Midweek Wire - The $50bn Refinery Play, A Regulatory Dividend Block, and Why Nigeria's Oil Quota Miss Matters More Than You Think

Wednesday, May 13, 2026 | Ranora Consulting Market Intelligence

WELCOME — MIDWEEK CHECK-IN

Good evening, investors.

We’re at the midpoint of a week that started with tightening liquidity and big expansion ambitions and Wednesday is not slowing down. On Monday, we flagged the CBN’s aggressive ₦3.3 trillion OMO sales as a deliberate move to rein in system cash, and raised the question: would tighter liquidity create fresh opportunities or deepen defensive positioning before midweek? We now have part of the answer. Today, that same system liquidity has spiked 40% following OMO bill repayments a sharp, near-term reversal that shifts the tone in the money market. Meanwhile, Dangote is back in the headlines this time not with Kenya expansion plans (as we covered Monday), but with a $50 billion valuation target ahead of a potential stock market listing. The DMO has announced a ₦600 billion FGN bond auction. Access Holdings is navigating a regulatory block on dividend payments. And globally, the U.S.-China trade picture just got more interesting.

Here’s everything you need to know to stay positioned heading into the second half of this week.

NIGERIA — WHAT'S MOVING

Financial Markets

Access Holdings Blocked from Paying 2025 Dividend:

Regulators have stepped in to restrict Access Holdings from paying its 2025 dividend a signal that capital retention requirements in the banking sector remain a live issue. For dividend-seeking retail investors, this is a reminder that regulatory risk in Nigerian banking is real and must be priced in. The broader question: which other tier-1 banks could face similar restrictions? - Dmarketforces

Money Market System Liquidity Jumps 40% on OMO Repayment:

Recall Monday’s CBN OMO sales of ₦3.3 trillion? well, that maturity cycle has started releasing cash back into the system. A 40% spike in financial system liquidity is material. Expect short-term rates to soften and watch for the CBN’s response. Will they conduct another OMO sale to mop up the excess? This is a key signal for where rates and the naira could move into the weekend. - Dmarketforces

Fixed Income DMO Announces ₦600bn FGN Bond Auction for May 2026:

Hot on the heels of Monday's liquidity tightening via OMO sales, the DMO is now offering ₦600 billion in FGN bonds. This is a significant government borrowing move and coming in the same week as the 40% liquidity spike, it will be closely watched. Higher system liquidity could support demand at the auction, potentially keeping yields from rising sharply. Fixed income investors should monitor bid-to-cover ratios closely. - Channels

Energy / Capital Markets

Dangote Targets $50bn Refinery Valuation Before Listing:

Following Monday's report of a potential $17bn Kenya expansion, Dangote Group is now signaling its intent to list and the price tag is $50 billion. This is a landmark development for Nigerian capital markets. A listing of that scale would be the largest in NGX history and would redefine the energy-investment landscape in West Africa. Investors should begin watching for pre-IPO signals, institutional positioning, and any timeline disclosures. - Punch

Energy

Nigeria Misses OPEC Production Quota Again:

Nigeria failed to meet its OPEC crude oil production quota again, highlighting ongoing challenges in output capacity and supply stability within the oil sector. - Channels

Consumer Goods

Cadbury Nigeria Names New MD as Folake Ogundipe Steps Down:

Leadership transitions at listed consumer goods firms always invite scrutiny especially in an inflation-pressured environment. The incoming MD, Gaafar, inherits a company navigating rising input costs and a cautious consumer. Watch for any strategic or margin commentary at the next investor briefing. - BusinessDay

