Weekly Roundup: Profit Taking Hits Nigerian Equities as Global Rates Stay Tight

Ranora Market Outlook - This week reminded investors that high yields, currency discipline, and selective equity exposure still matter more than headline market momentum.

Opening View

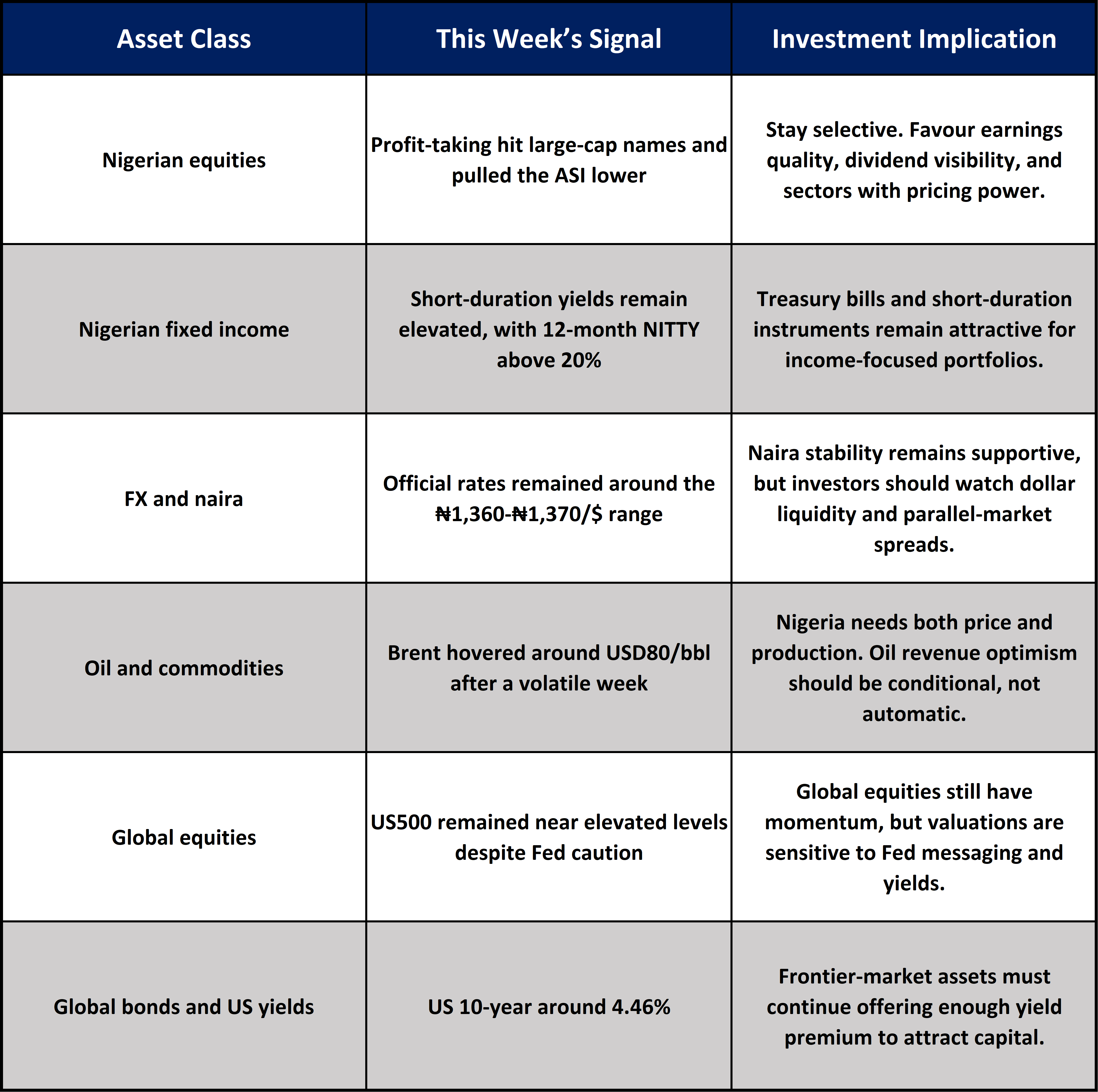

The week ended June 19, 2026 was defined by a useful tension: Nigerian equities remained structurally strong on a year-to-date basis, but near-term profit-taking showed that valuations and liquidity still matter. The NGX All-Share Index fell sharply in the latest reported session, with heavyweights in industrials, oil and gas, insurance, and banking among the pressure points. That does not automatically break the bull case for Nigerian equities, but it changes the conversation from broad market optimism to sector selection, earnings delivery, and entry discipline.

