Weekly Roundup: Profit Taking Hits Nigerian Equities as Global Rate Risk Stays Alive

Ranora Market Outlook - This week showed why liquidity, inflation, oil prices, and US rate expectations remain the main variables for Nigerian market positioning.

Opening View

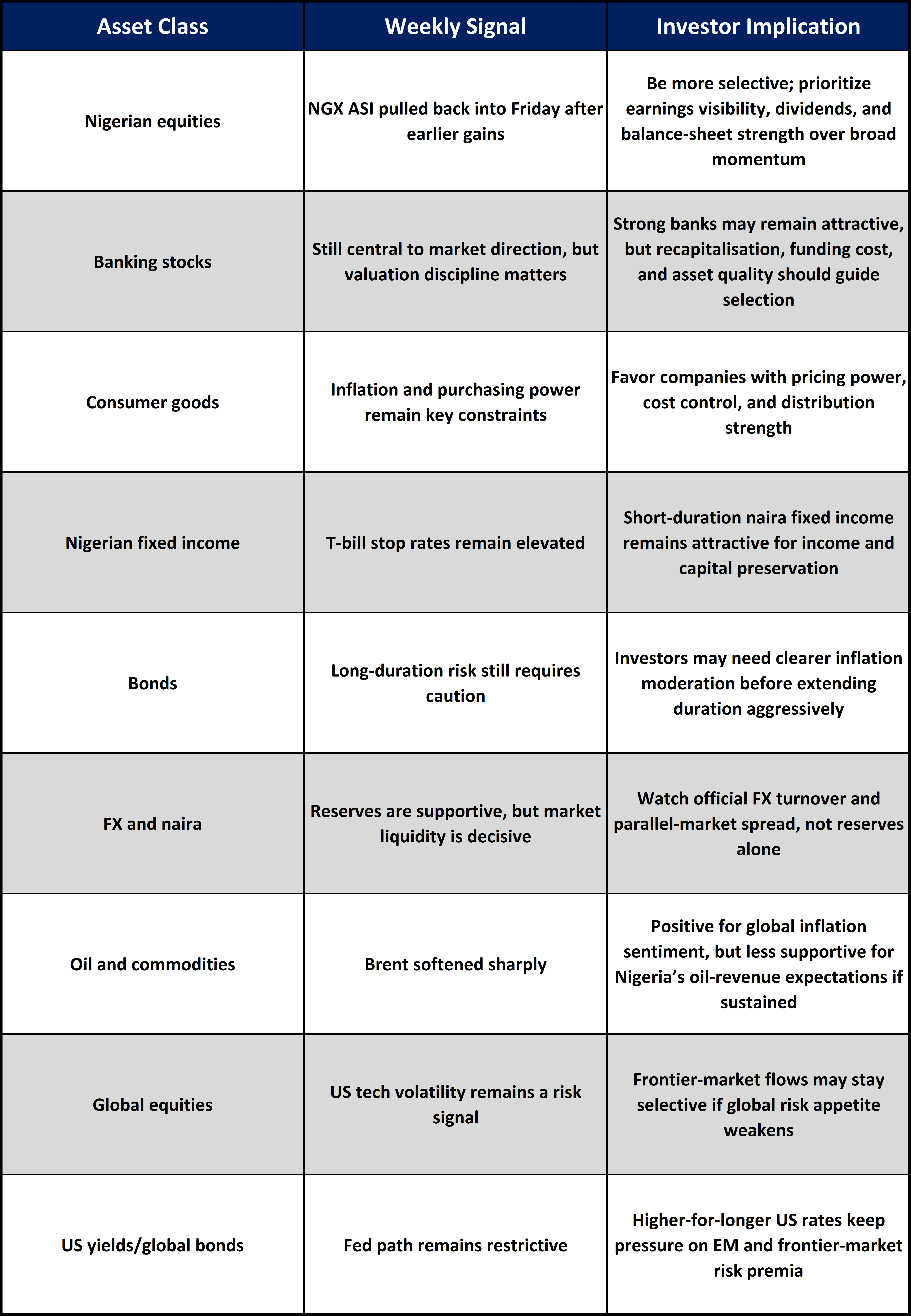

The strongest market message this week is that investors are no longer buying Nigerian risk indiscriminately. The NGX All-Share Index closed Friday at about 232,049 points, down on the day and lower than the previous Friday’s close, after a month that has already seen meaningful profit-taking from earlier highs. That does not mean the Nigerian equity story has broken. It means valuation discipline is returning, especially in sectors where prices had moved faster than earnings visibility.