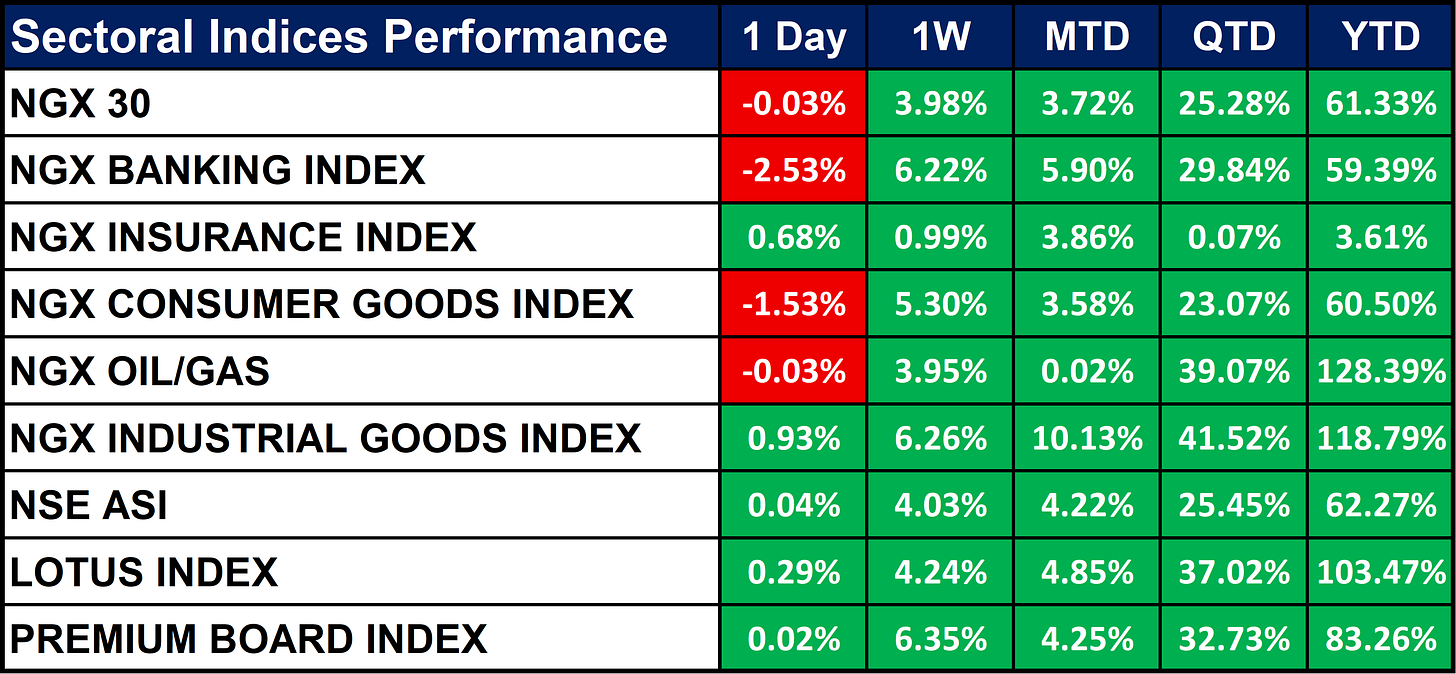

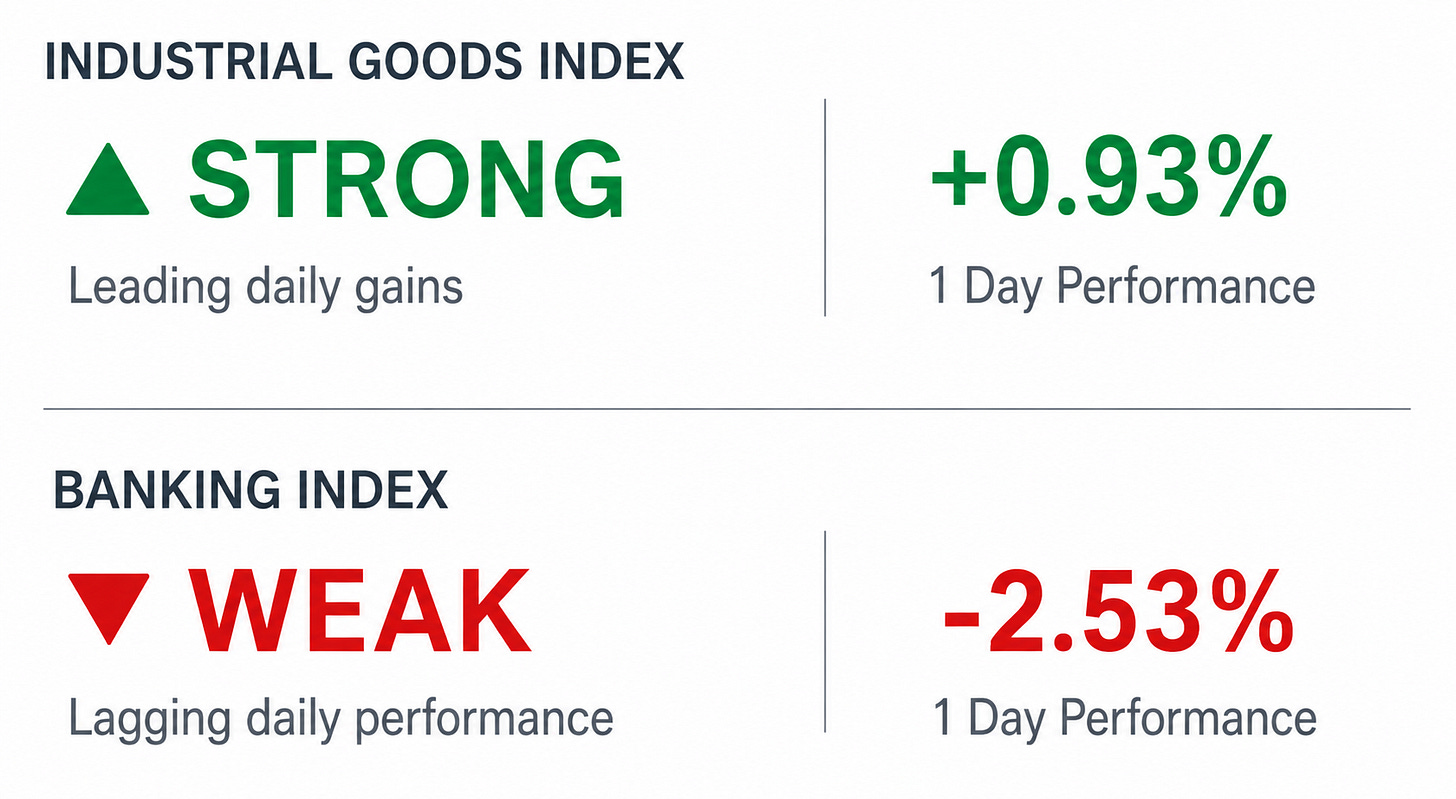

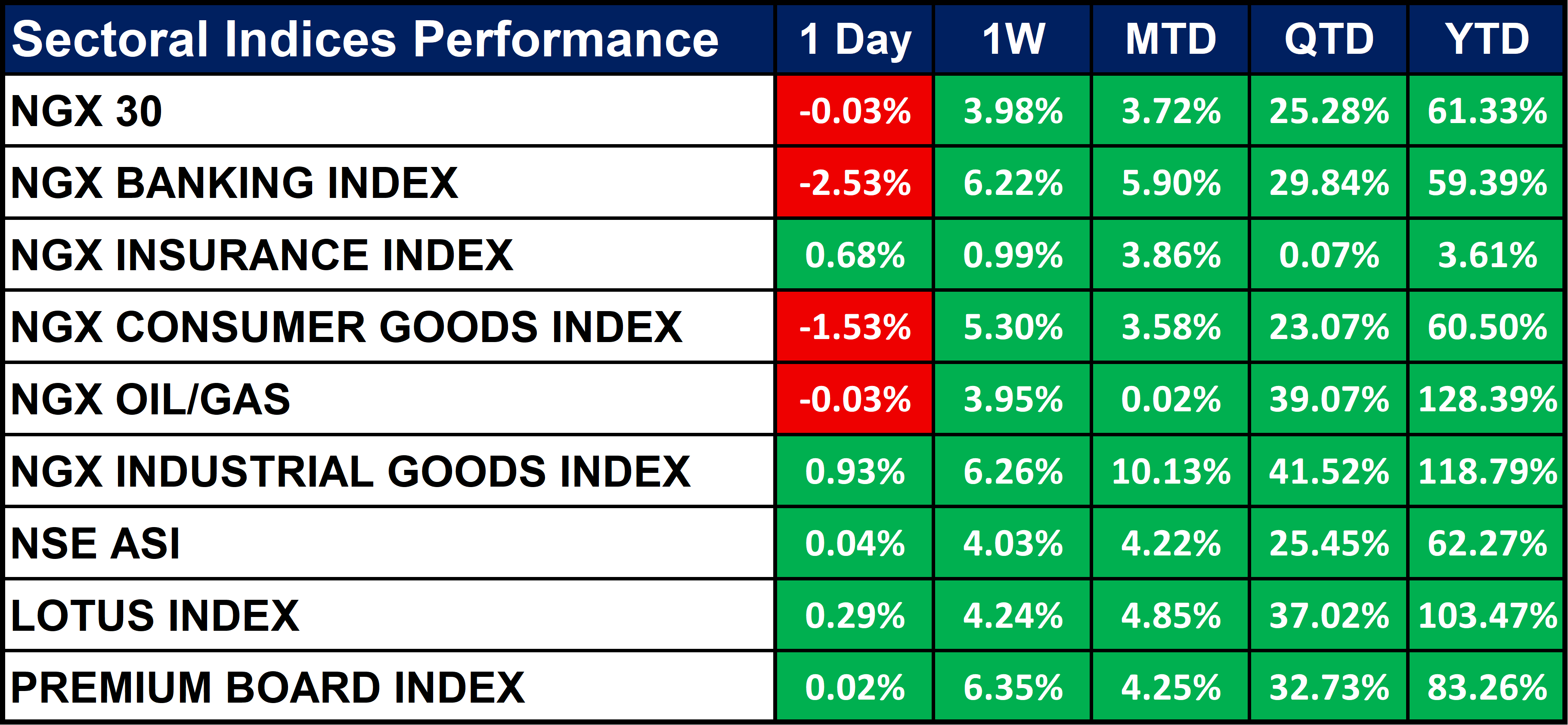

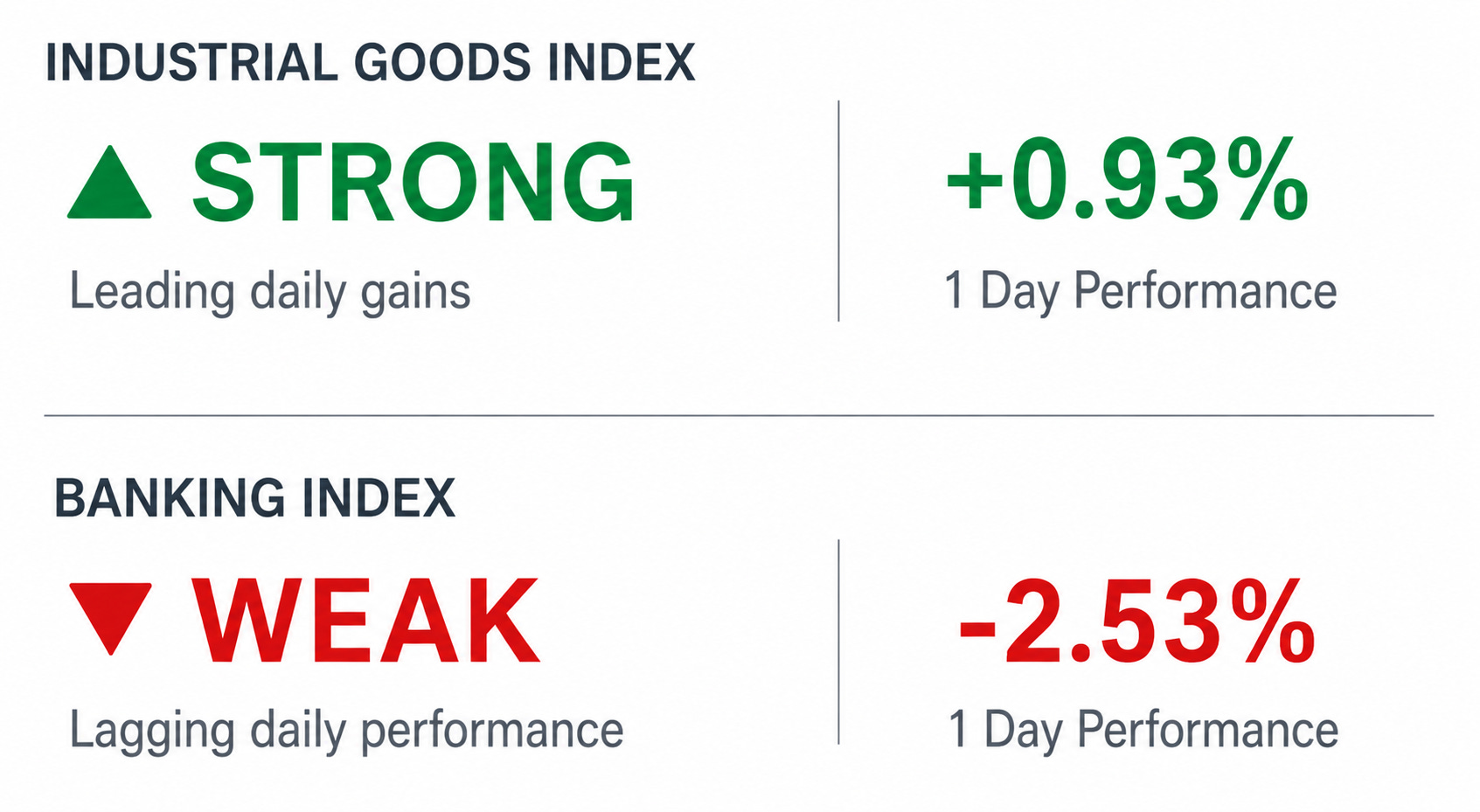

Nigeria Sectoral Indices Performance

Nigerian equities closed mixed with a cautious tone, as gains in Industrial Goods and Insurance were offset by declines in Banking and Consumer Goods.

The Industrial Goods Index led daily performance, while the Banking Index lagged amid profit-taking and regulatory concerns. Overall, investors remain selective, favoring defensive and fundamentally strong sectors despite volatility in financial stocks.