In fixed income, yields remain high enough to compete seriously with equities. FMDQ data showed 12-month Nigerian Treasury bill true yields above 20% as of June 18, while money market rates stayed elevated. For investors, that keeps short-duration income attractive, especially where equity positions have already delivered strong gains.

Globally, the Federal Reserve held rates at 3.50%-3.75% this week, while US yields, dollar strength, oil volatility, and gold weakness shaped risk appetite. For Nigeria, the main implication is clear: global capital will still demand yield, currency stability, and credible policy signals before increasing frontier-market exposure.

The Big Picture:

This was a week of repricing, not panic.

Nigeria’s inflation picture remains important. NBS data showed headline inflation at 15.93% in May 2026, with food inflation at 16.96% and core inflation at 16.82%. That keeps the CBN under pressure to avoid premature easing, even after the February rate cut to 26.5%. The CBN’s latest listed MPC decision showed the MPR at 26.5%, while the May MPC communication also pointed to a cautious hold.

The investment implication is that Nigerian markets are still operating under a high nominal yield regime. That supports fixed income demand, helps protect naira assets if FX liquidity remains orderly, and raises the hurdle rate for equities. Stocks with weak earnings visibility may struggle, while banks, cash-generative consumer names, and companies with pricing power should remain better placed.

Globally, the Fed’s decision to hold rates keeps US real-yield competition alive. The US 10-year yield was around 4.46% on June 18, while the US500 hovered near 7,496 on June 19. Gold fell to about USD4,150/oz, and Brent crude traded around USD80/bbl after a volatile week shaped by US-Iran and Strait of Hormuz developments.

Nigeria Market Intelligence

Nigerian equities: profit-taking became the week’s clearest signal

What happened: The NGX All-Share Index dropped to 237,404.92 in the latest reported session, with market capitalisation falling to about ₦152.27 trillion. Market reports pointed to losses in names including Dangote Cement, Oando, NEM, Dangote Sugar, and Zenith Bank.

Why it matters: The Nigerian equity market has delivered a powerful run, but this week showed that profit-taking can become concentrated when investors begin locking in gains across large-cap names. The pressure in industrials and banks matters because these are index-heavy sectors. When they correct, the broader market feels it quickly.

What to watch next: Watch whether bargain hunting returns to banks and defensives, or whether selling extends into smaller and mid-cap names. A controlled pullback would be healthy. A broader rotation out of high-beta names would suggest investors are becoming more sensitive to valuation.

Inflation: May CPI keeps policy easing on a short leash

What happened: NBS reported headline inflation at 15.93% for May 2026. Food inflation stood at 16.96%, while core inflation was 16.82%.

Why it matters: The latest inflation reading weakens the case for aggressive near-term monetary easing. Even if inflation is far below the extreme levels of prior years, the month-to-month direction matters for the CBN. Rising food and core inflation keep real household income under pressure and may delay a deeper decline in market yields.

What to watch next: The June inflation print will be important. If food inflation continues to rise, the CBN may prefer to hold rates again rather than risk weakening the naira or reigniting inflation expectations.

Fixed income: short-duration yields remain hard to ignore

What happened: FMDQ data for June 18 showed 12-month Nigerian Treasury bill true yield at 20.2452%, with 9-month true yield at 19.1115%. Secondary-market NTB yields also remained elevated, with the June 2027 NTB yield shown at 19.29%.