For fixed income, the direction remains more straightforward: elevated policy rates, firm Treasury bill stop rates, and active liquidity management continue to support short-duration naira assets. The CBN’s latest policy stance remains tight, with the MPR at 26.5%, while May inflation rose to 15.93%. That combination keeps the argument for cash management, Treasury bills, and selective fixed income exposure intact.

Globally, investors received another reminder that the Fed is not yet finished with inflation. Core PCE rose 3.4% year-on-year in May, and the Fed’s June projections still imply a restrictive policy path. Softer Brent crude prices ease some pressure on global inflation, but for Nigeria they also reduce the upside from oil revenue unless production and export volumes compensate.

The Big Picture:

This was a week of repricing rather than panic.

In Nigeria, the equity market is digesting earlier gains. The NGX ASI remains substantially higher year-on-year, but the late-June pullback shows investors are becoming more selective. When an index has already delivered a strong run, the burden shifts from momentum to earnings, dividend sustainability, and sector-specific catalysts.

In fixed income, the market remains anchored by high nominal yields. The June 17 Treasury bills auction reportedly cleared at 16.28% for 91-day bills, 16.50% for 182-day bills, and 17.34% for 364-day bills, reinforcing that short-term sovereign paper remains competitive against equities where valuation risk has increased.

The naira story is more balanced. CBN exchange-rate data showed the NFEM rate around N1,380/$ on June 26, while external reserves have reportedly moved above $50 billion. That reserve build is supportive, but the real test is whether dollar supply remains deep enough to reduce volatility in the official market.

Globally, the Fed remains the main capital-flow signal. The FOMC held the federal funds target range at 3.50% to 3.75% on June 17 and its projection materials showed a 2026 median federal funds rate of 3.8%. That matters for Nigeria because higher US yields reduce the urgency for global investors to take frontier-market risk unless local yields and FX stability offer adequate compensation.

Nigeria Market Intelligence

Nigerian equities cooled as profit-taking continued.

What happened: The NGX All-Share Index closed Friday around 232,049.02, down 0.66% on the session, according to live market data. The index was also lower than the previous Friday’s 235,941.27 close, implying a weekly decline of roughly 1.65%.

Why it matters: The pullback is important because it came after a very strong prior rally. Investors are starting to distinguish between companies with earnings power and those that simply benefited from broad market momentum. This may reduce speculative breadth and increase demand for cash-generative names.

What comes next: Watch whether banking, consumer goods, and industrial names stabilize. A rebound with weak breadth would suggest tactical buying. A rebound with stronger volume and improved breadth would suggest investors are rebuilding positions.

Inflation is not yet low enough to relax the fixed income argument.

What happened: Nigeria’s headline inflation rose to 15.93% in May from 15.69% in April, while CBN inflation data also showed food inflation at 16.96% for May.

Why it matters: Even though inflation is much lower than the extreme levels seen in prior years, the recent rise reduces the case for a quick policy easing cycle. For investors, this keeps short-duration fixed income relevant, especially where yields offer a positive spread over expected near-term inflation.

What comes next: The June inflation print will matter more than usual. If inflation continues to edge higher, duration risk in bonds may stay unattractive. If month-on-month price pressure softens, investors may start looking further along the curve.

CBN policy remains restrictive.

What happened: The CBN’s Monetary Policy Committee retained the MPR at 26.5%, kept the standing facilities corridor at +50/-450 basis points, and retained CRR settings for banks in its latest policy decision page.

Why it matters: A high MPR and tight liquidity posture keep banks, corporates, and asset managers focused on short-term funding costs. This supports money-market yields, but it also raises the hurdle rate for equities and private-sector borrowing.