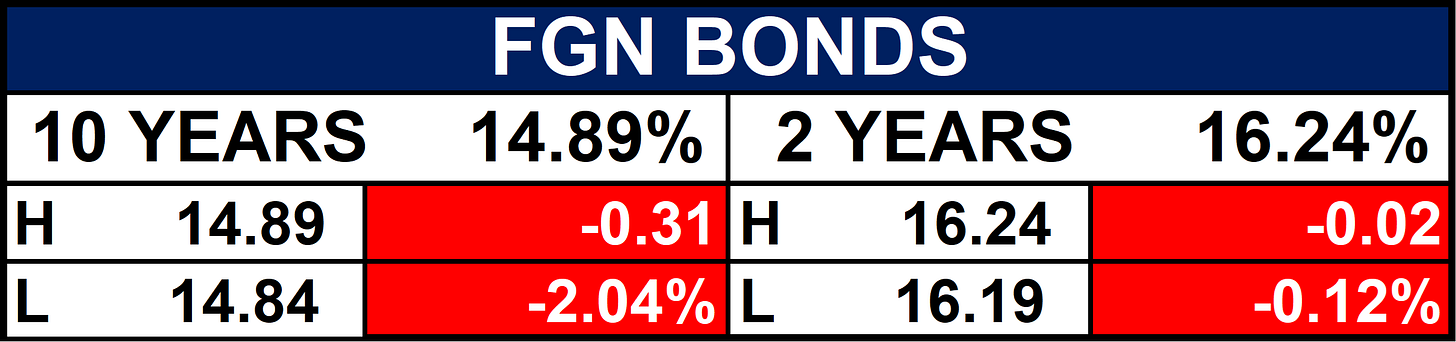

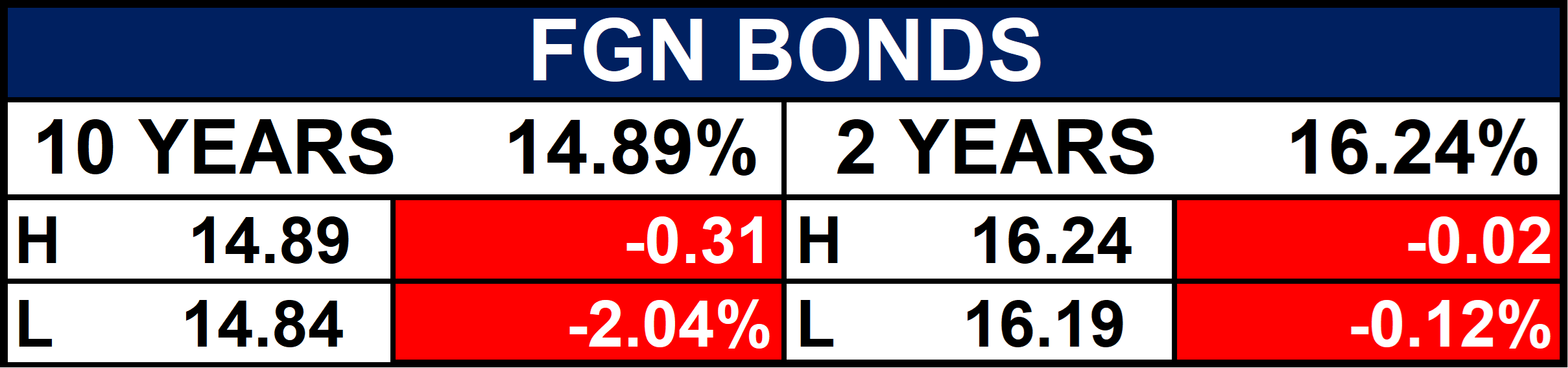

Fixed Income (FGN Bonds)

GLOBAL — THE BIG PICTURE

Geopolitics / Trade Policy (North America & Asia)

Trump & Xi Consider Tariff Cuts on $30bn+ in Imports:

This is potentially the biggest global macro story of the week. If the U.S. and China move toward meaningful tariff reductions, it would ease global supply chain tensions, support commodity demand, and boost risk appetite across emerging markets including Nigeria. It's early, but any confirmed de-escalation would be broadly positive for frontier and emerging market equities. - Reuters

Energy (Global)

OPEC Cuts 2026 Oil Demand Growth Forecast:

Paired with Nigeria's domestic production failures, this downward revision from OPEC on global demand growth signals a softer oil price environment ahead. For a country where oil still drives the fiscal narrative, this should be front of mind for anyone tracking the naira, external reserves, or the FGN's 2026 budget assumptions. - ReutersINFLATION WATCH

Both Brazil and India printed in-line-to-slightly-hotter inflation in April. These are important proxies for emerging market central bank policy. Persistent inflation globally means higher-for-longer rates remain the base case, a headwind for capital flows into frontier markets like Nigeria.