Why it matters: At these levels, fixed income remains a serious competitor to equities. For conservative investors, short-duration bills can still provide attractive nominal income without taking full equity-market volatility. For equities, this means companies must justify valuations with earnings growth, dividend visibility, or clear catalysts.

What to watch next: Watch stop rates at the next NTB auction, banking-system liquidity, and whether pension funds continue to prefer duration-light fixed income exposure.

Global Market Intelligence:

The Fed held rates, but the message still supports higher-for-longer positioning

What happened: The Federal Reserve held the federal funds target range at 3.50%-3.75% on June 17, 2026.

Why it matters: A Fed hold does not mean easy money is back. With US yields still high, global capital has less urgency to chase frontier-market risk unless the yield premium is compelling and currency risk is contained. This matters for Nigeria because foreign portfolio flows will remain selective.

What to watch next: Watch the next US inflation prints, Fed speeches, and whether markets price rate cuts, hikes, or a longer hold.

US yields remain a benchmark for global risk pricing

What happened: The US 10-year Treasury yield eased to about 4.46% on June 18, according to Trading Economics.

Why it matters: A 4% plus US 10-year yield keeps global discount rates elevated. For Nigerian fixed income, this means the country must preserve a meaningful yield premium. For equities, it reduces tolerance for weak earnings and speculative valuation expansion.

What to watch next: Watch whether the US 10-year moves back toward 4.5%-4.7%. That would pressure emerging and frontier-market duration.

Oil volatility matters more for Nigeria than the headline Brent price

What happened: Brent crude traded around USD80/bbl on June 19 after a volatile week tied to US-Iran developments and Strait of Hormuz shipping expectations.

Why it matters: For Nigeria, oil above budget assumptions can support fiscal revenue and FX inflows, but volatility complicates planning. A sustained fall in Brent would reduce external-account comfort. A sharp rebound from geopolitical stress could support revenue but worsen global inflation and imported cost pressure.

What to watch next: Watch actual export volumes, not only Brent prices. Nigeria benefits from higher oil prices only if production, exports, and receipts are strong enough.

Gold weakness signals a shift in global defensive positioning

What happened: Gold fell to about USD4,150/oz on June 19, down more than 8% over the month.

Why it matters: Gold’s weakness suggests some geopolitical risk premium has faded while real-yield and dollar pressures remain important. For Nigerian investors, this matters because dollar strength and high US yields can tighten financial conditions for emerging markets even when commodity stress eases.

What to watch next: Watch whether gold stabilizes if geopolitical risk returns,or continues to weaken if the dollar and US yields stay firm.

Asset Class Implications:

Ranora View:

The main lesson from this week is that Nigerian markets are not short of opportunity, but the easy part of the trade may be behind us.

Equities remain supported by structural themes: naira stabilisation, stronger bank capital, high nominal earnings growth, and domestic liquidity. But after a strong run, the market now needs earnings to validate prices. Broad buying is less attractive than targeted exposure to companies with clear margins, dividend capacity, and balance-sheet strength.

Fixed income remains the cleaner near-term allocation for conservative capital. With short-duration Nigerian yields still high, investors do not need to stretch aggressively into equity risk unless the expected return is compelling. This may keep treasury bills and selected short bonds attractive while investors wait for better equity entry points.

For businesses, the message is also practical: financing costs remain high, FX planning still matters, and consumer demand is not yet out of pressure. Companies with local sourcing, pricing power, and disciplined working-capital management should remain better positioned.

What to Watch Next:

NGX follow-through: whether Friday and early next week bring bargain hunting or deeper profit-taking.

June inflation direction: especially food inflation and core inflation.

CBN liquidity management: NTB stop rates, OMO activity, and banking-system liquidity.

Naira stability: official FX rates, parallel-market spreads, and external-reserve signals.

Oil market direction: whether Brent holds near USD80/bbl or re-prices lower as geopolitical risk fades.

Question of the day:

With Nigerian fixed income yields still attractive and equities coming off a strong run, would you rather add duration, buy the equity pullback, or hold more cash until the next inflation and FX signals are clearer?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.