3. Nigerian fixed income remained the clearest beneficiary of current conditions

With the CBN staying tight and inflation still elevated, local debt markets continued to benefit from demand for high nominal yields and sovereign carry.

Why it mattered:

This reinforces the case that fixed income remains highly competitive against equities in the current environment. Investors do not need to take substantial balance-sheet risk to earn attractive returns, which naturally affects equity appetite.

What comes next:

Unless inflation falls more decisively or yields compress sharply, short-duration and sovereign paper may remain the default allocation for conservative capital.

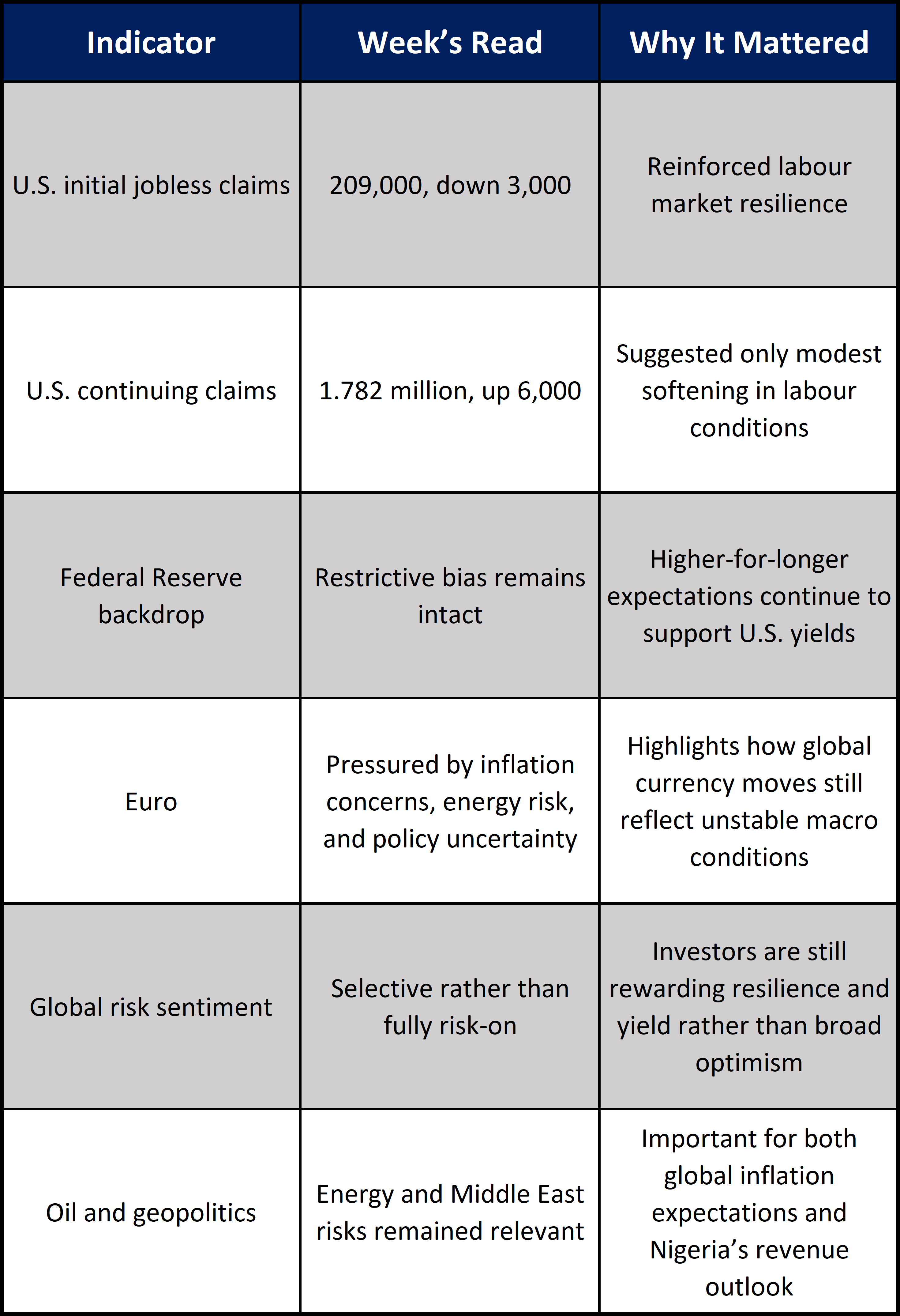

4. U.S. labour market resilience kept the global rates story alive

Initial jobless claims in the United States fell by 3,000 to 209,000 in the second week of May, matching expectations, while continuing claims rose only modestly to 1.782 million.

Why it mattered:

This matters because a stable labour market gives the Federal Reserve room to keep policy restrictive for longer. That supports higher U.S. yields, a firmer dollar, and a more demanding environment for emerging and frontier markets.

What comes next:

If U.S. labour data remains firm and inflation stays sticky, global investors may stay selective on risk assets, which could cap the pace of foreign inflows into Nigeria.

5. The euro and broader global policy mix remained unsettled

The euro came under pressure from a combination of geopolitical tension, energy-price risk, and shifting monetary expectations. At the same time, hawkish Fed signals and uncertainty around growth limited broader enthusiasm for global risk assets.

Why it mattered:

For Nigeria, this matters because the external environment still shapes capital flows, dollar liquidity, and risk pricing. A stronger reform story at home helps, but it does not eliminate vulnerability to global rate and currency moves.

What comes next:

Watch the interaction between Fed expectations, oil, and major currency moves. That mix will continue to influence how much breathing room frontier markets get.

Nigeria Market Scorecard:

Global Market Scorecard:

The Main Lesson From This Week:

The most important lesson from this week is that domestic reform progress is helping Nigeria, but it is not operating in a vacuum. The combination of a tighter CBN stance, a firmer naira, and improved sovereign credibility gives local investors a stronger macro base than they had a year ago. But globally, the investment climate is still being shaped by high U.S. yields and a Federal Reserve with little reason to rush into easing. That means Nigerian assets can perform, but they will likely do so on the strength of local policy credibility and yield support rather than on the back of abundant global risk appetite.

Ranora View:

The domestic signal improved this week. The naira’s strength against the euro, combined with the CBN’s steady policy stance, supports the argument that Nigeria’s reform framework is gaining traction with markets. But the global picture remains less forgiving. A resilient U.S. labour market keeps higher-for-longer Fed pricing in play, which could limit foreign appetite for frontier risk even when local fundamentals improve. For investors, that points to a barbell approach: keep meaningful exposure to attractive local fixed income, while staying selective in equities with a bias toward quality balance sheets, pricing power, and sectors that can benefit from macro stabilisation rather than simply survive it.

What to Expect Next Week:

Whether the naira can hold its recent strength if global dollar conditions remain firm.

Any shift in local fixed-income demand as investors reassess inflation and policy expectations.

Whether Nigerian equities regain momentum or continue to lose ground to high-yield sovereign paper.

Fresh U.S. macro data that could influence Fed expectations and Treasury yields.

Oil and geopolitical developments that may affect both inflation expectations and Nigeria’s external position.

Question of the week:

If Nigeria’s reform story continues to improve but U.S. yields stay elevated, which matters more for investor positioning over the next quarter: local policy credibility or global liquidity conditions?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.