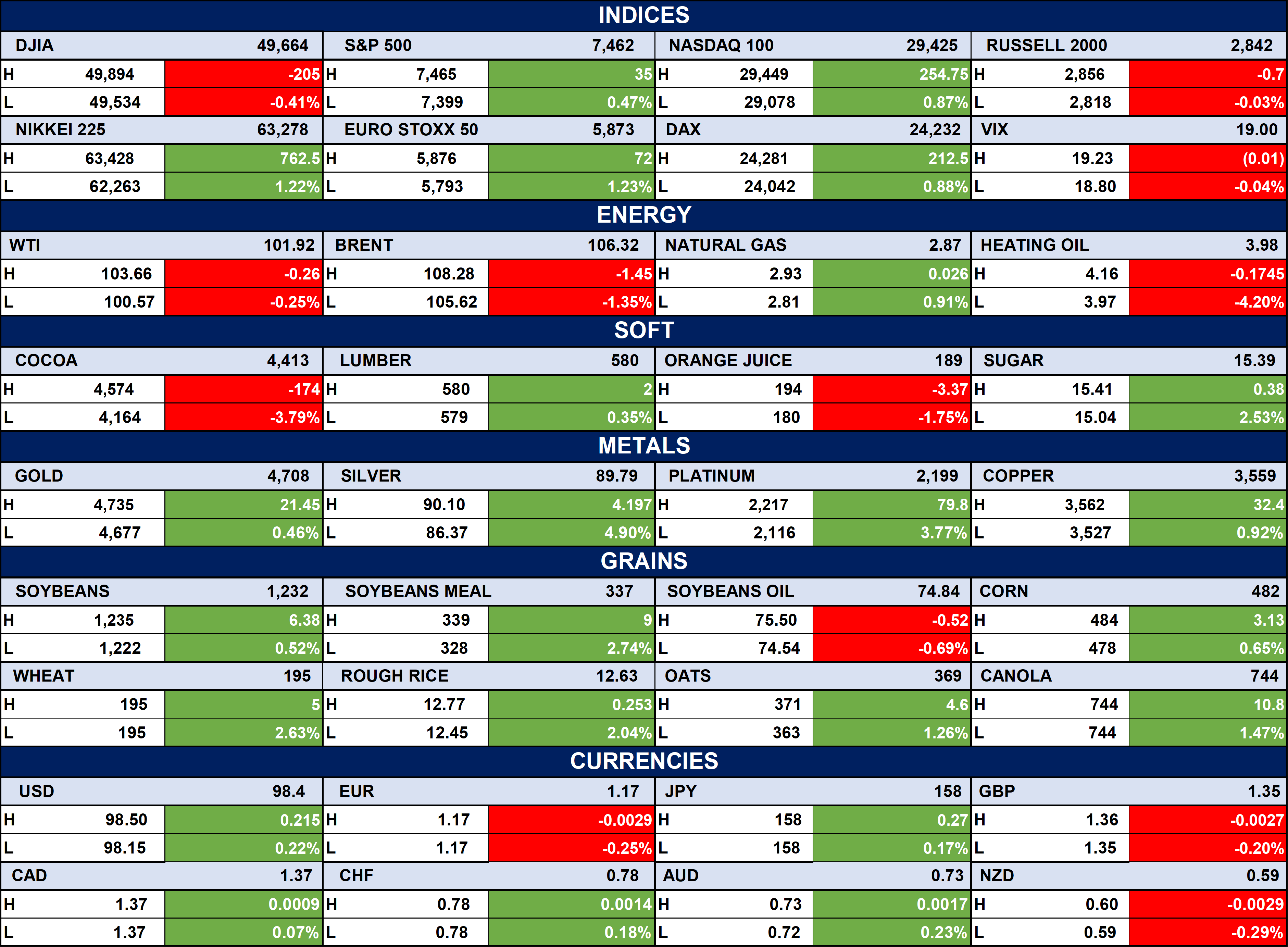

Indices, Commodities & Currencies

The table below shows that the Global markets closed mixed with a cautiously positive tone, as gains in major equities contrasted with softer energy prices and selective weakness in risk assets. Metals and agricultural commodities remained strong, reflecting continued positioning toward inflation-sensitive and defensive assets. Overall, investors remain selective amid ongoing macroeconomic uncertainty, shifting energy dynamics, and evolving global policy expectations.