What comes next: The key question is whether the CBN keeps liquidity tight while inflation remains sticky. If it does, Treasury bills and OMO instruments may continue to compete strongly with equities.

Global Market Intelligence:

The Fed remains restrictive despite holding rates.

What happened: The Fed held the federal funds target range at 3.50% to 3.75% on June 17. Its June projections showed a 2026 median federal funds rate of 3.8%, while projected 2026 PCE inflation rose to 3.6% and core PCE inflation to 3.3%.

Why it matters: This is not a clear easing signal. For frontier markets, it means global capital may remain selective. Nigeria must offer both yield and FX credibility to attract foreign portfolio flows.

What comes next: US inflation, jobs data, and Fed communication will determine whether global investors add risk or stay defensive.

US inflation data still argues for patience.

What happened: BEA data showed US core PCE inflation at 3.4% year-on-year in May, up from 3.3% in April.

Why it matters: Core PCE is closely watched by the Fed. A move higher makes it harder for policymakers to justify near-term easing. That keeps US real yields relevant for global asset allocation and can reduce appetite for emerging and frontier markets.

What comes next: Watch whether June inflation confirms a sticky trend or gives the Fed room to soften its tone.

US equities remain vulnerable to tech concentration risk.

What happened: US market data on Friday showed the S&P 500 roughly flat to modestly positive intraday, while the Nasdaq was more volatile after earlier weakness in technology and semiconductor names.

Why it matters: A tech-led correction can affect global risk appetite even when Nigeria is not directly exposed to US technology earnings. If global funds reduce risk, frontier market flows can weaken.

What comes next: Watch whether the S&P 500 holds above key technical support and whether mega-cap technology earnings can stabilize sentiment.

Brent crude softened sharply.

What happened: Trading Economics showed Brent crude around $72.01 per barrel on June 26, down more than 4% on the day and roughly 22% over the past month.

Why it matters: Lower oil prices can reduce global inflation pressure, but for Nigeria they are a two-sided development. Softer Brent may reduce import-related inflation pressure indirectly, but it can also weaken fiscal and FX expectations if export revenue falls.

What comes next: Nigeria needs production consistency as much as price support. If Brent stays softer, volume and fiscal discipline become more important.

Asset Class Implications:

Ranora View:

Ranora’s view is that Nigerian investors should treat this week as a reminder that yield, liquidity, and earnings quality are now doing more work than market momentum.

Equities still have a role, but the easy phase of broad re-rating looks less compelling after the recent pullback. The better approach is not to exit risk entirely, but to separate structurally strong companies from crowded trades. Banks, select consumer names, and high-quality industrials may still deserve attention, but only where earnings growth can justify valuations.

Fixed income remains the cleaner near-term opportunity. With inflation at 15.93%, the MPR at 26.5%, and one-year Treasury bill stop rates reportedly above 17%, short-duration sovereign exposure continues to offer a useful income anchor. This may keep institutional portfolios tilted toward bills and money-market instruments until inflation clearly turns lower or equities reset to more attractive entry levels.

For businesses, the message is equally clear: capital remains expensive, FX planning still matters, and pricing power remains a strategic advantage. Companies that can protect margins without destroying demand should be better positioned than those relying on cheap funding or volume growth alone.

What to Watch Next:

June inflation data: A further rise would strengthen the case for tight policy and short-duration fixed income.

NGX market breadth: Watch whether the next rebound is broad-based or concentrated in a few heavyweights.

Treasury bill auction demand: Strong subscriptions at elevated stop rates would confirm that yield remains the market’s anchor.

Official FX turnover and naira spreads: The reserve build is helpful, but liquidity at the official window is the real confidence test.

US inflation and Fed commentary: A sticky inflation path may keep global risk appetite restrained and reduce foreign appetite for frontier exposure.

Question of the day:

If Nigerian Treasury bills continue to offer attractive yields while equities pull back, would you increase fixed income exposure or use the equity weakness to build positions in quality stocks?

Stay smart. Stay informed. Subscribe to Ranora Market Outlook for free and support independent market analysis.