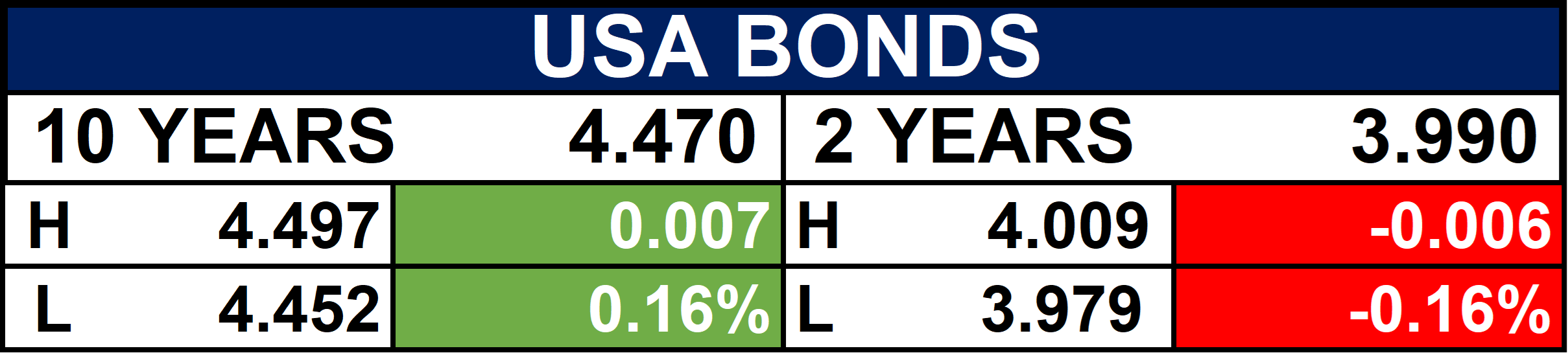

Fixed Income (USA Bonds)

Event

WHAT TO WATCH BEFORE FRIDAY

Here’s where the threads connect heading into the back half of the week:

Liquidity vs. Bonds — System liquidity just jumped 40%. The DMO wants to borrow ₦600bn. Will excess cash find its way to the bond auction, suppressing yields? Or will the CBN intervene again with OMO sales?

Dangote’s $50bn Signal — A listing ambition of this scale needs an institutional audience. Is this a pre-marketing move? Watch for any analyst briefings or investor roadshow leaks.

Oil & Revenue Pressure — Nigeria’s quota miss plus OPEC’s demand downgrade is a compounding fiscal risk. Any downward revision to government revenue projections may tighten the FGN’s fiscal space and increase bond issuance pressure.

U.S.-China Trade Thaw — If tariff cuts materialize, watch for a risk-on wave that lifts commodity prices, emerging market equities, and global trade volumes. Nigeria’s non-oil export play becomes more attractive in that scenario.

CLOSING NOTE

Wednesday has confirmed what Monday hinted at this week is a tug-of-war between liquidity, regulation, and ambition. The CBN is managing the system tightly, the DMO is borrowing boldly, and Dangote is thinking in billions. Meanwhile, Nigeria’s oil story continues to disappoint at the production level, even as the refinery story grows more compelling by the day.

The market is not moving in one direction and that’s exactly where opportunity hides.

We’ll be back Friday with a full week wrap-up, deeper data, and our outlook for the week ahead. Don’t miss it, Friday’s edition is where we connect all the dots.

Thanks for reading Ranora Consulting! Subscribe for free to receive new posts and support my work.